Market Overview Q2 2025

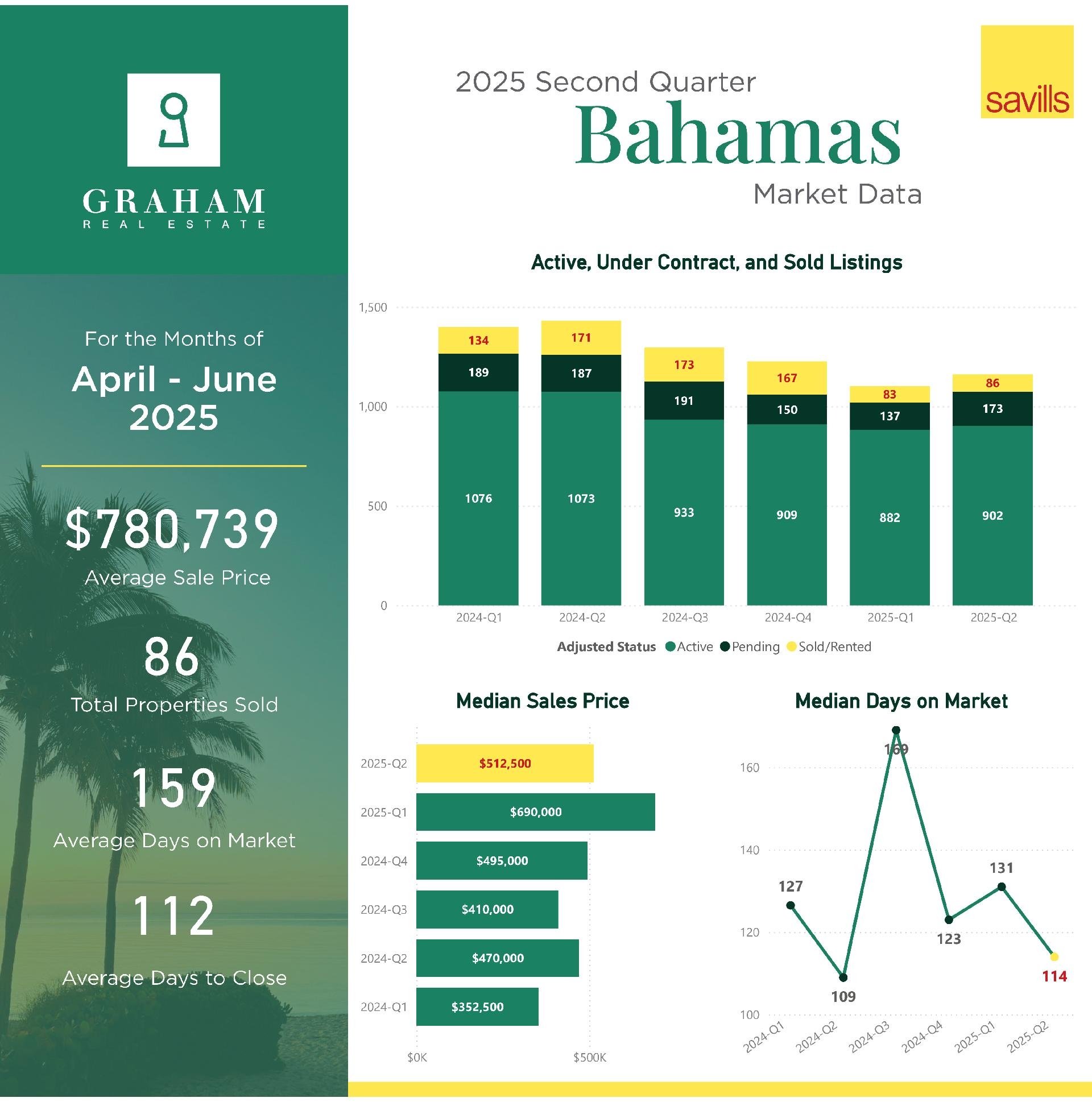

The Bahamian real estate market continued to show mixed signals in the second quarter of 2025. While overall sales volume rose in many regions, price trends suggest a pivot toward mid-range homes and a move away from the high-end spikes seen in prior quarters. Buyers appear increasingly motivated by value and pricing realism, especially in regions where inventory is sufficient and properties are properly positioned. Although average sale prices dipped in several markets, faster sales timelines and stronger pending figures suggest demand remains healthy, with a shift in where and how that demand is being expressed.

Looking Ahead

Recent changes to VAT and real property legislation in The Bahamas are expected to introduce additional administrative hurdles and red tape, potentially slowing an already lengthy and cumbersome closing process. These new requirements place increased liability on industry professionals and may create confusion for both buyers and sellers as they navigate unclear registration procedures. While the long-term impact remains to be seen, the immediate effect is likely to be further delays and frustration across the real estate sector.

Given this shifting landscape, we highly recommend that buyers and sellers work with experienced, knowledgeable, and trusted real estate agents and attorneys who can help navigate these changes and safeguard their interests.

We’ll share a more detailed breakdown of these regulatory changes in an upcoming blog post.

GRE Islands

The GRE Islands showed steady momentum. Active listings climbed slightly to 902, and more importantly, pending sales increased from 137 to 173, a strong indicator of forward demand. Closed sales rose modestly to 86. However, a sharp decline in average price from $1.65M to $780K, and median from $690K to $512K, reflects a shift in buyer preference toward moderately priced homes. This isn’t necessarily a price crash but a broadening of the transaction base. The improvement in median days on market from 131 to 114 suggests buyers are more decisive when the property is priced appropriately.

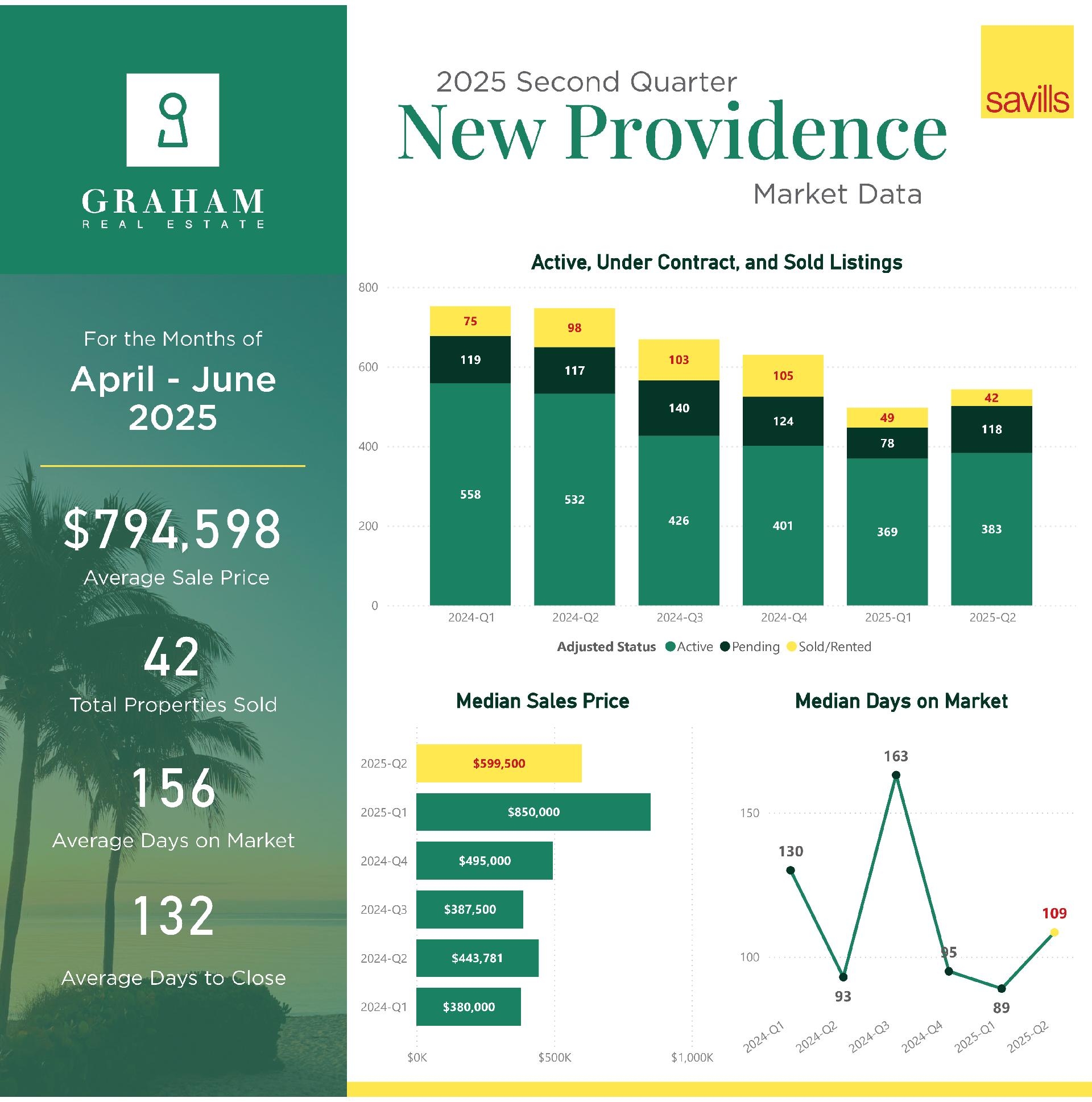

New Providence

New Providence posted 118 pending sales, up from 78, indicating strong forward momentum. Though closed sales dipped slightly to 42, the sharp drop in average price (from $1.76M to $794K) and median (from $850K to $599K) suggests a swing back toward mid-market homes and condos. Slight increases in time on market reflect normal friction in a shifting market. Demand remains strong; it’s simply adjusting to more practical price points.

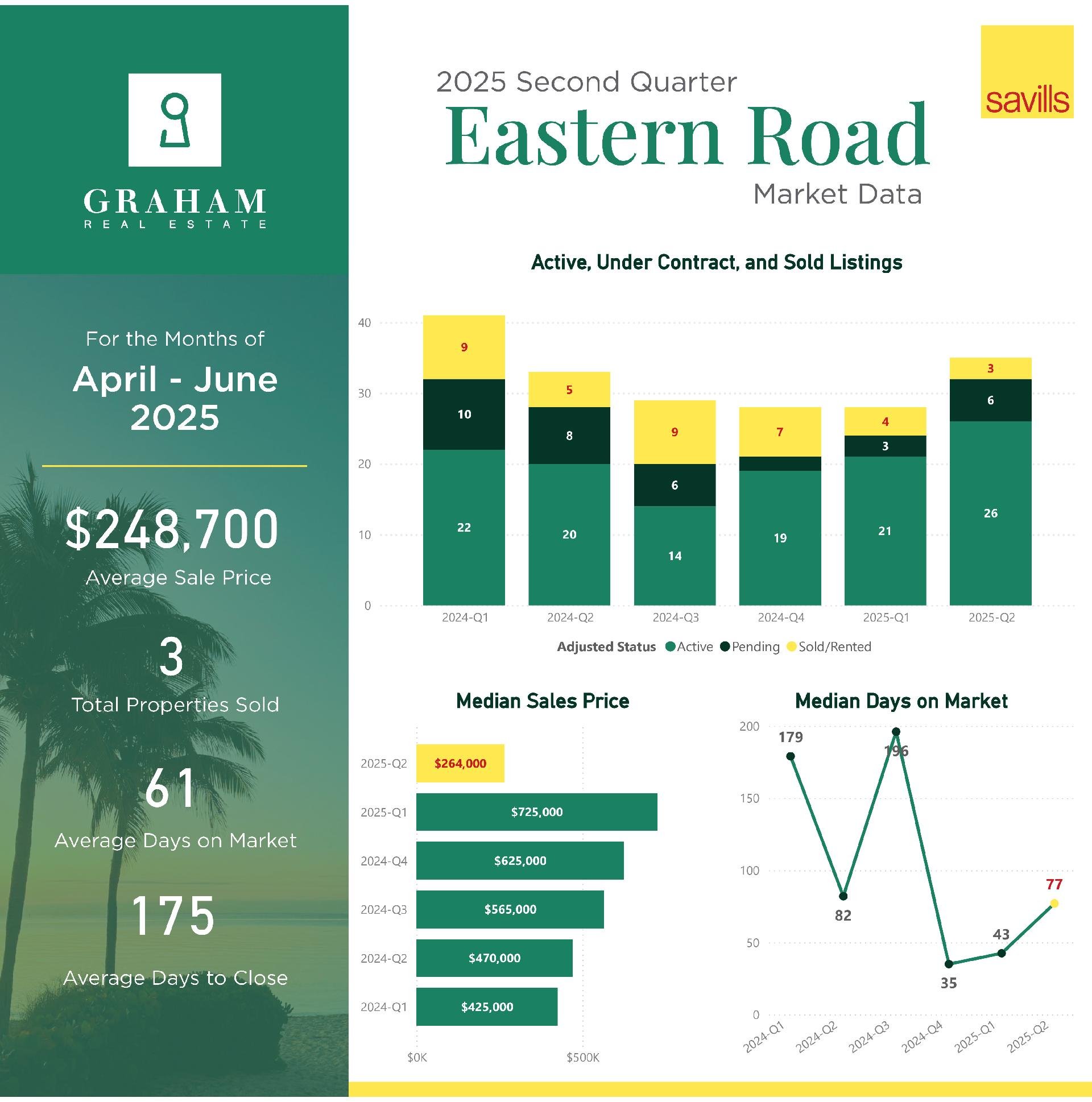

Eastern Road

Sales slowed slightly in Eastern Road with 3 homes sold, down from 4, though listings and pending activity increased. The average sale price fell to $248K from over $1.5M, indicating a possible shift in the mix toward more modest homes or older properties. Time to close remained consistent, and median days on market rose slightly, possibly due to variation in listing quality or readiness.

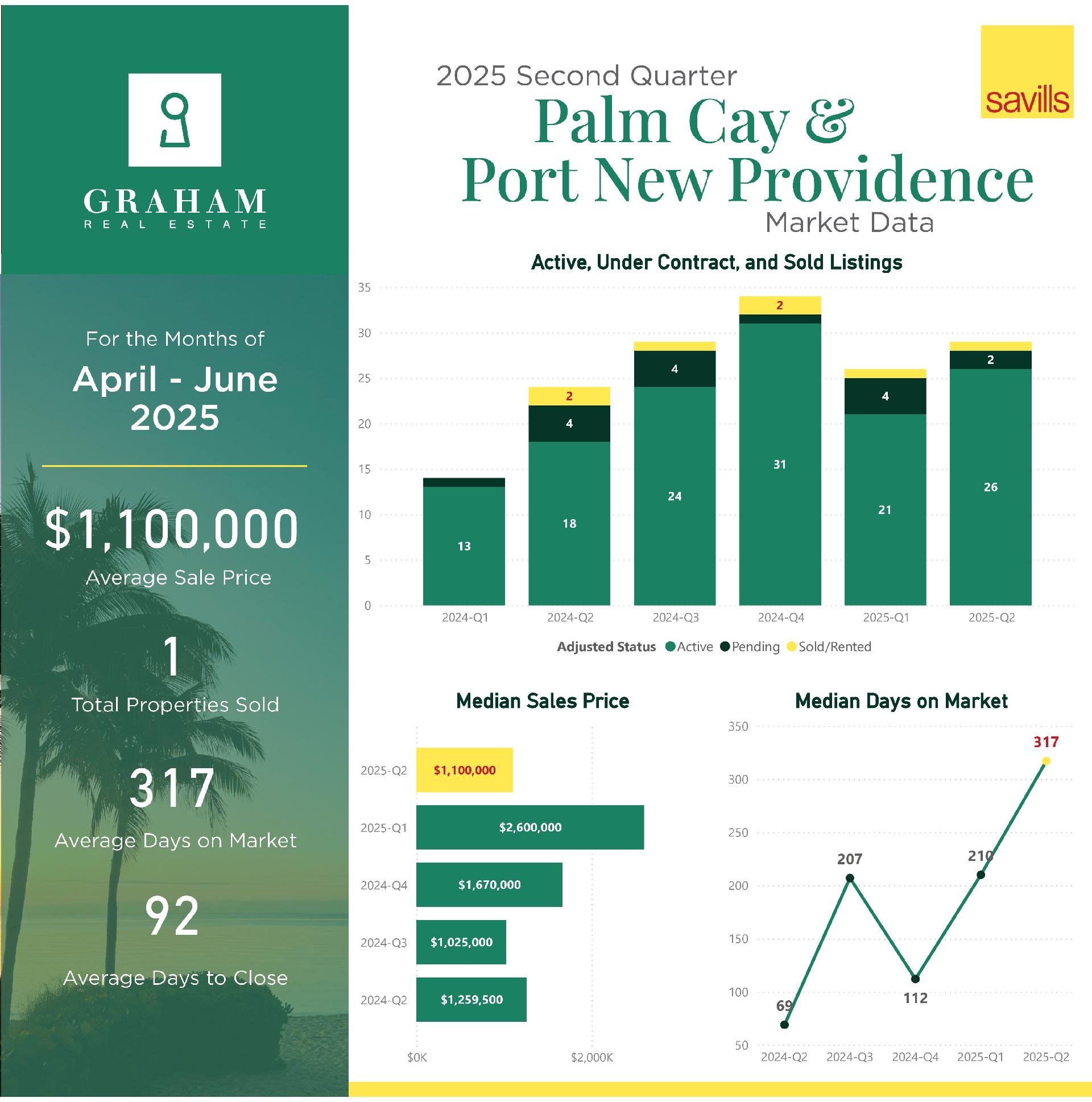

Port New Providence & Palm Cay

With only 1 sale, this high-end market was quiet in Q2. The property sold at $1.1M, well below Q1’s $2.6M, though that price shift likely reflects the unique nature of each transaction. The time on market increased to 317 days, consistent with the pace of ultra-luxury sales. Listings rose, suggesting sellers remain confident, though buyers are taking longer to commit at this price level.

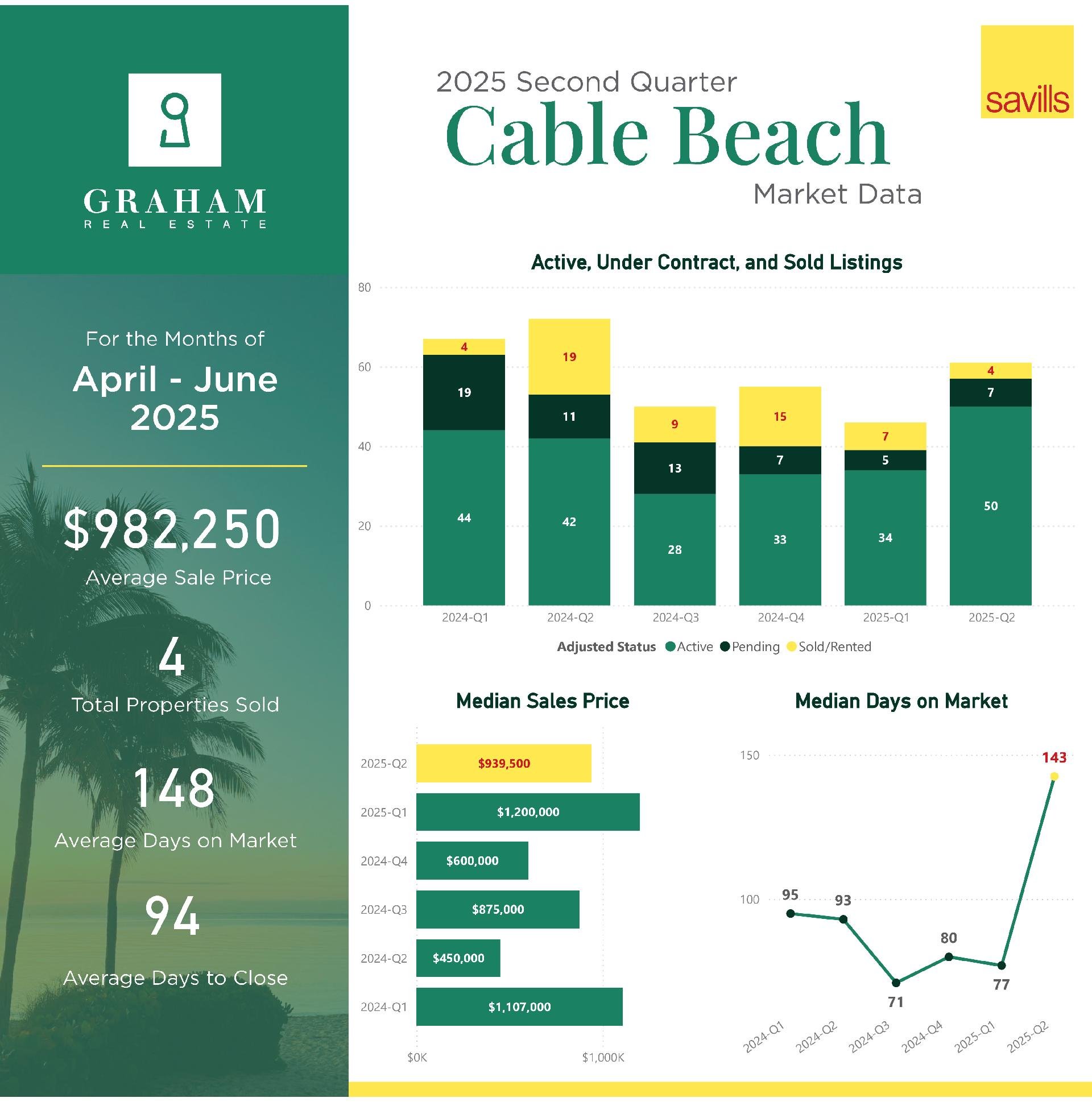

Cable Beach

Cable Beach had a lighter quarter, with 4 homes sold, down from 7, and a moderate price dip to $982K average. The median slipped to $939K. Longer days on market — now averaging 148 — indicate that buyers may be hesitating on higher-end product or waiting for price corrections. The area remains fundamentally strong, but current activity suggests buyers are being selective.

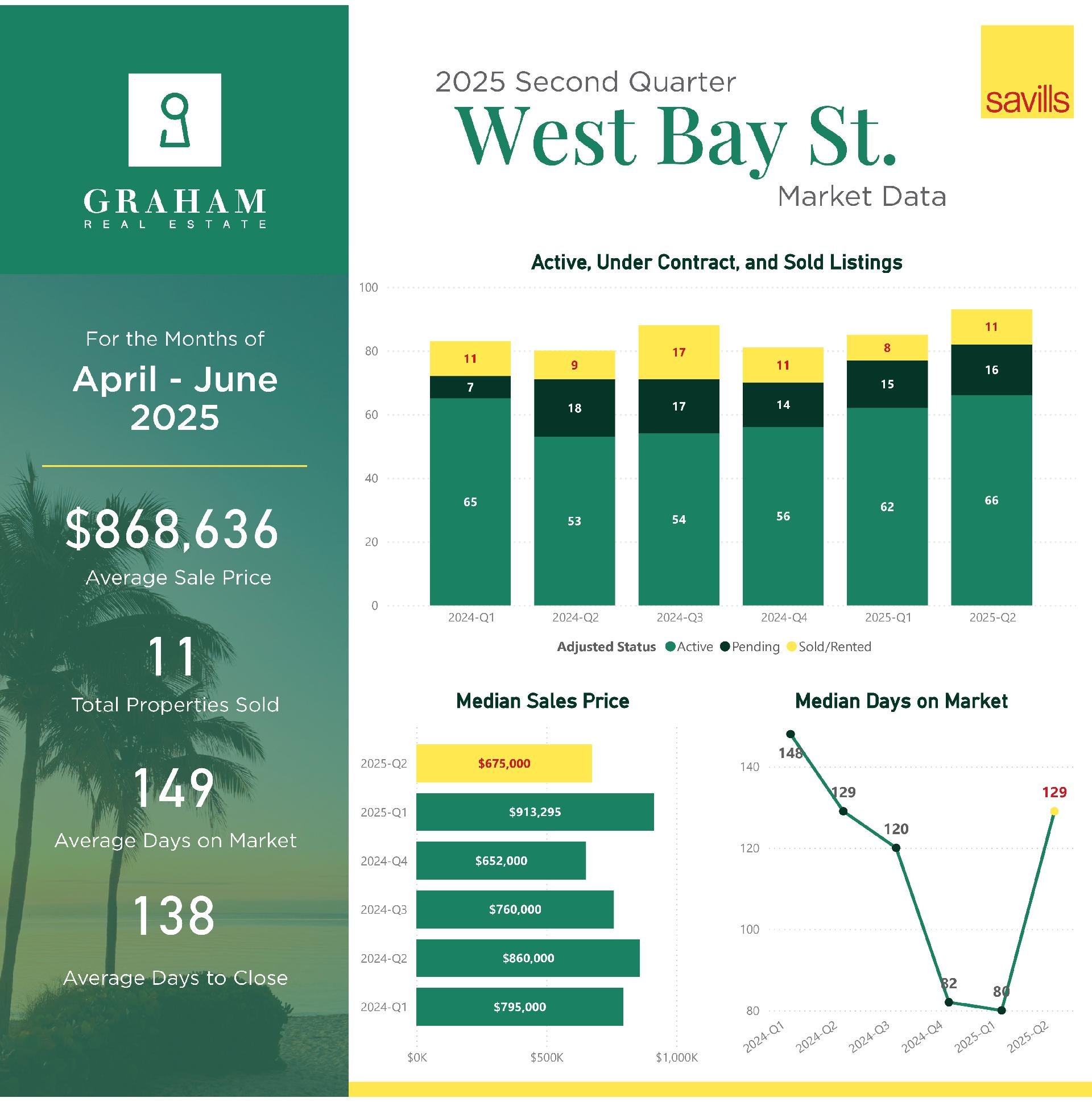

West Bay Street

West Bay Street saw a rise in activity, with 11 homes sold, up from 8, and pending listings holding steady. Pricing adjusted slightly downward, with the median at $675K. Sales timelines lengthened, with average days on market now at 149, indicating that while demand is solid, buyers are taking more time to negotiate or finance.

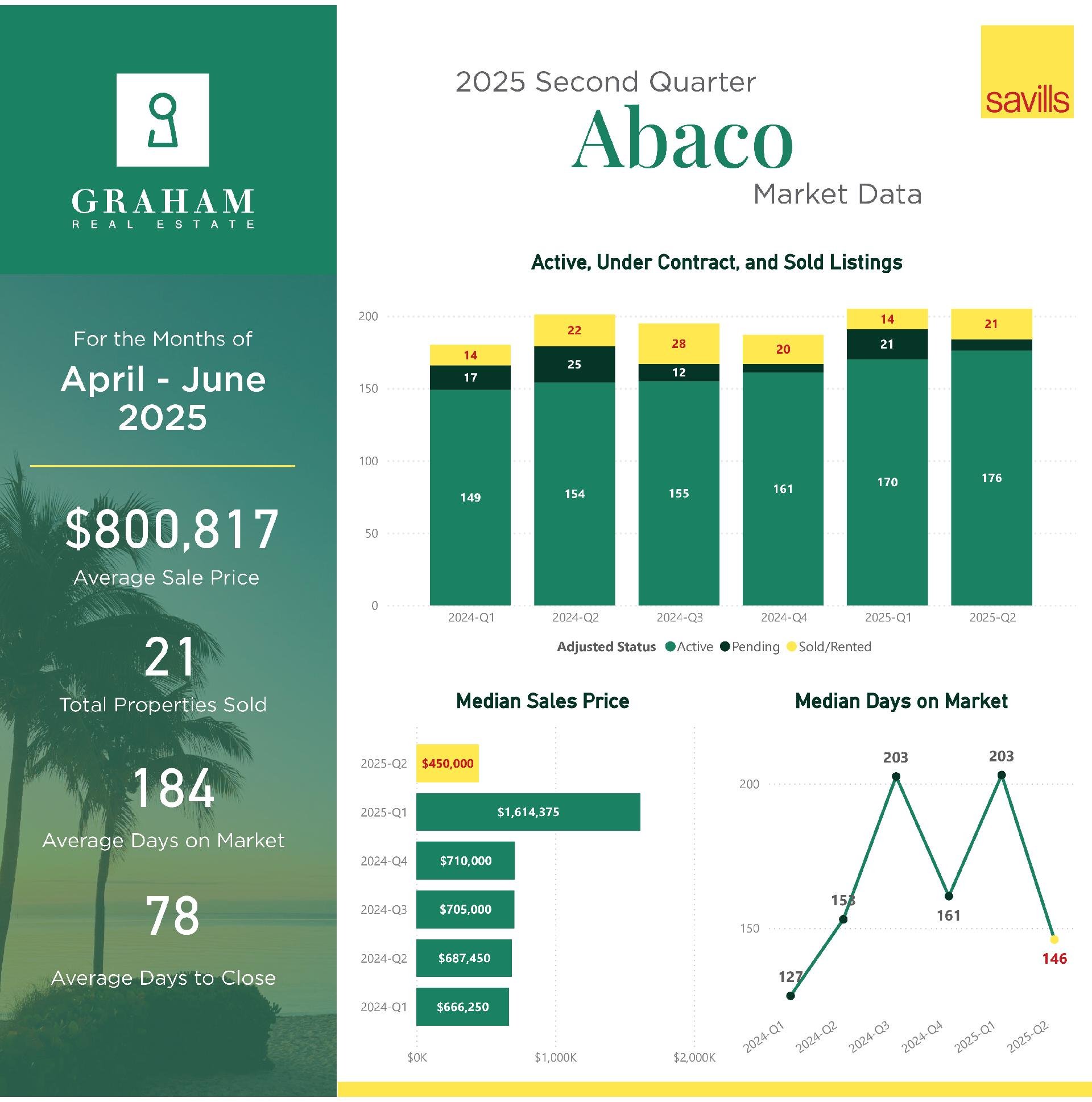

Abaco

Abaco saw a 50% increase in sold listings (from 14 to 21), a positive sign of deepening activity. The drop in pending listings (from 21 to 8) might initially seem concerning, but in context, it likely indicates that Q1 contracts successfully closed. The steep decline in average price (from $2.2M to $800K) and median (from $1.6M to $450K) points to a clear pivot away from luxury properties toward homes priced for working families or second-home buyers. Faster sales, with average days on market dropping to 184, confirm that appropriately priced inventory is moving.

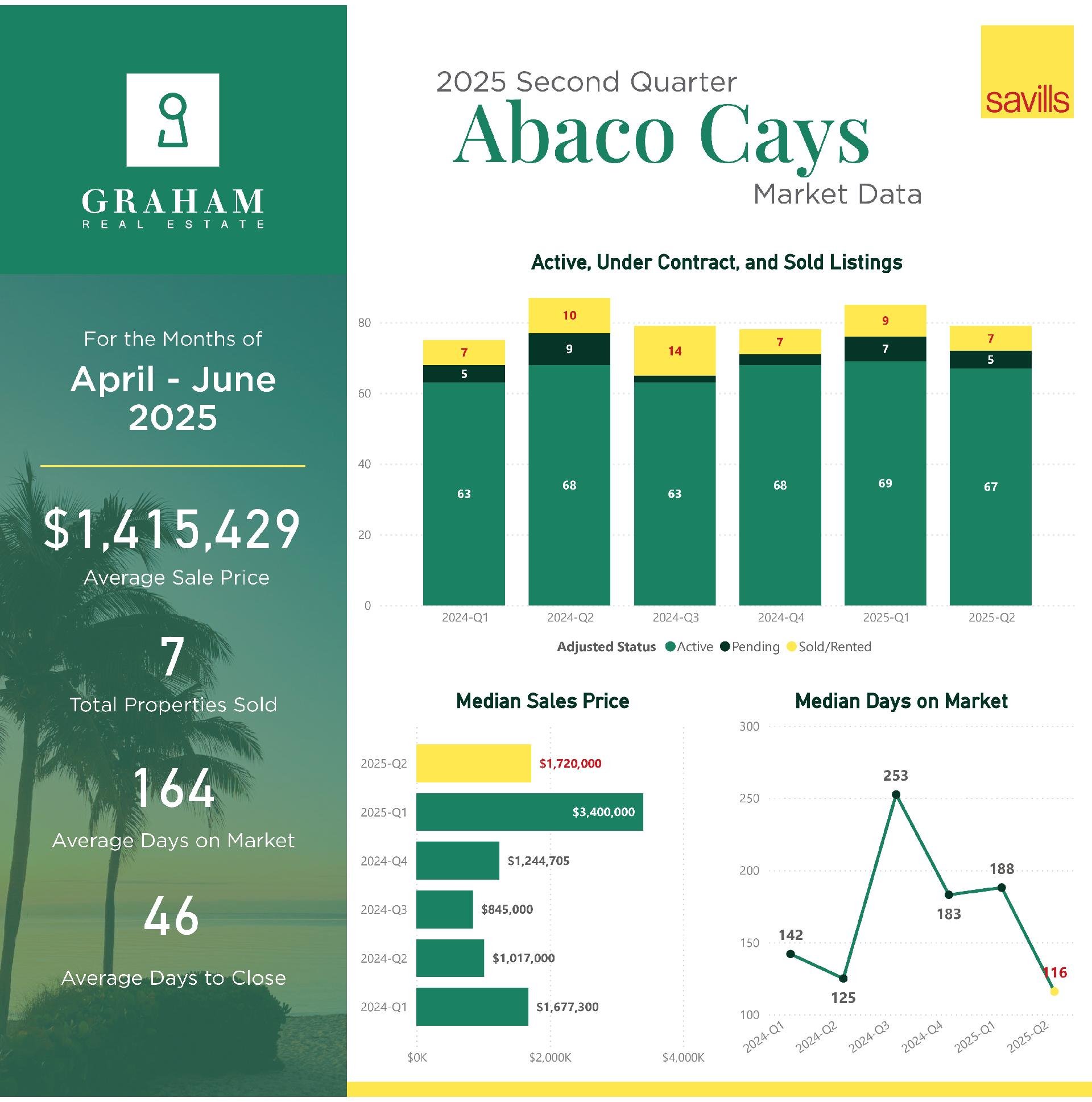

Abaco Cays

Sales volume eased in the Abaco Cays, with 7 homes sold, down from 9, and pending sales slipped slightly. Price reductions were significant — average sale price fell from $2.65M to $1.41M, and median from $3.4M to $1.72M. While this may seem drastic, it’s more likely reflective of a pause in ultra-luxury transactions. Meanwhile, sales pace improved, with homes selling in 116 median days, down from 188, signaling buyers are still active when pricing adjusts to market expectations.

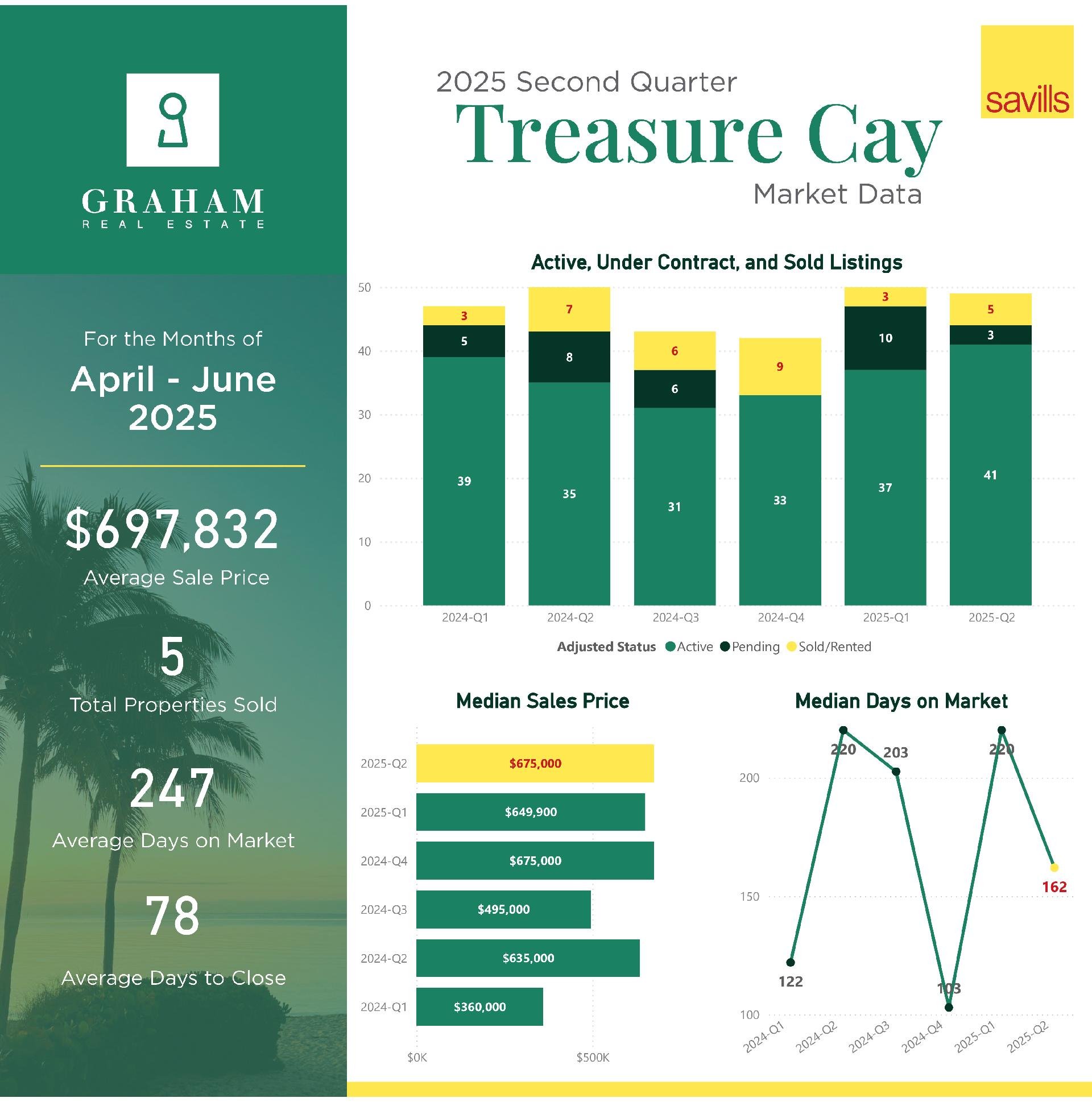

Treasure Cay

Treasure Cay posted a modest increase in sales (from 3 to 5), though pending contracts dropped from 10 to 3, suggesting possible inventory bottlenecks or buyer hesitancy. Notably, the median price increased slightly to $675K, and days on market shortened across the board. While the average price declined sharply, this was influenced by the small sample size and mix of inventory. The market appears to be finding a new price floor and could benefit from more mid-tier listings.

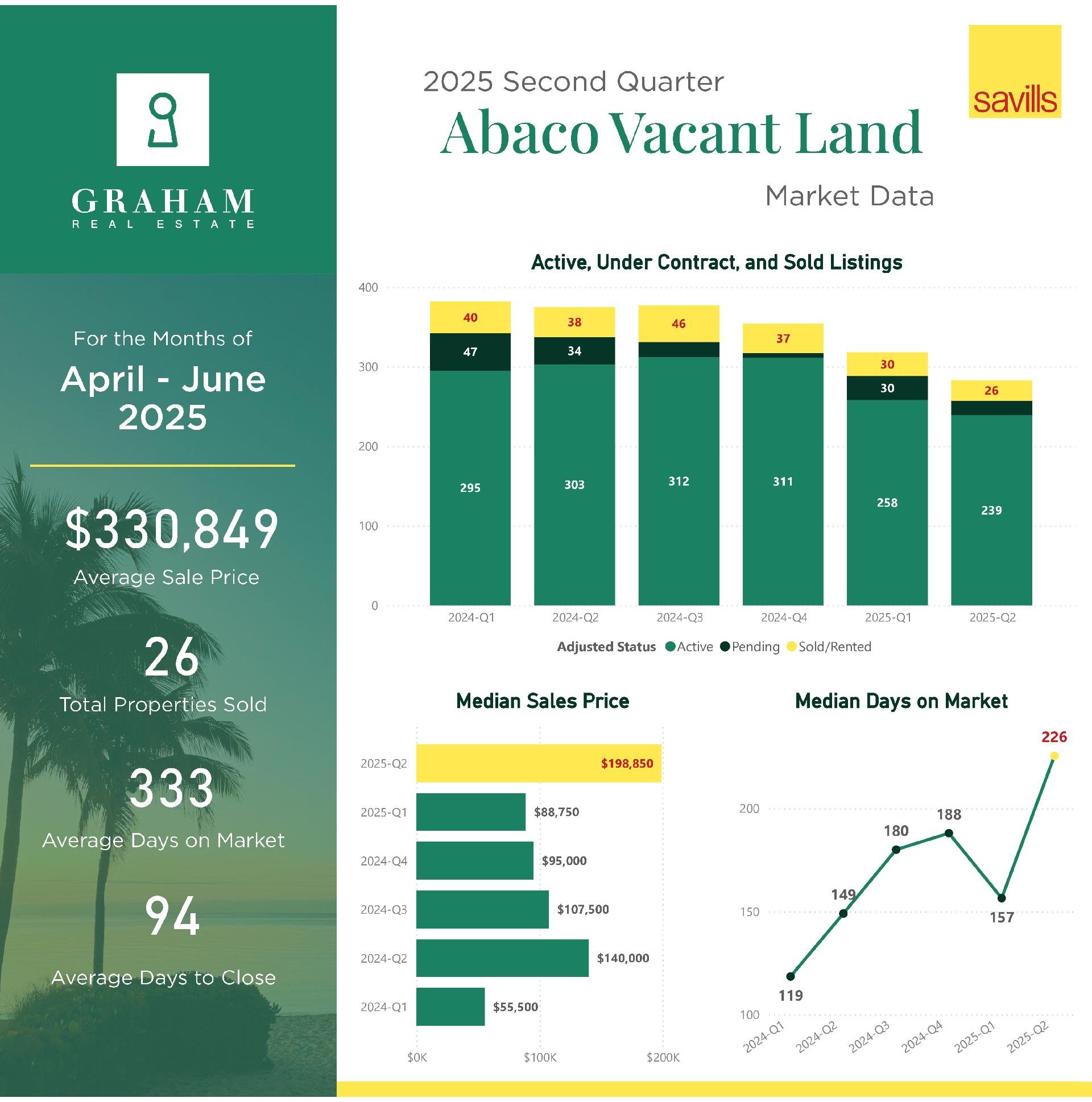

Abaco Land

Abaco Land saw a small drop in transactions, from 30 to 26, but pricing more than doubled, with the median rising to $198,850. This suggests larger or more desirable parcels are beginning to move. Days on market and time to close both improved, despite the higher values, which bodes well for landowners considering a sale.

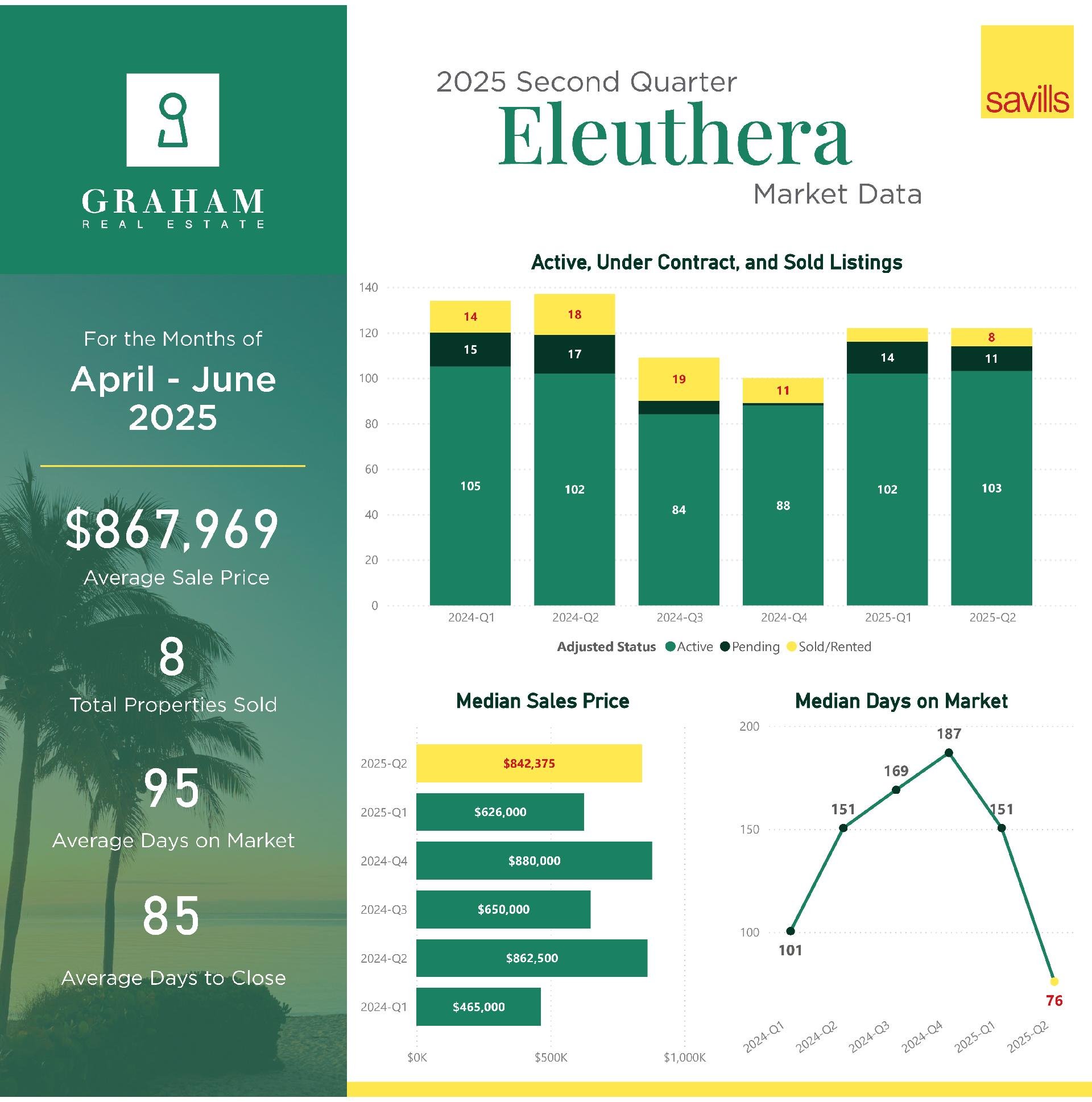

Eleuthera

Eleuthera saw a more active and balanced quarter. Sales increased from 6 to 8, and prices improved across the board. The average sale rose to $867K and the median to $842K, with faster transactions — homes sold in 76 median days, nearly half the time of Q1. The combination of improved pricing and shorter time on market shows a more confident and responsive buyer base. Eleuthera is clearly benefiting from having a mix of well-positioned inventory.

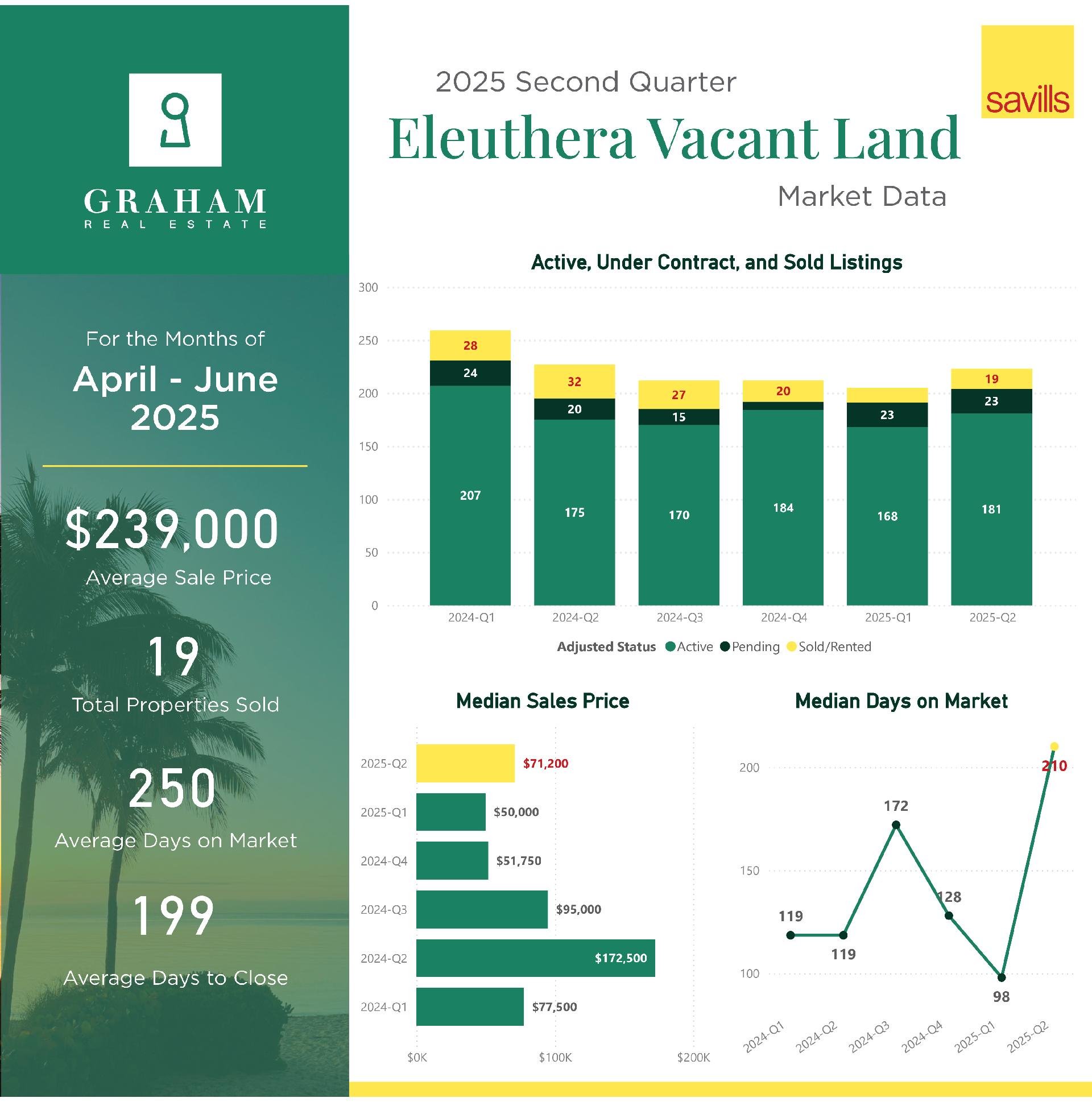

Eleuthera Land

Eleuthera Land remained strong, with 19 sales, up from 14. Median price increased to $71K, and average to $239K. Extended time on market — now at 250 days — reflects common delays in land sales tied to due diligence and financing. Nonetheless, steady transaction volume shows consistent interest.

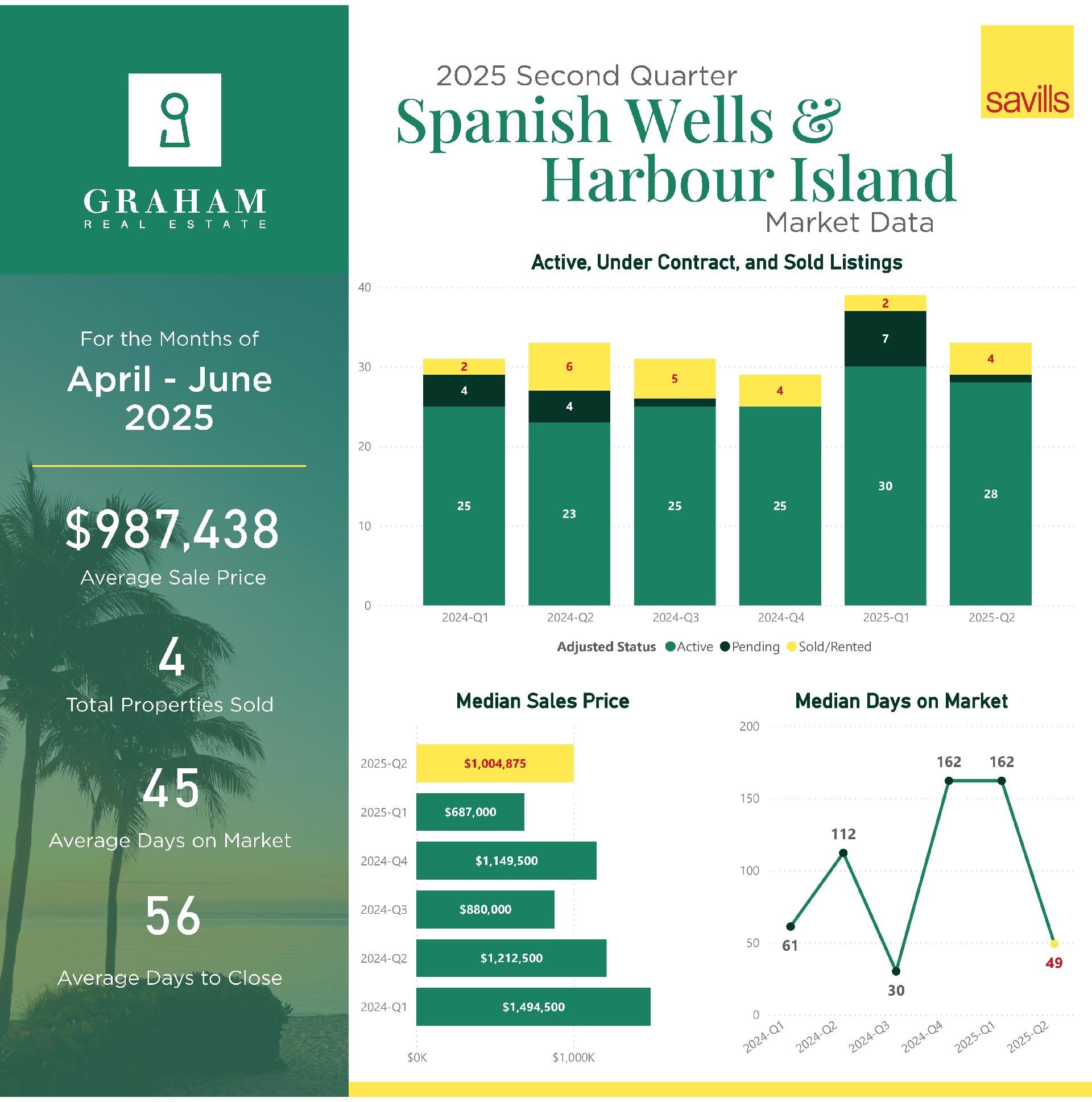

Spanish Wells & Harbour Island

Sales doubled from 2 to 4, and both average and median prices rose to just under $1M. Most notable was the significant drop in marketing time — homes sold in just 45 average days, compared to 162 in Q1. This suggests strong demand for well-located, higher-end homes in this market. The low number of pending listings may reflect limited inventory rather than a lack of demand.

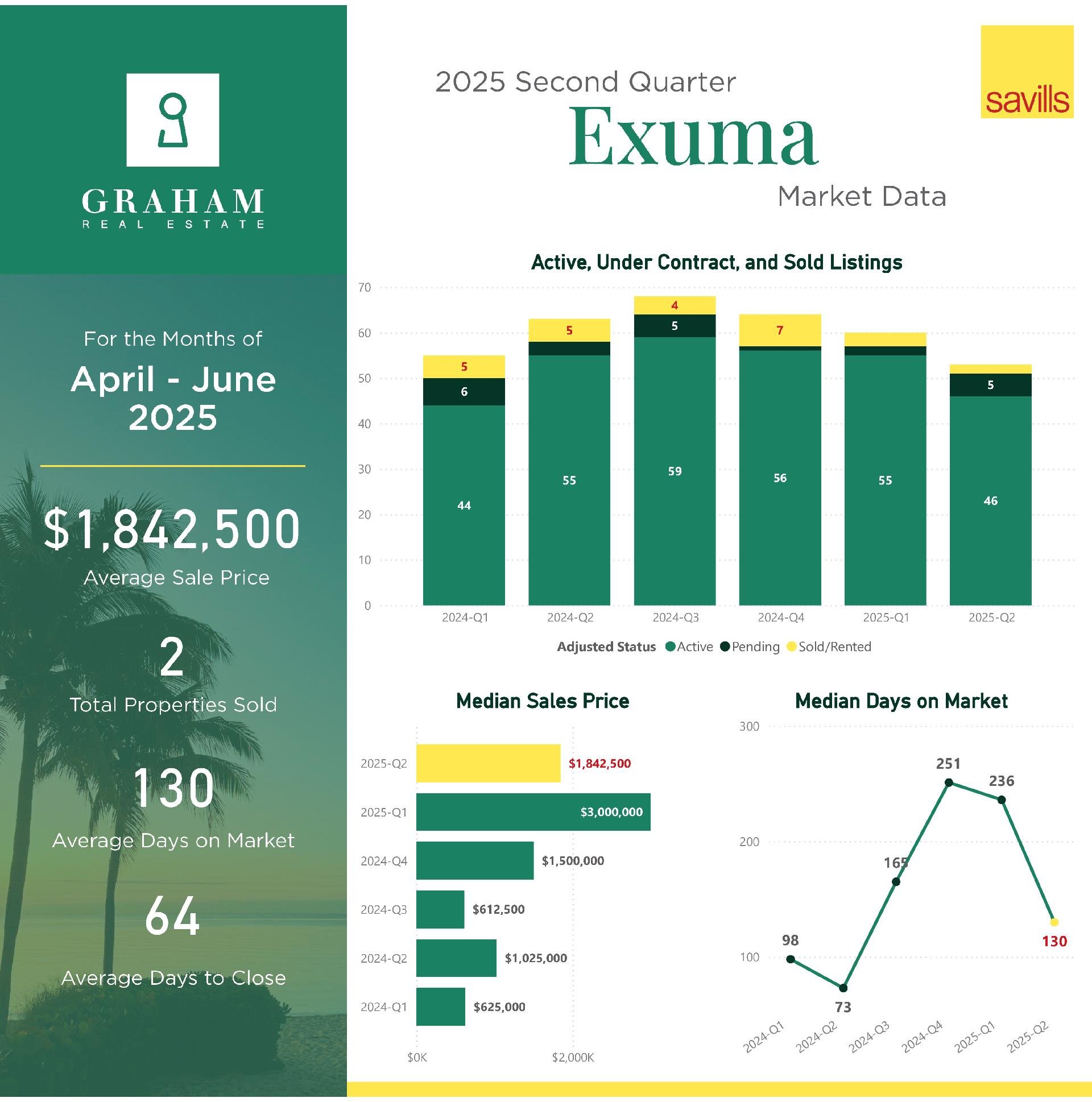

Exuma

Exuma remained slow in Q2 with only 2 completed sales, but pending listings more than doubled from 2 to 5, indicating likely pickup in Q3. The average and median prices, both at $1.84M, remain elevated, suggesting a continued focus on high-end homes. Properties are moving faster — days on market fell to 130 from over 200 — a sign that high-net-worth buyers are returning, albeit slowly.

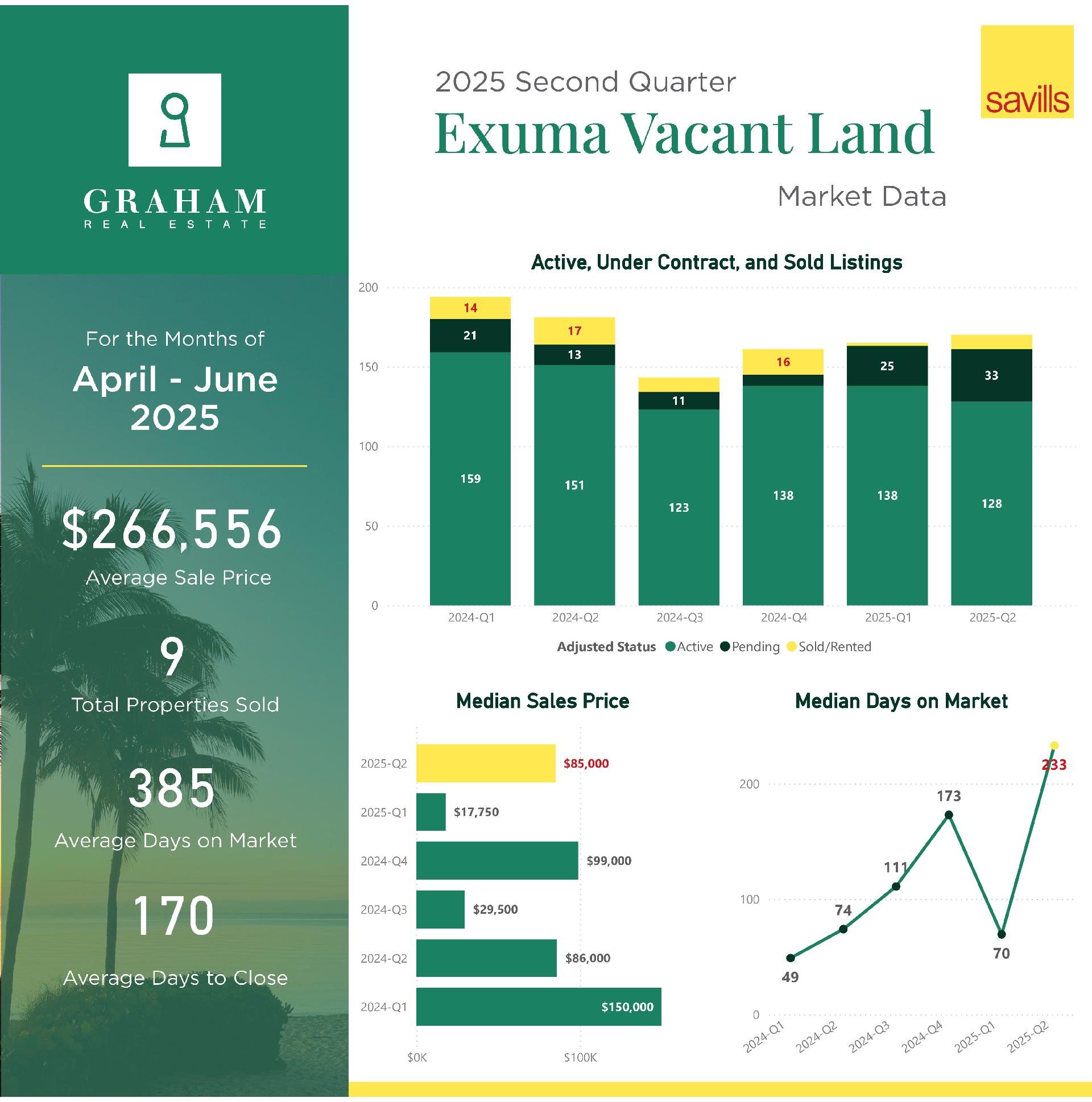

Exuma Land

Exuma Land was one of the most active land markets this quarter, jumping from 2 to 9 sales. Average price surged to $266K, up from just $17K last quarter. This dramatic swing may reflect higher-quality parcels trading hands, possibly tied to early development activity. Days on market rose to 385, suggesting older listings are finally clearing.

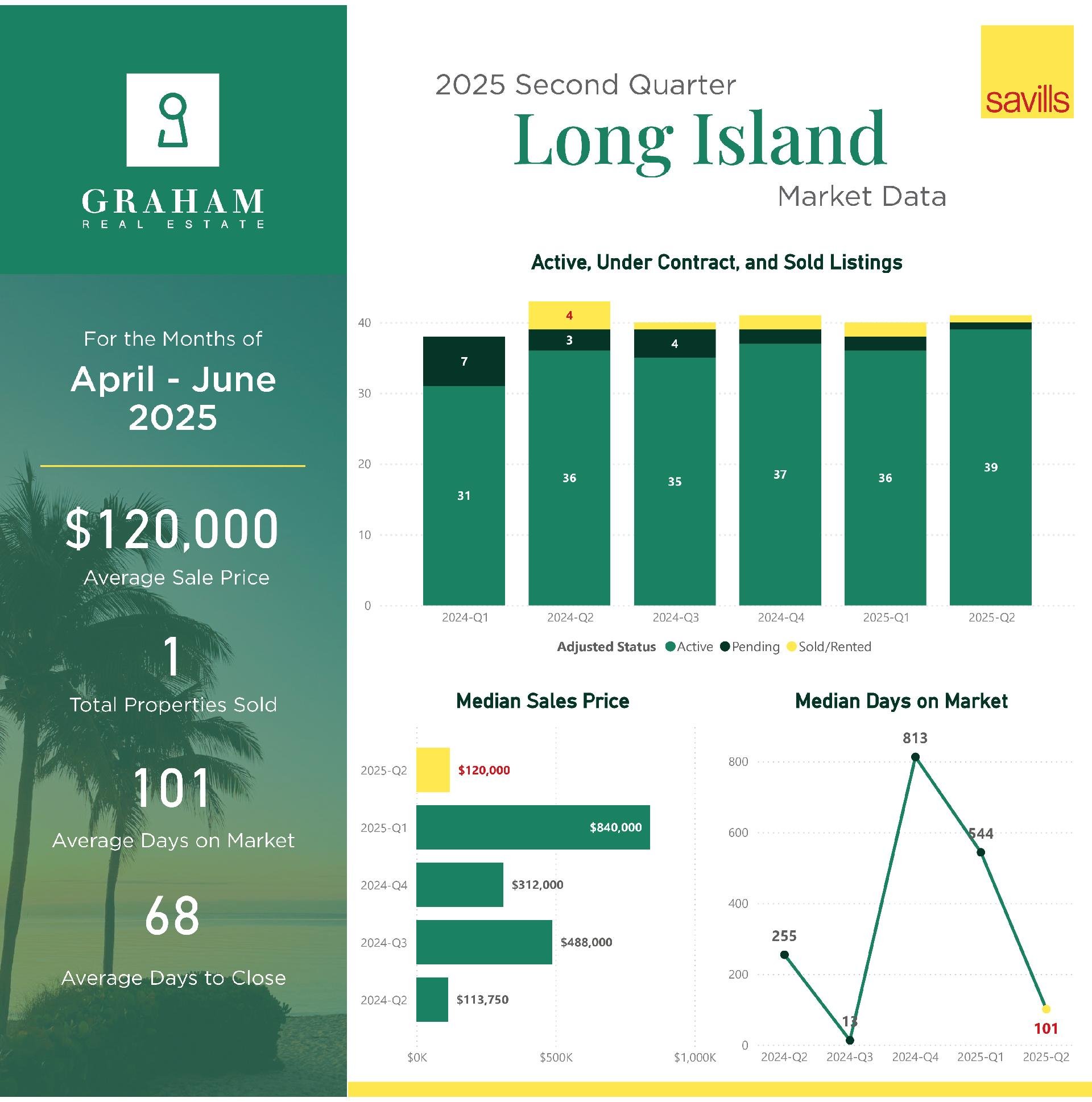

Long Island

Just 1 sale was recorded, down from 2, but with a sharply reduced days on market of 101, down from 544. The sale price was $120K, suggesting an affordable or land-adjacent home. This market remains highly seasonal and inventory-sensitive.

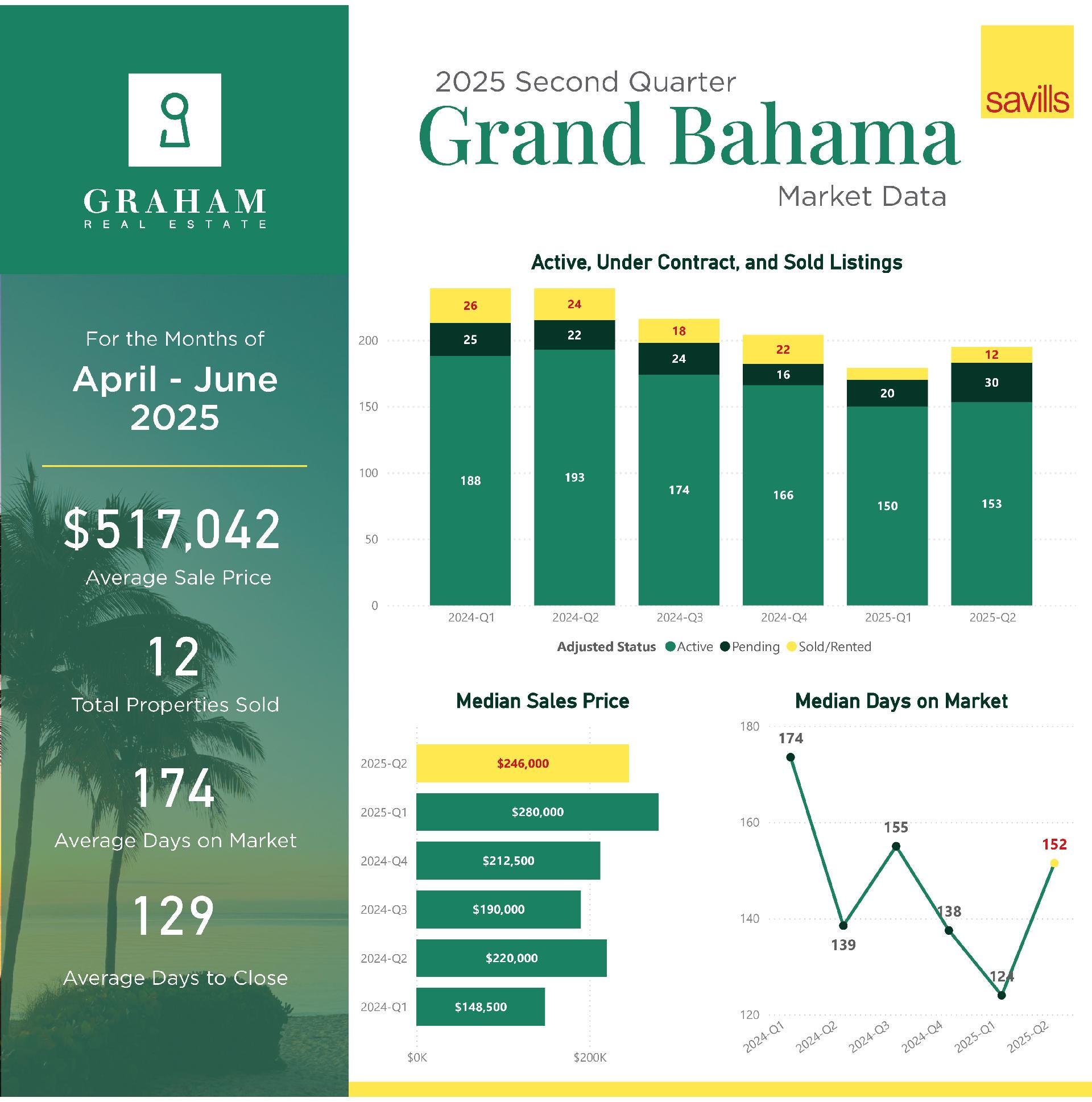

Grand Bahama

Grand Bahama continues to show signs of recovery. Pending listings rose from 20 to 30, which is a strong lead indicator. Sales dipped from 12 to 9, and prices softened slightly. Median pricing fell from $280K to $246K, reflecting a shift to more accessible inventory. Still, homes sold faster overall, suggesting that buyers are finding value and moving quickly on homes priced right.