The Bahamian residential real estate market ended Q4 2025 with increased inventory and slower transaction activity, reflecting a more measured and selective environment. Across the GRE Islands, active listings rose while pending and closed sales declined, and days on market lengthened, signaling that buyers are taking more time and exercising greater leverage. Median prices remained relatively stable despite modest softening in average sales prices, highlighting continued demand for well-priced and well-located properties. Higher-end and specialized markets experienced longer marketing timelines, while mid-range segments—particularly in New Providence and parts of Abaco—showed greater resilience when pricing aligned with current market conditions. Overall, Q4 reinforced the importance of realistic pricing and professional guidance in a market where preparation and positioning continue to drive results.

Market Coverage Note

This report focuses on residential real estate activity on the Islands of Abaco, Eleuthera, Exuma, Grand Bahama, Long Island, and New Providence. Data includes single-family homes, condominiums, apartments, and half duplexes unless otherwise noted. Vacant land and commercial properties are excluded except where specifically referenced. This scope provides a consistent view of the residential markets in which Graham Real Estate operates.

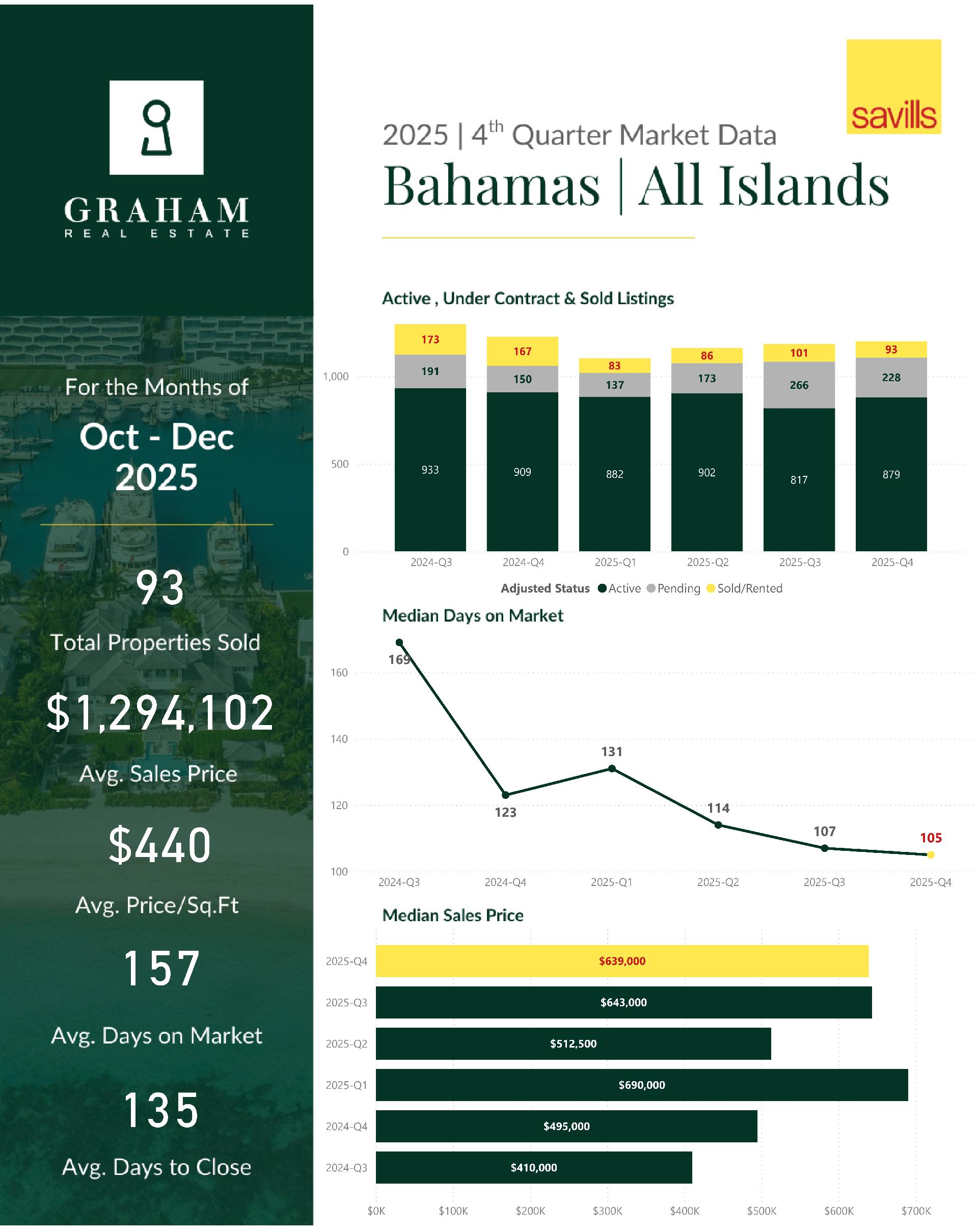

GRE Islands – Overall Market

Across the GRE Islands, Q4 2025 saw 879 active listings, up from 817 in Q3, while pending listings declined to 228 from 266 and closed sales dipped to 93 from 101. The average sales price eased slightly to $1,294,102, with the median sales price holding steady at $639,000. Properties took longer to sell, with average days on market increasing to 157 days, and price per square foot declining to $440. This reflects a market with more inventory and slower decision-making, giving buyers more time and leverage while reinforcing the importance of proper pricing for sellers.

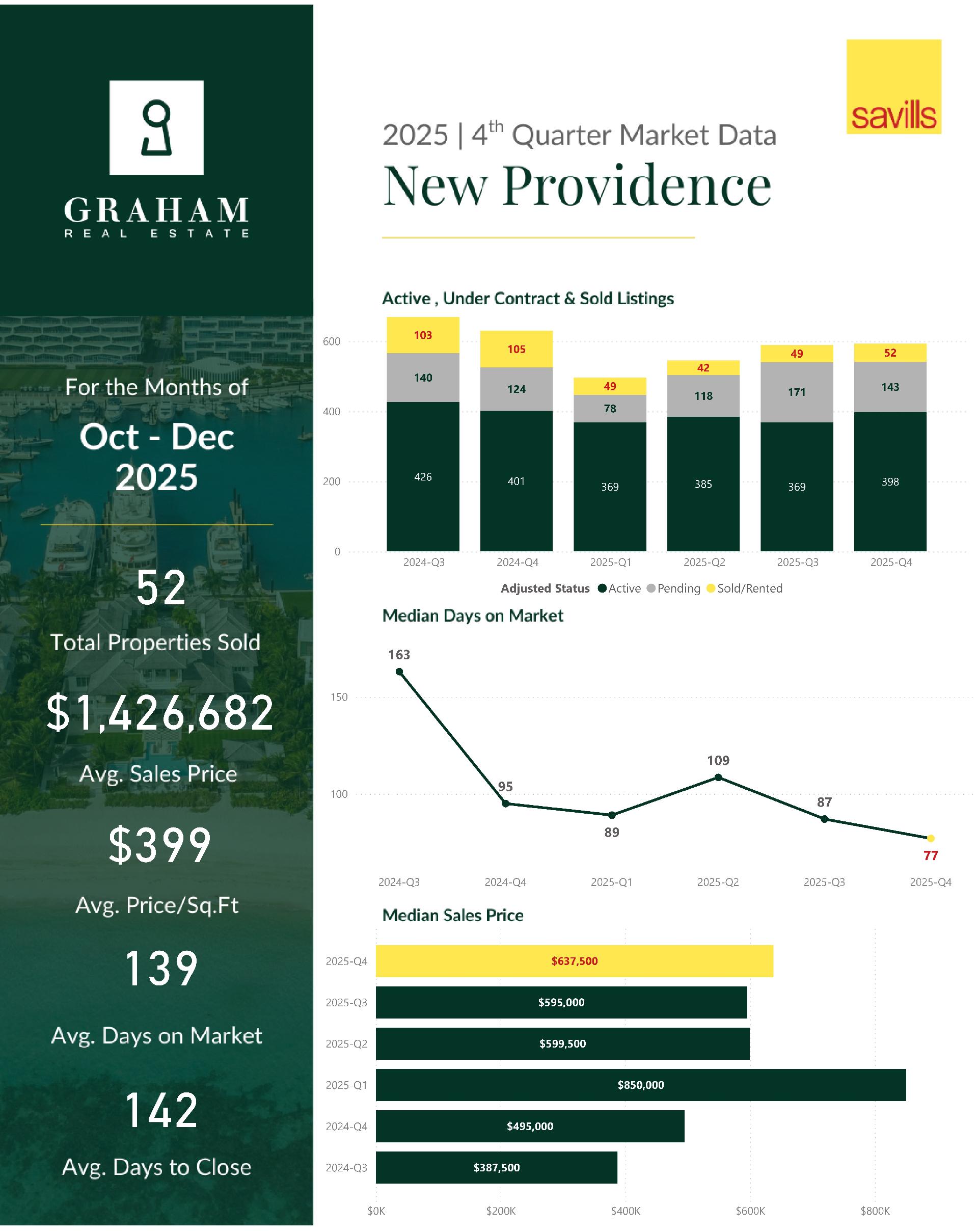

New Providence

New Providence ended Q4 with 398 active listings, up from 369, while pending listings declined to 143 and closed sales increased slightly to 52. The average sales price adjusted to $1,426,682, while the median sales price increased to $637,500. Average days on market improved to 139 days, and price per square foot declined to $399, pointing to a more balanced market with continued strength in the mid-range.

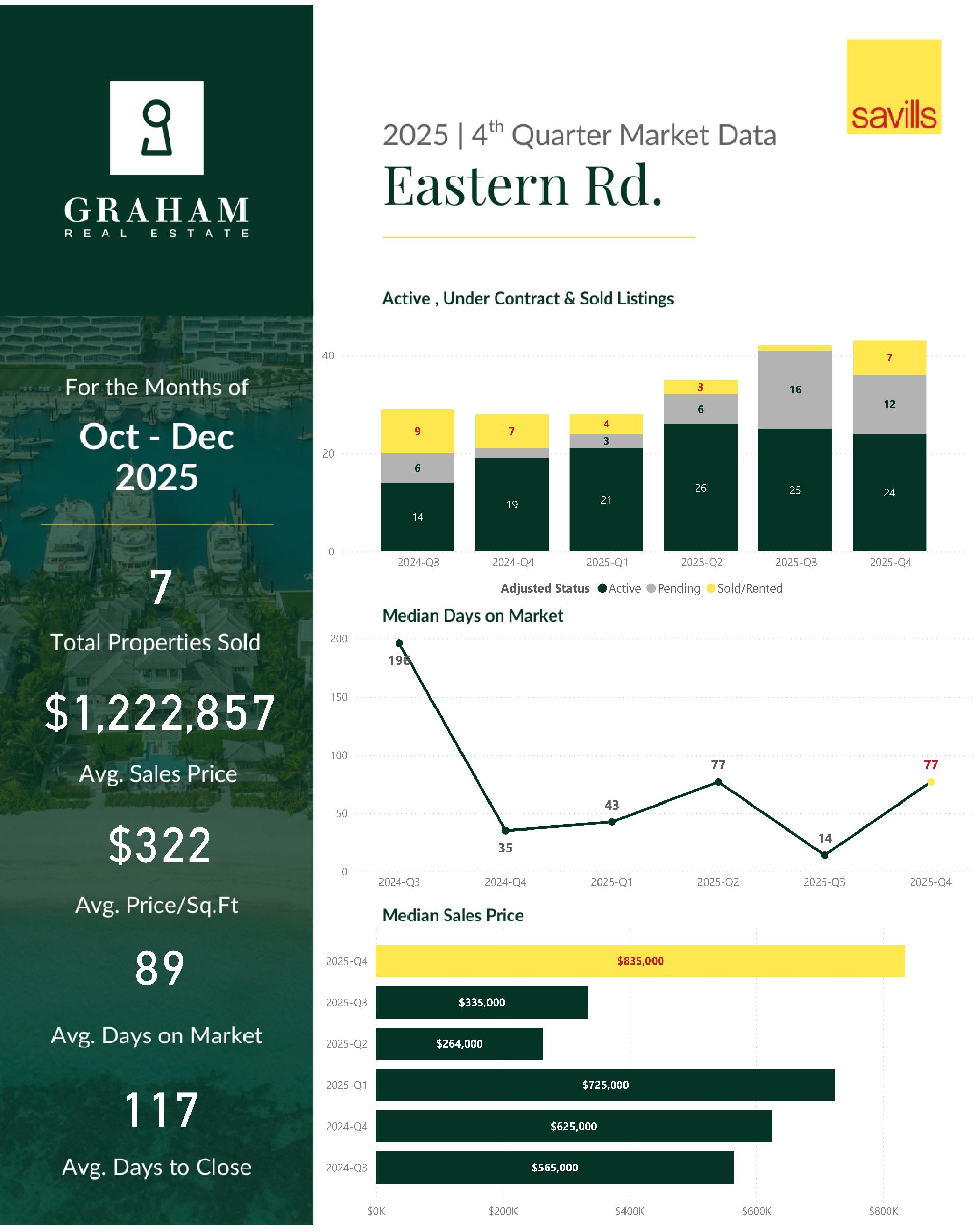

Eastern Road

Eastern Road recorded 24 active listings, 12 pending listings, and 7 closed sales, a significant increase from 1 sale in Q3. The average sales price rose to $1,222,857, with a median price of $835,000. Average days on market increased to 89 days, reflecting a return to more typical timelines after an unusually fast previous quarter.

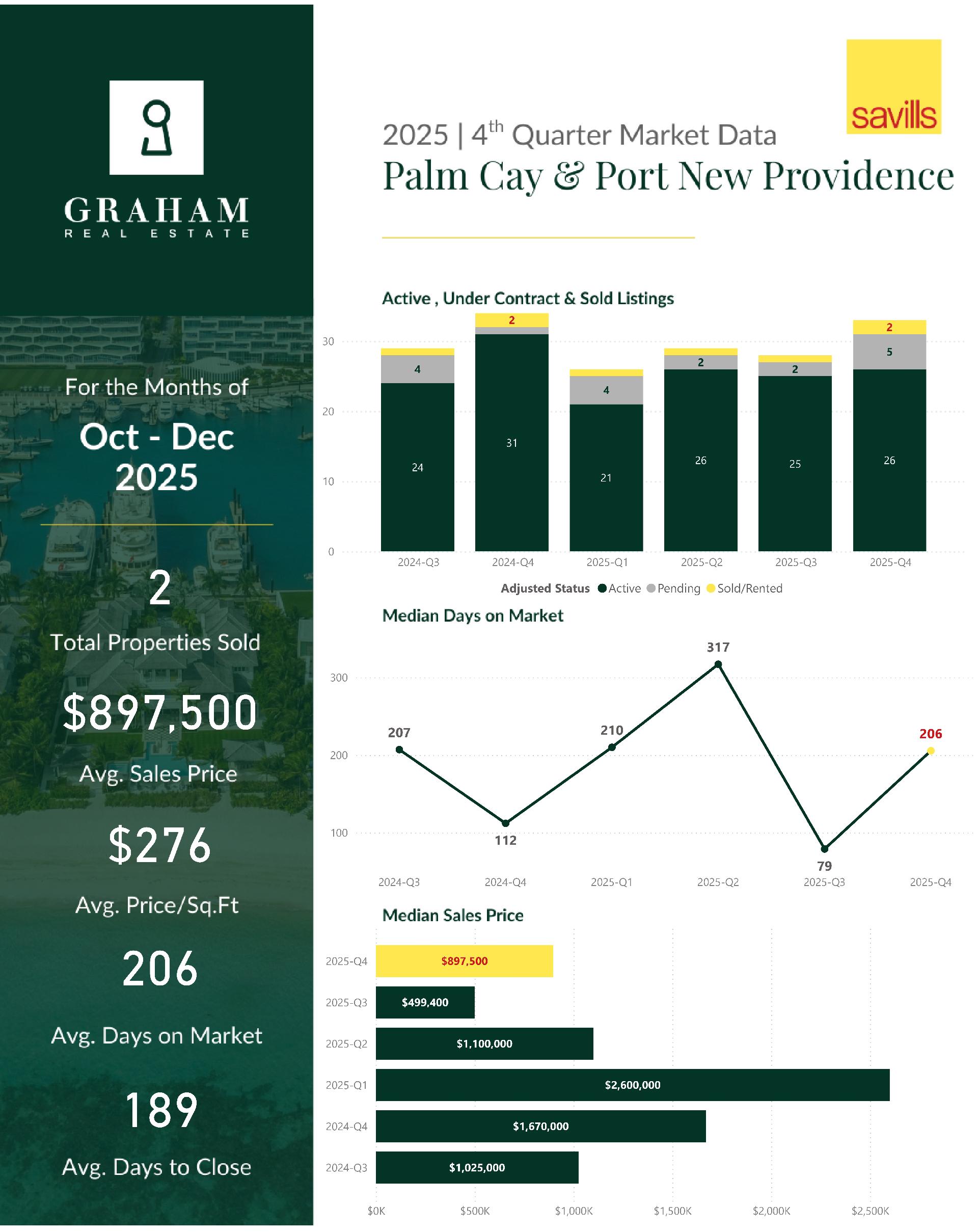

Port New Providence and Palm Cay

This area finished Q4 with 26 active listings, 5 pending listings, and 2 closed sales. Both the average and median sales price increased to $897,500, while average days on market extended to 206 days. The data reflects selective buyer activity and longer transaction timelines, particularly for marina-oriented properties.

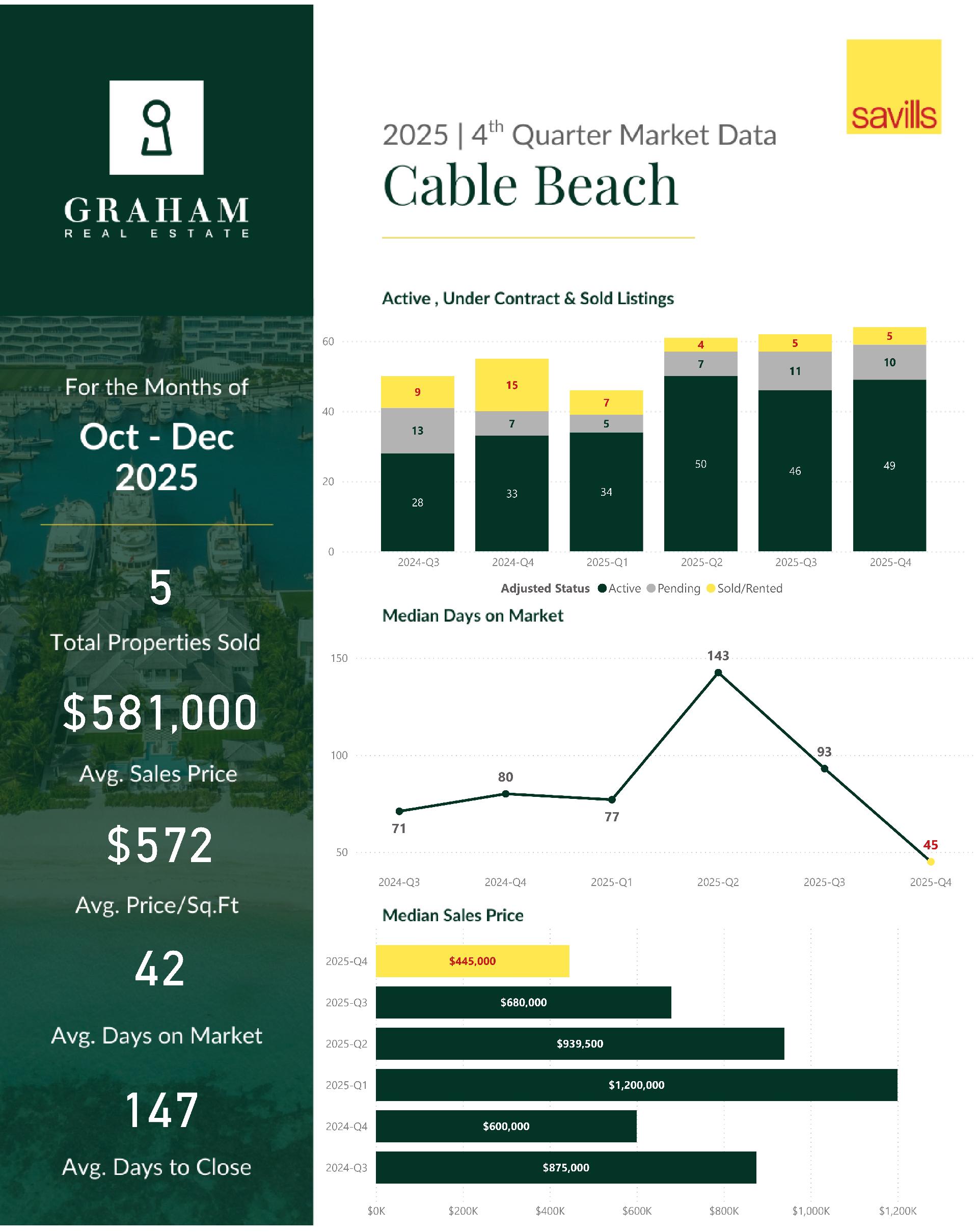

Cable Beach

Cable Beach saw 49 active listings, 10 pending listings, and 5 closed sales, consistent with Q3 volume. Pricing softened, with the average sales price declining to $581,000 and the median to $445,000. Average days on market improved to 42 days, indicating steady demand for well-priced condo and resort-area properties.

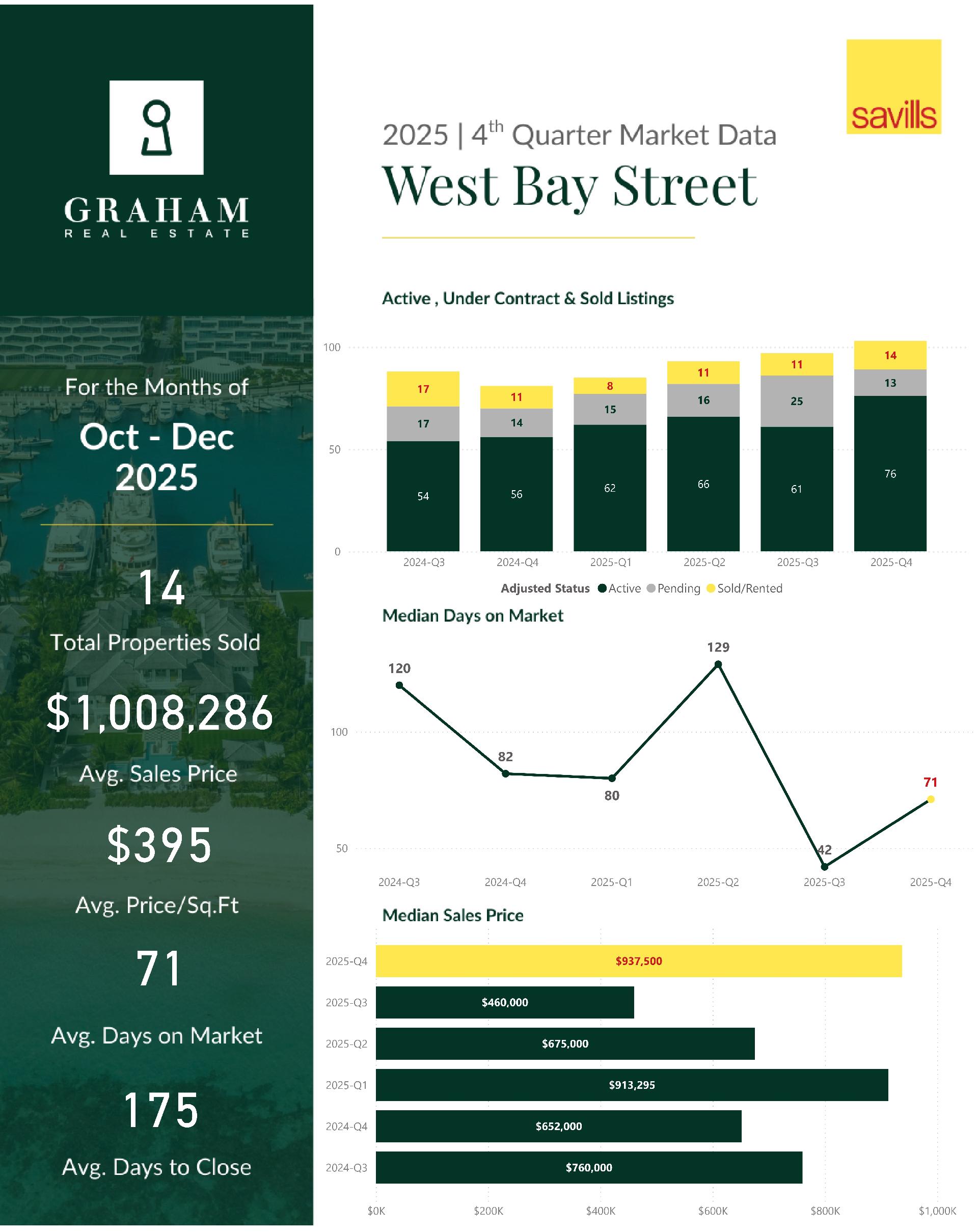

West Bay Street

West Bay Street recorded 76 active listings, 13 pending listings, and 14 closed sales, up from 11 in Q3. The average sales price increased to $1,008,286, and the median sales price rose to $937,500. Average days on market remained stable, while days to close increased, reflecting strong demand paired with more detailed due diligence.

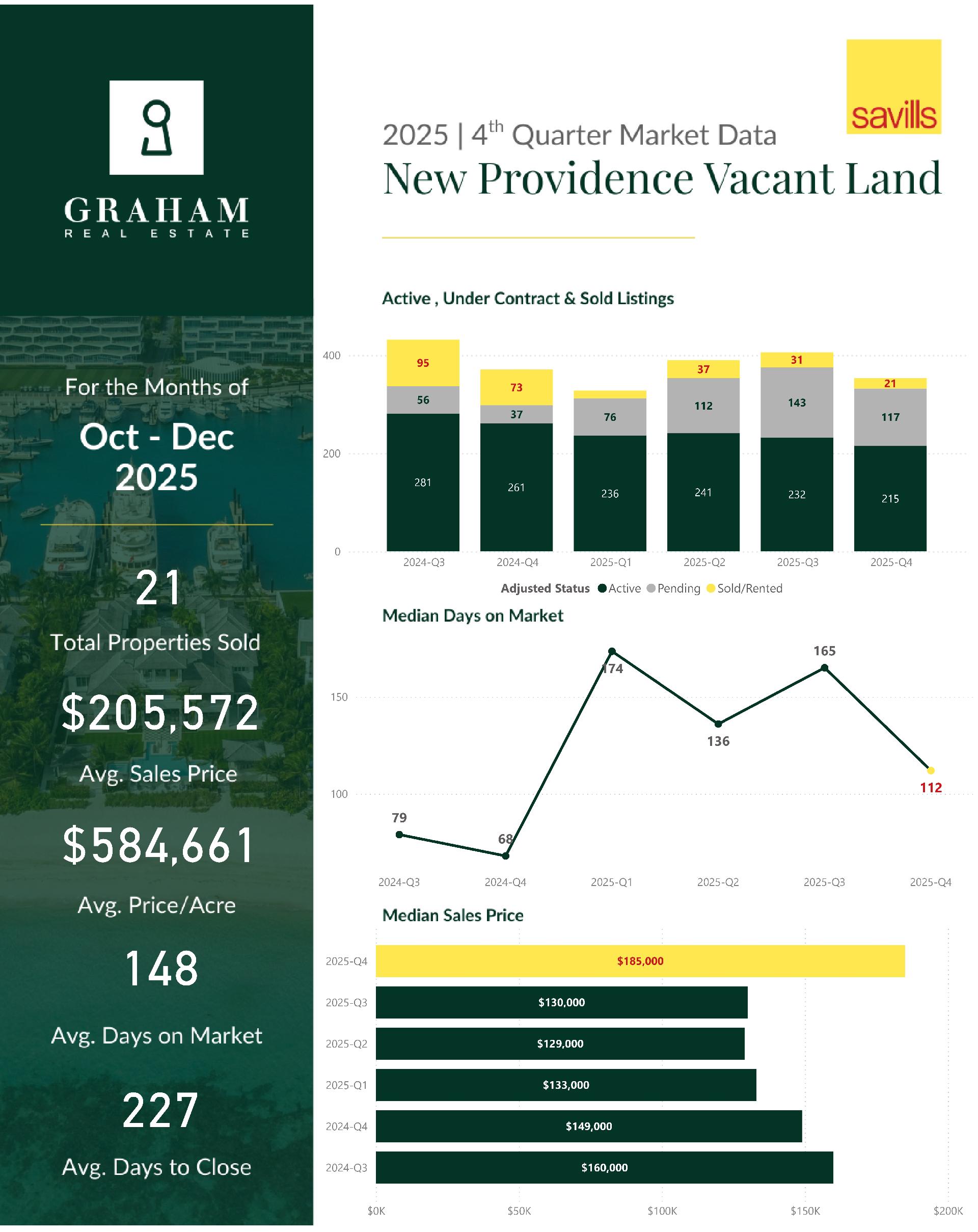

New Providence Land

New Providence land inventory declined to 215 active listings, while pending listings fell to 117 and closed sales dropped to 21. The average sales price increased to $205,572, and the median price rose to $185,000, despite average days to close extending to 227 days. Demand remains strongest for well-located residential lots.

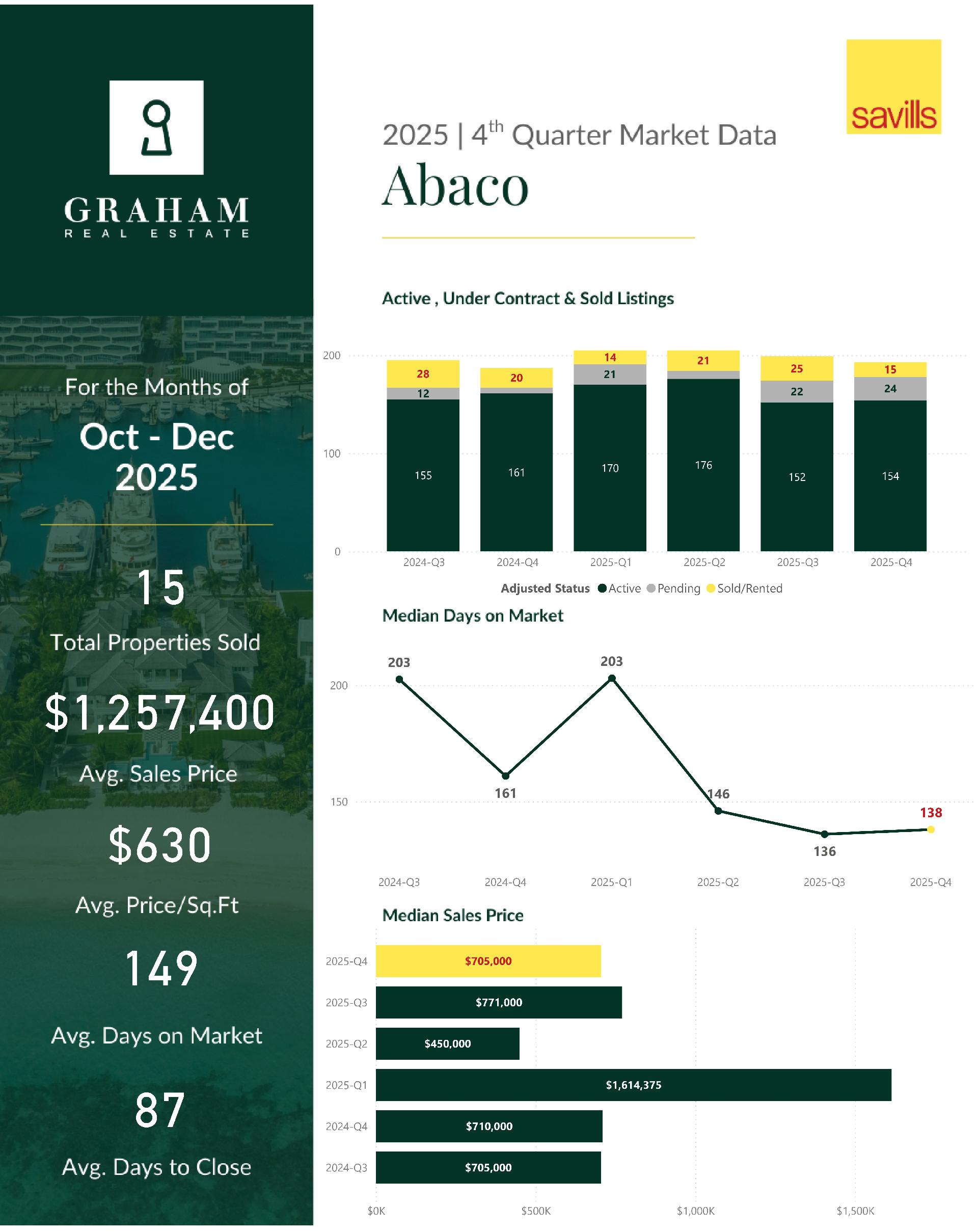

Abaco

Abaco finished Q4 with 154 active listings, similar to Q3 levels, while pending listings increased to 24 and closed sales declined to 15. The average sales price rose to $1,257,400, while the median price adjusted to $705,000. Marketing times improved, with average days on market dropping to 149 days, and average days to close shortening to 87 days. These trends suggest that while fewer transactions are closing, well-priced properties are still moving efficiently once buyers commit.

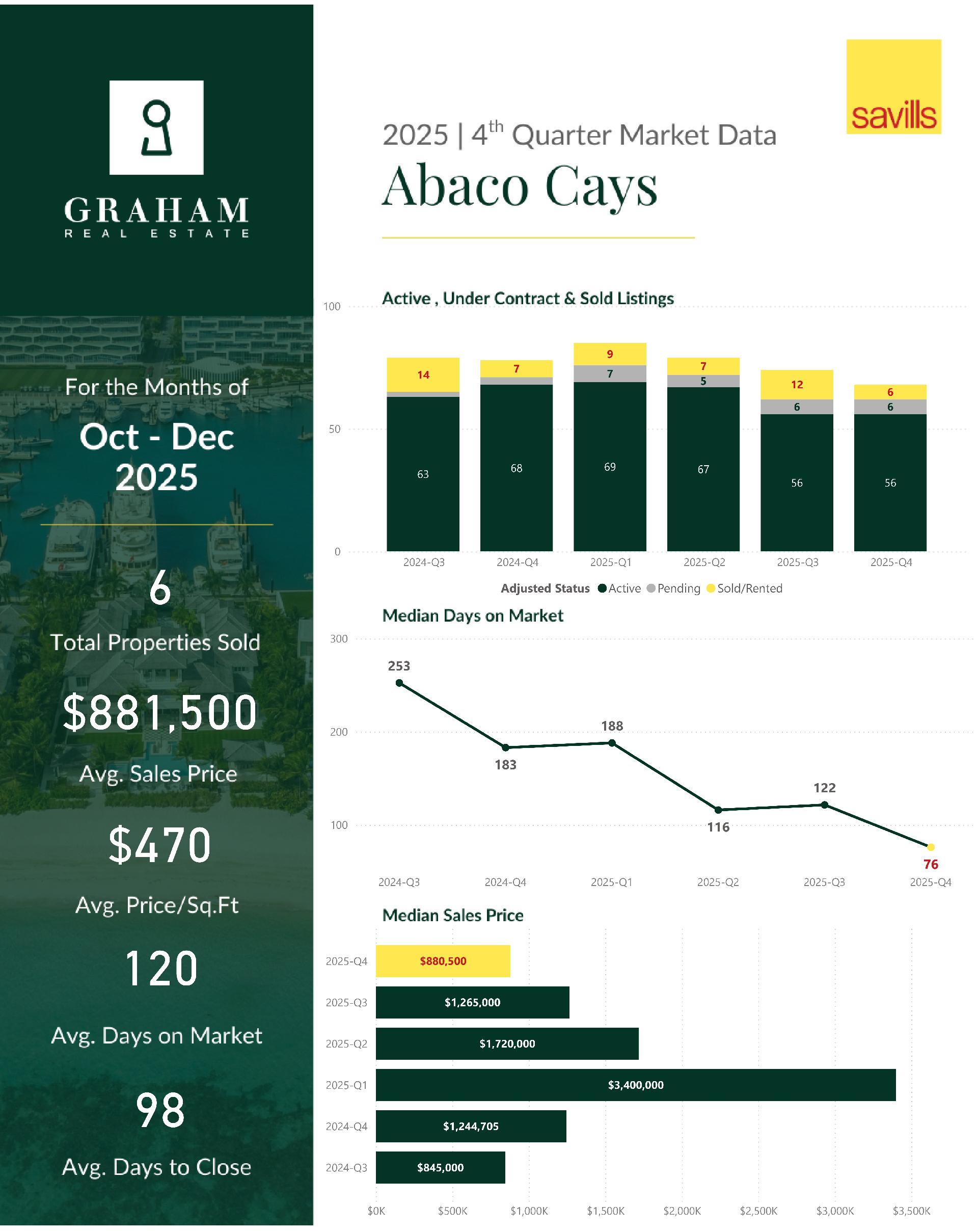

Abaco Cays

In the Abaco Cays, active listings remained flat at 56, with 6 pending listings and 6 closed sales, down from 12 in Q3. Both the average sales price of $881,500 and median sales price of $880,500 declined from Q3, largely reflecting the mix of properties sold. Encouragingly, average days on market improved to 120 days, and average days to close shortened to 98 days, indicating steady buyer interest for correctly priced offerings.

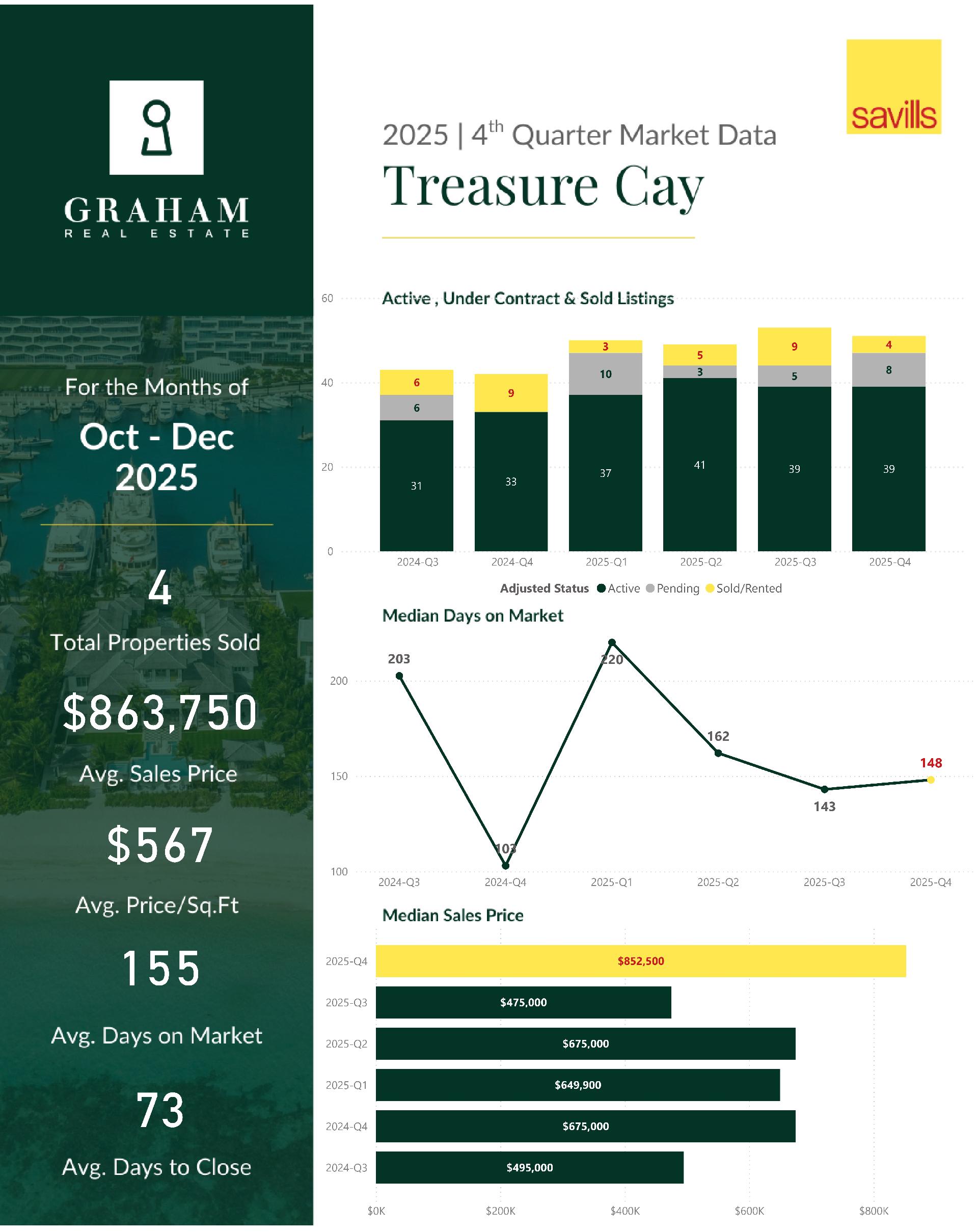

Treasure Cay

Treasure Cay ended Q4 with 39 active listings, 8 pending listings, and 4 closed sales, down from 9 in Q3. Despite fewer sales, pricing strengthened, with the average sales price rising to $863,750 and the median sales price increasing to $852,500. Average days on market declined to 155 days, and days to close improved to 73 days, suggesting increased confidence among buyers when the right property becomes available.

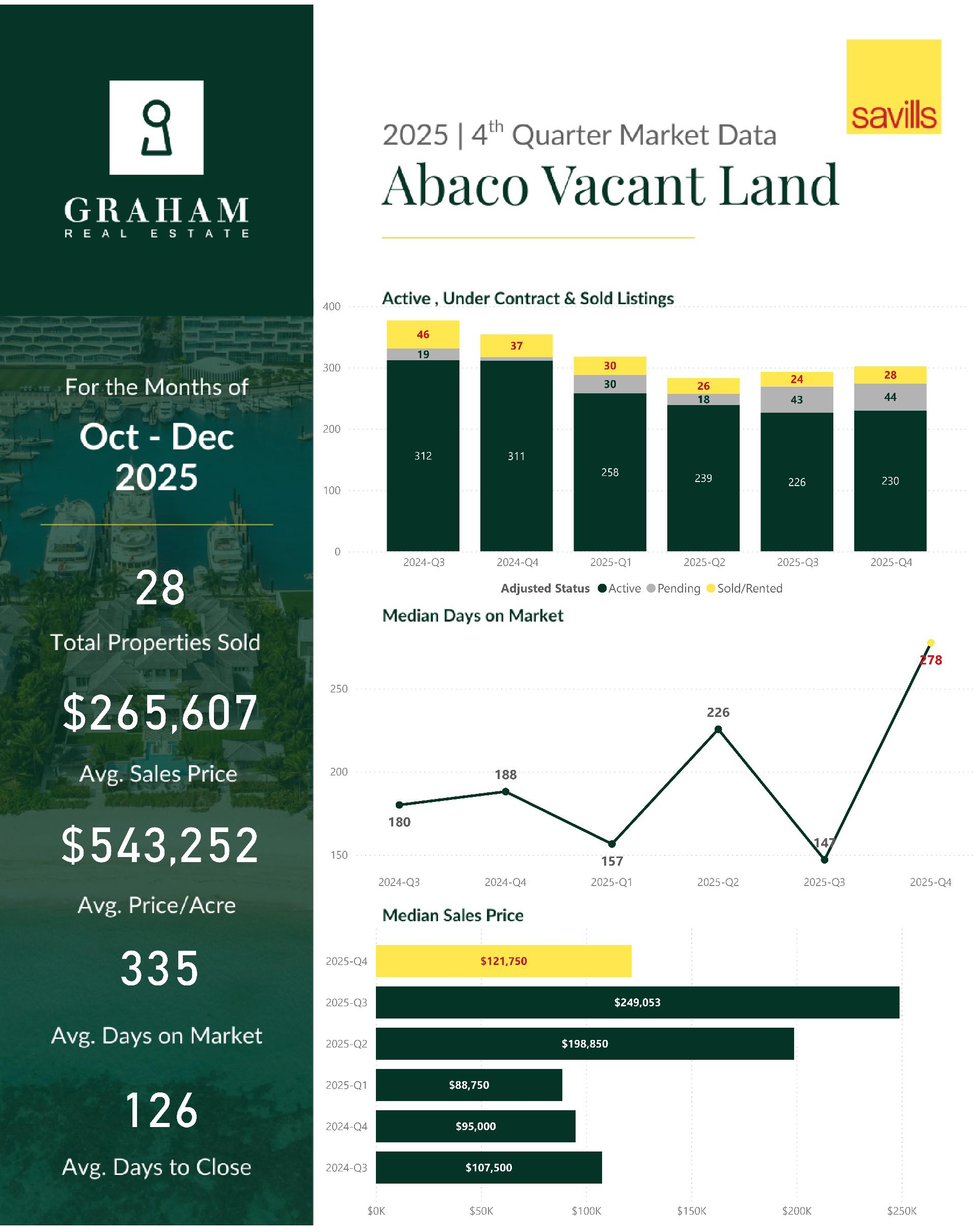

Abaco Land

Abaco land closed Q4 with 230 active listings, 44 pending listings, and 28 closed sales, up from 24 in Q3. The average sales price declined to $265,607, and the median price to $121,750, while average price per acre fell to $543,252. Longer days on market suggest buyers are active but negotiating carefully.

.

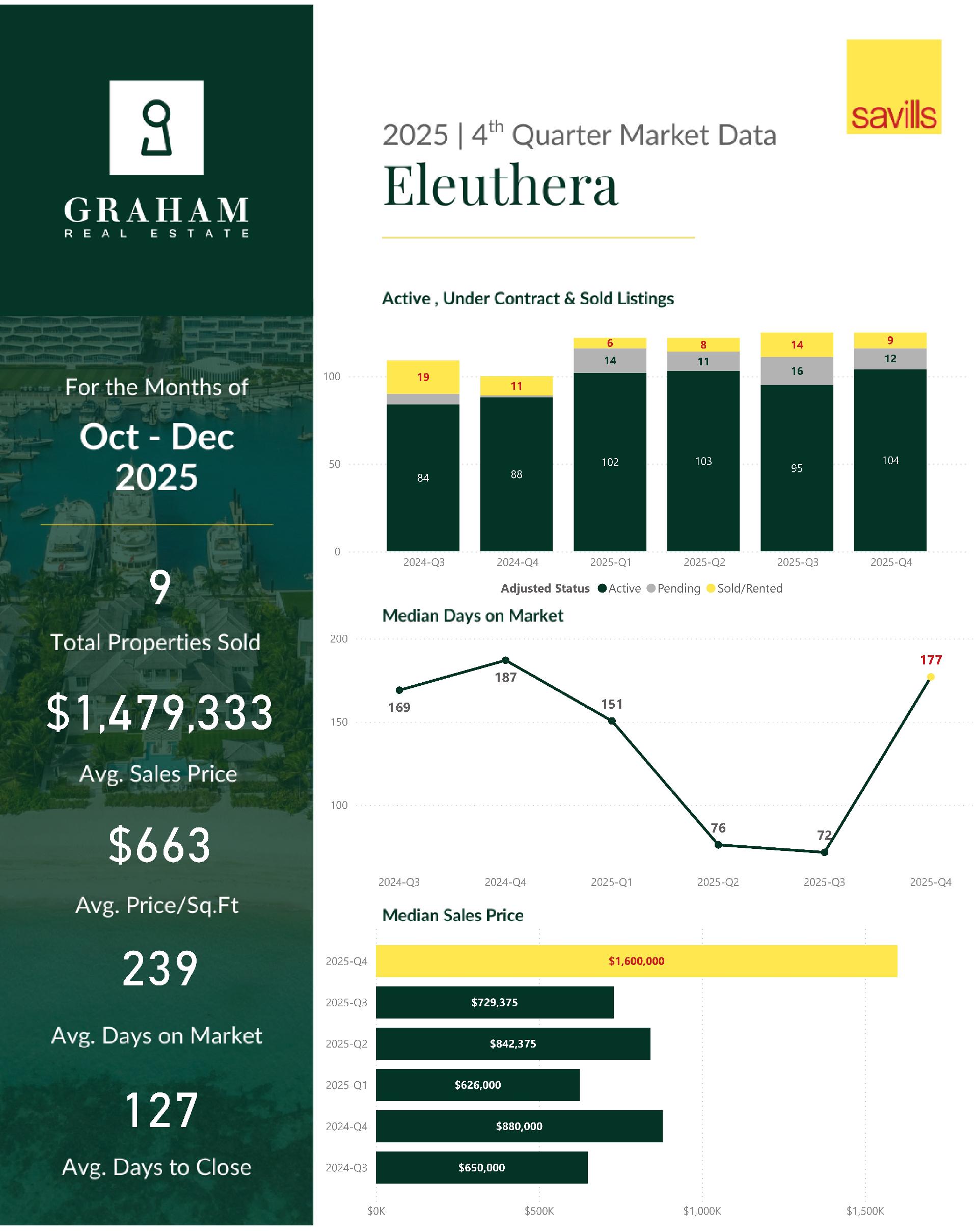

Eleuthera

Eleuthera saw inventory increase to 104 active listings, while pending listings declined to 12 and closed sales fell to 9. Pricing rose sharply, with the average sales price increasing to $1,479,333 and the median sales price reaching $1,600,000. At the same time, average days on market expanded to 239 days, reflecting longer decision timelines. This points to a market driven by higher-end transactions where buyers are taking a more measured approach.

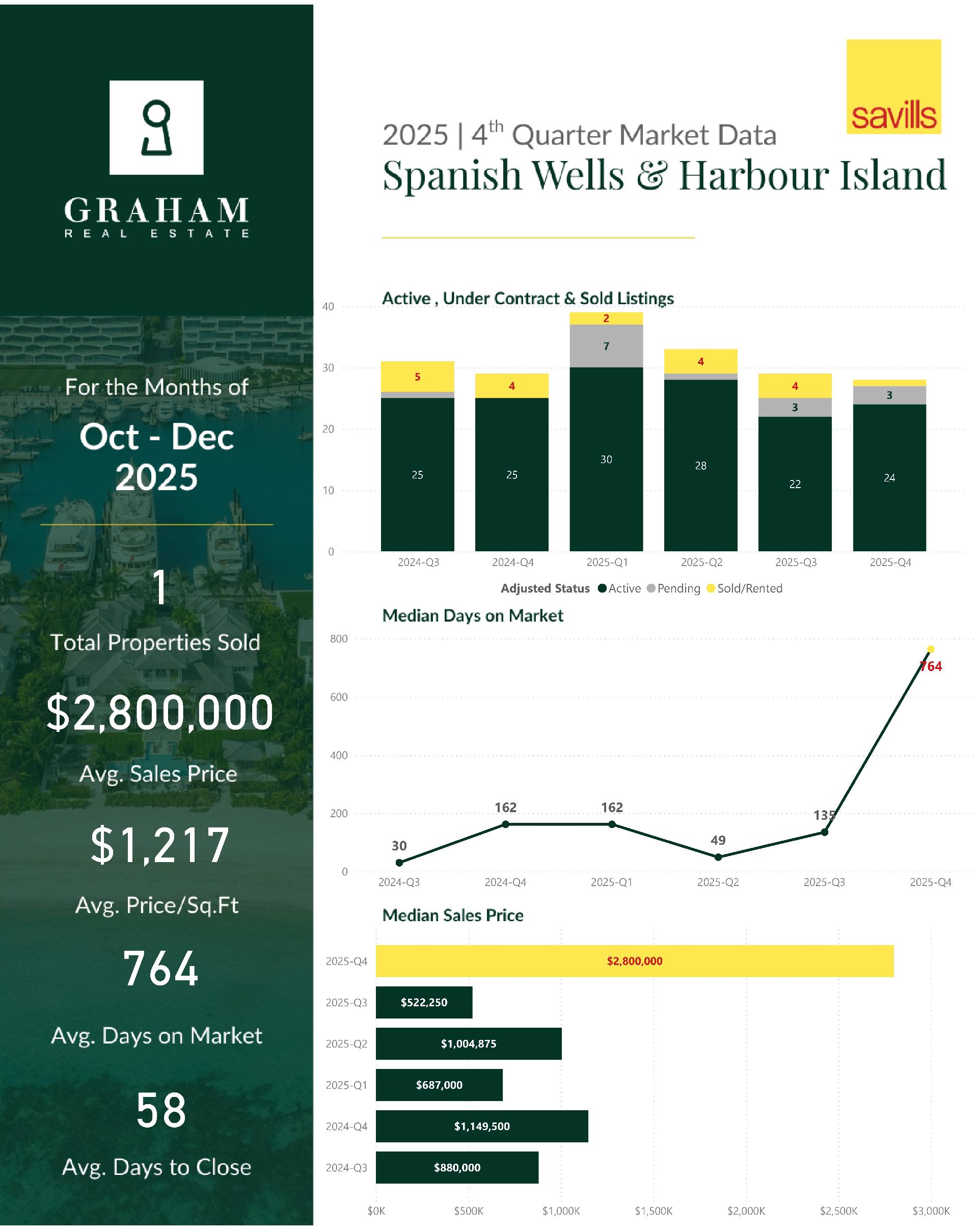

Spanish Wells and Harbour Island

Spanish Wells and Harbour Island recorded 24 active listings, 3 pending listings, and 1 closed sale in Q4. That single transaction resulted in both the average and median sales price of $2,800,000. Days on market extended significantly to 764 days, underscoring the highly specialized nature of this market. While activity is limited, demand remains for unique, high-quality properties, though marketing timelines can be lengthy.

Eleuthera Land

Eleuthera land inventory increased to 233 active listings, with 31 pending listings and 15 closed sales. Pricing softened, with the average sales price at $130,033 and median price at $55,000, while average price per acre declined to $266,899. Marketing timelines remained extended, reflecting ongoing price discovery.

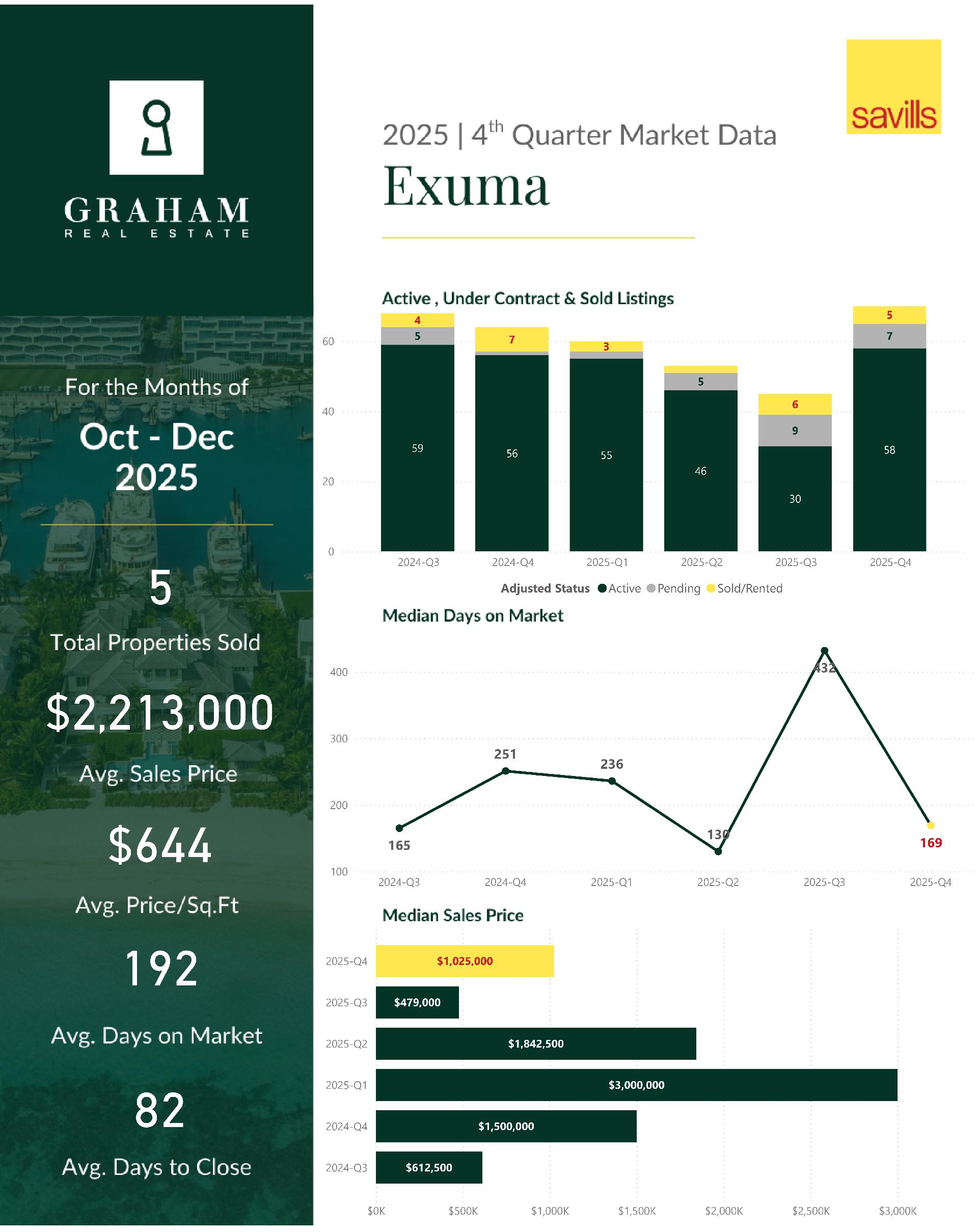

Exuma

Exuma experienced a notable increase in inventory, with 58 active listings, up from 30 in Q3. Pending listings declined to 7, while 5 properties closed. Pricing moved higher, with the average sales price rising to $2,213,000 and the median sales price to $1,025,000. Average days on market improved to 192 days, and days to close shortened to 82 days, signaling renewed buyer engagement despite higher inventory levels.

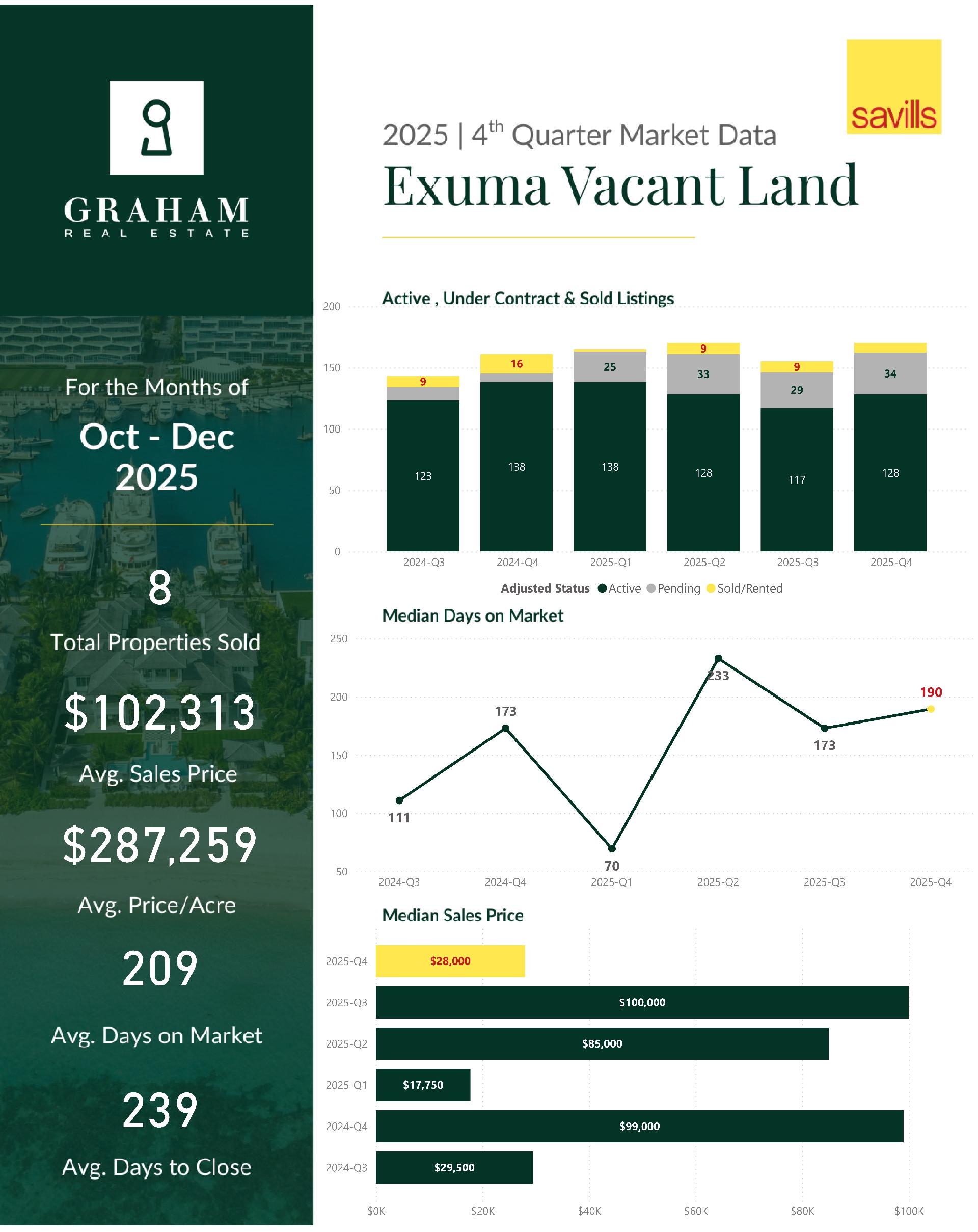

Exuma Land

Exuma land ended Q4 with 128 active listings, 34 pending listings, and 8 closed sales. The average sales price declined to $102,313, with the median price dropping to $28,000, and average price per acre falling to $287,259. While days on market improved, buyers remain value-focused and price-sensitive.

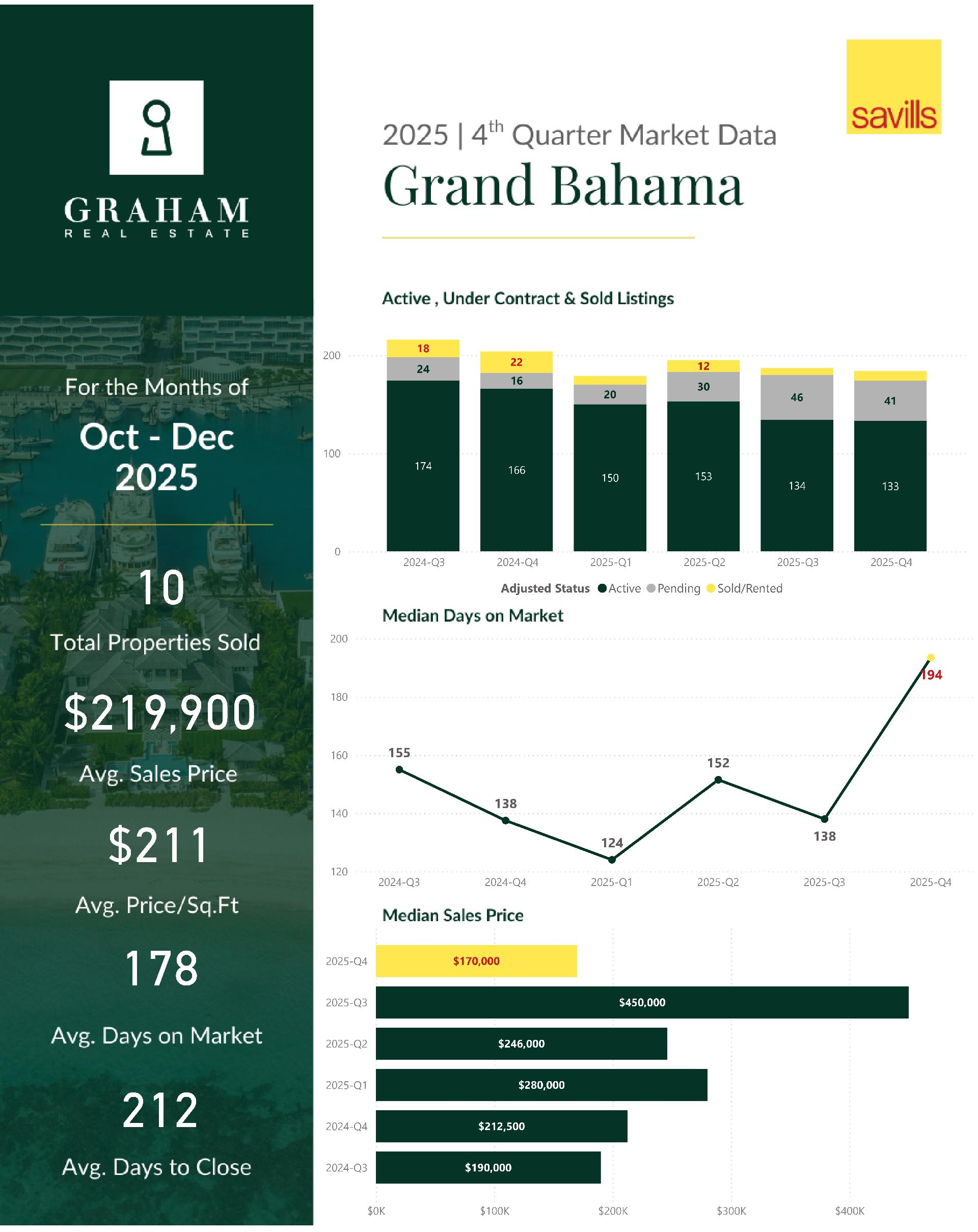

Grand Bahama

Grand Bahama closed Q4 with 133 active listings, 41 pending listings, and 10 closed sales, up from 7 in Q3. Pricing declined, with the average sales price dropping to $219,900 and the median price to $170,000. Average days on market improved slightly, but average days to close lengthened to 212 days, reflecting continued price sensitivity and extended transaction timelines.

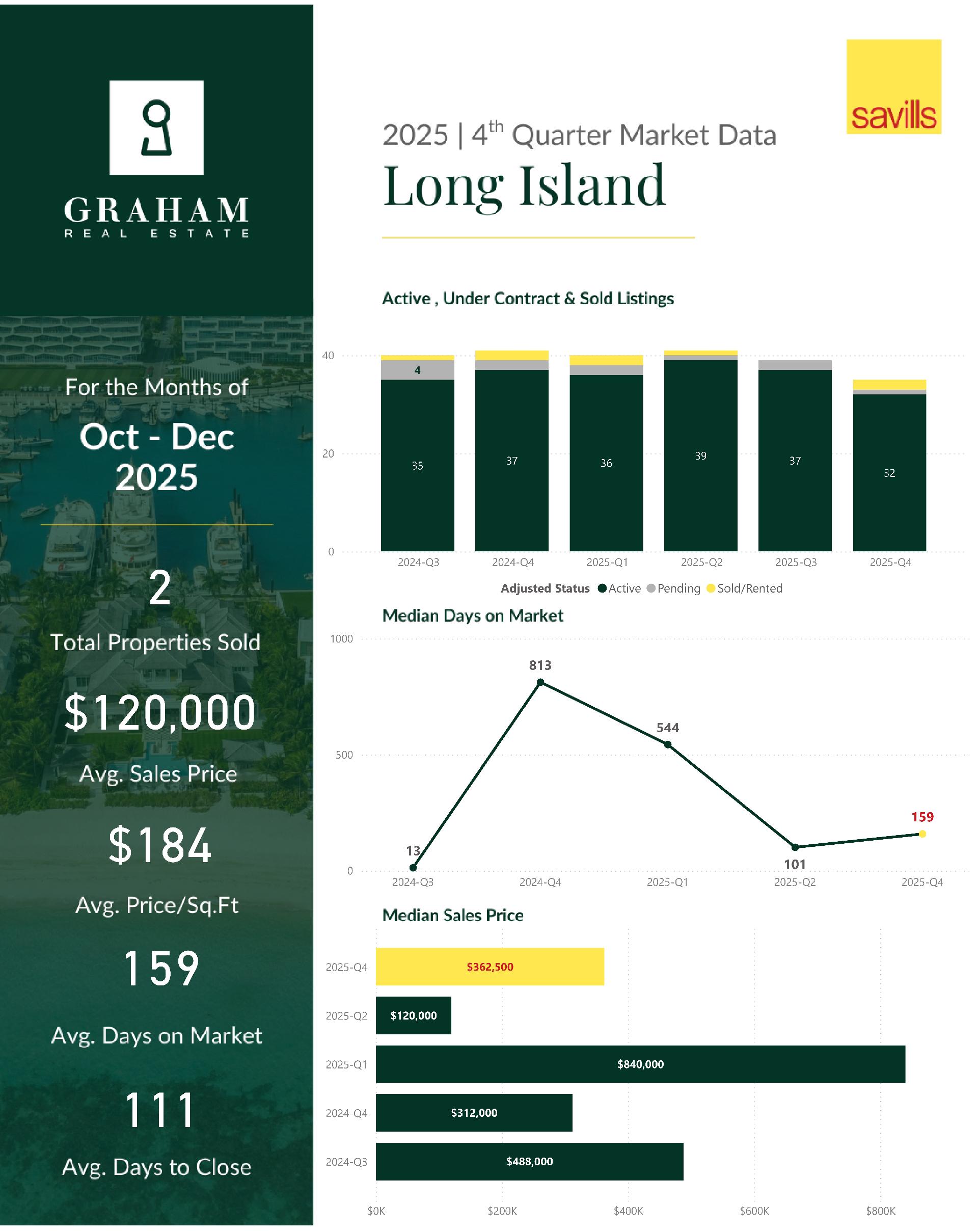

Long Island

Long Island recorded 32 active listings, 1 pending listing, and 1 closed sale in Q4 after no sales in Q3. The average and median sales price both came in at $362,500. While activity remains limited, the transaction reflects continued interest at accessible price points, with days on market at 111 days.

Conclusion

This market shows strong fundamentals supported by durable demand drivers, constrained supply dynamics, and clear opportunities for differentiated positioning. Success will favor operators who move early, design with flexibility, and align offerings tightly with evolving consumer behavior while maintaining disciplined cost structures. Execution quality and speed to market will be decisive advantages.