The Bahamian residential real estate market opened Q1 2026 with rising inventory and a strengthening pending pipeline, while closed sales moderated from Q4 2025 levels. Active listings increased across the Graham Real Estate (GRE) Islands as more sellers entered the market, and pending sales rose, pointing to a more active closing quarter ahead. Average sales prices moved higher in several key markets, driven by a concentration of premium transactions, while days on market extended across most islands, reflecting buyers taking more time to evaluate their options. Mid-range segments on New Providence continued to show resilience, and high-end markets in Eleuthera, Harbour Island, and Treasure Cay recorded notable pricing strength. Overall, Q1 reinforced that well-priced, well-positioned properties continue to attract committed buyers across all segments of the market.

Market Coverage Note This report focuses on residential real estate activity on the Islands of Abaco, Eleuthera, Exuma, Grand Bahama, Long Island, and New Providence. Data include single-family homes, condominiums, apartments, and half-duplexes unless otherwise noted. Vacant land and commercial properties are excluded except where specifically referenced. This scope provides a consistent view of the residential markets in which Graham Real Estate operates.

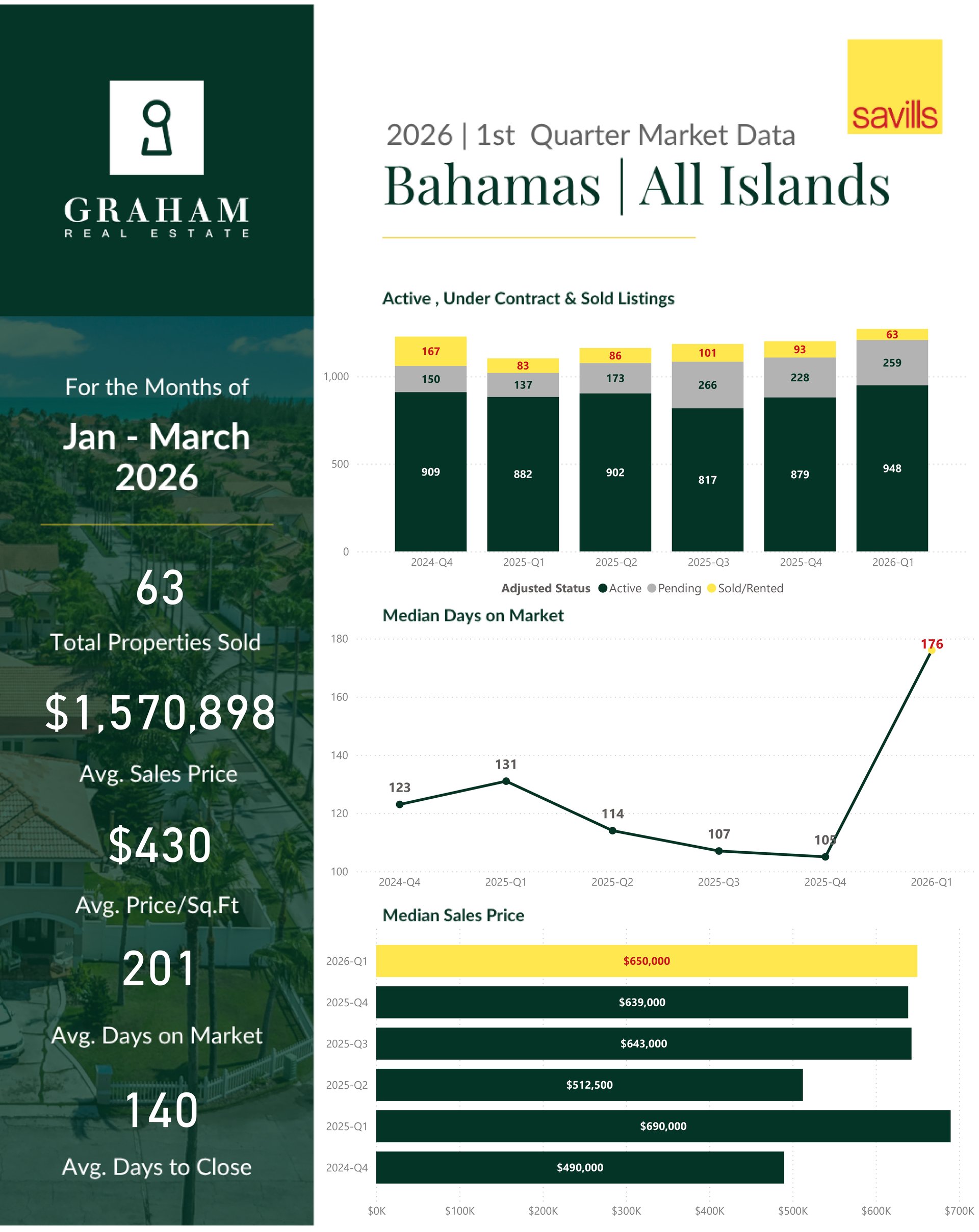

GRE Islands – Overall Market

Across the GRE Islands, Q1 2026 recorded 948 active listings, up from 879 in Q4 2025, while pending sales increased to 259 from 228 and closed sales declined to 63 from 93. The average sales price rose to $1,570,898, with the median sales price holding near $650,000. Average days on market extended to 201 days, and price per square foot declined to $430. The rise in pending activity against a backdrop of slower closings suggests that buyer engagement is growing, with transaction completions expected to follow in Q2.

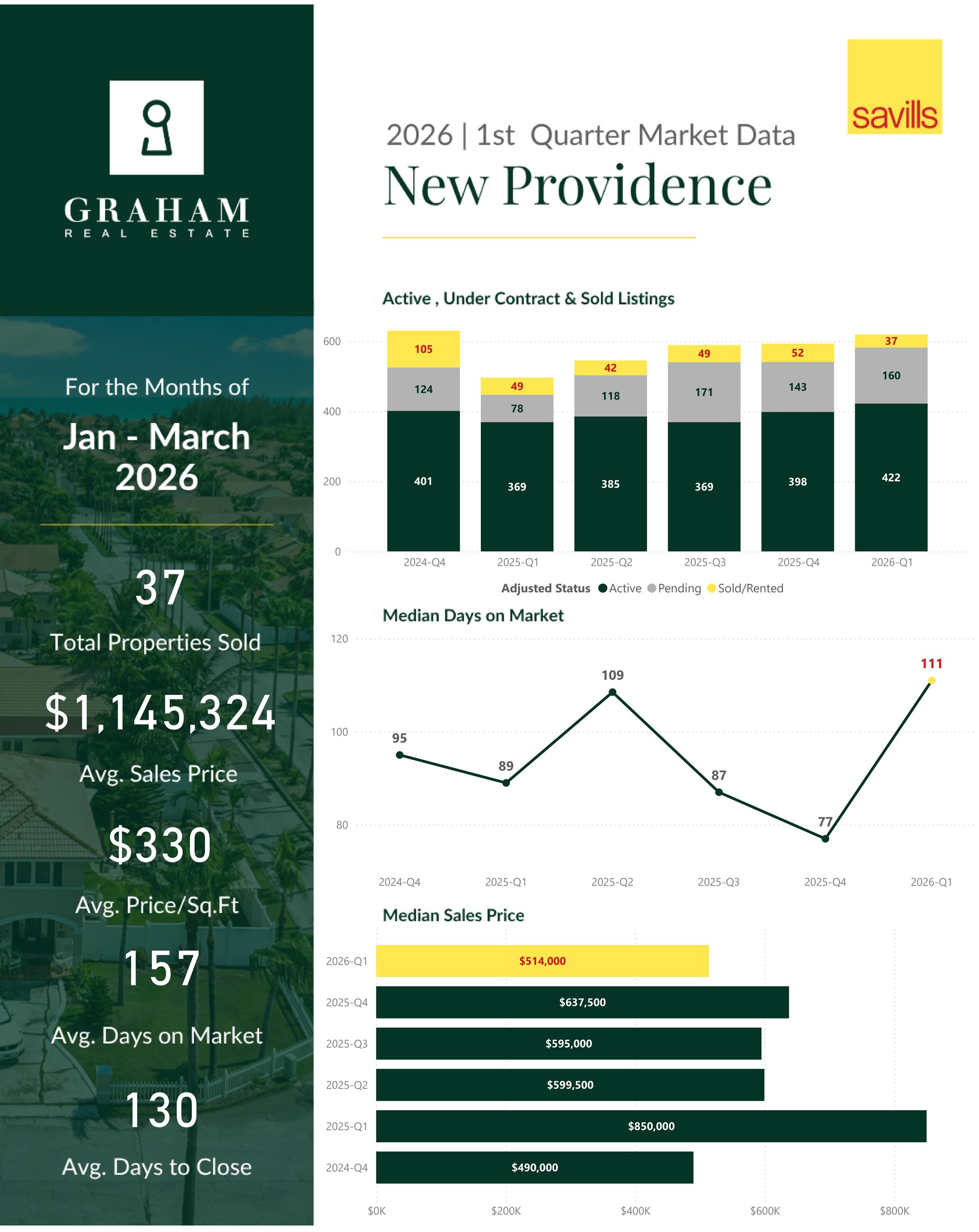

New Providence – Overall

New Providence recorded 422 active listings in Q1, up from 398 in Q4, while pending sales increased to 160 and closed sales declined to 37 from 52. The average sales price was $1,145,324, with a median of $514,000. Average days on market were 157 days, and price per square foot came in at $330, reflecting a market with a healthy forward pipeline and continued demand across the mid-range.

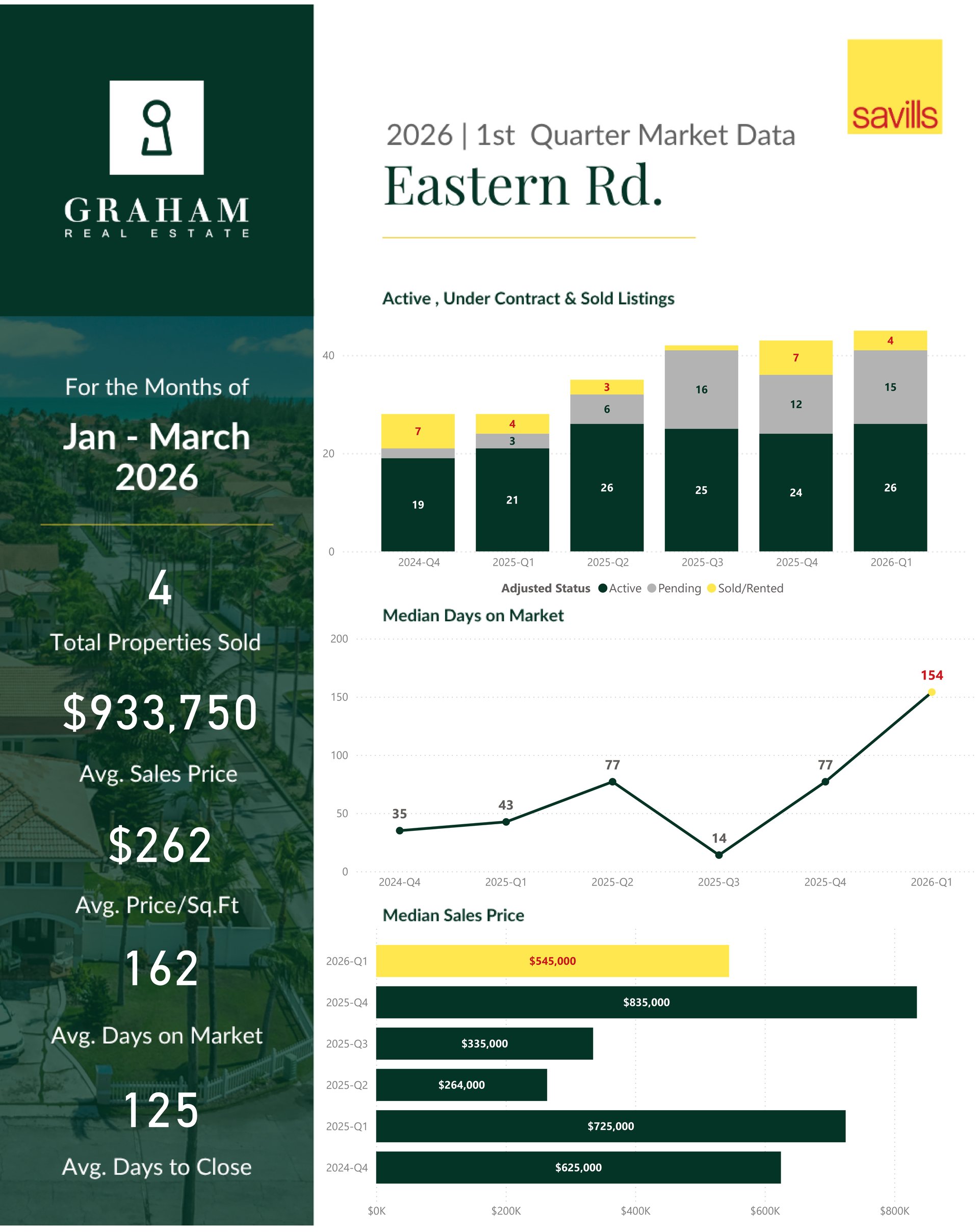

Eastern Road

Eastern Road recorded 26 active listings, 15 pending listings, and 4 closed sales in Q1. The average sales price was $933,750, with a median of $545,000. Average days on market were 162 days and average days to close 125 days, reflecting steady buyer activity in this corridor.

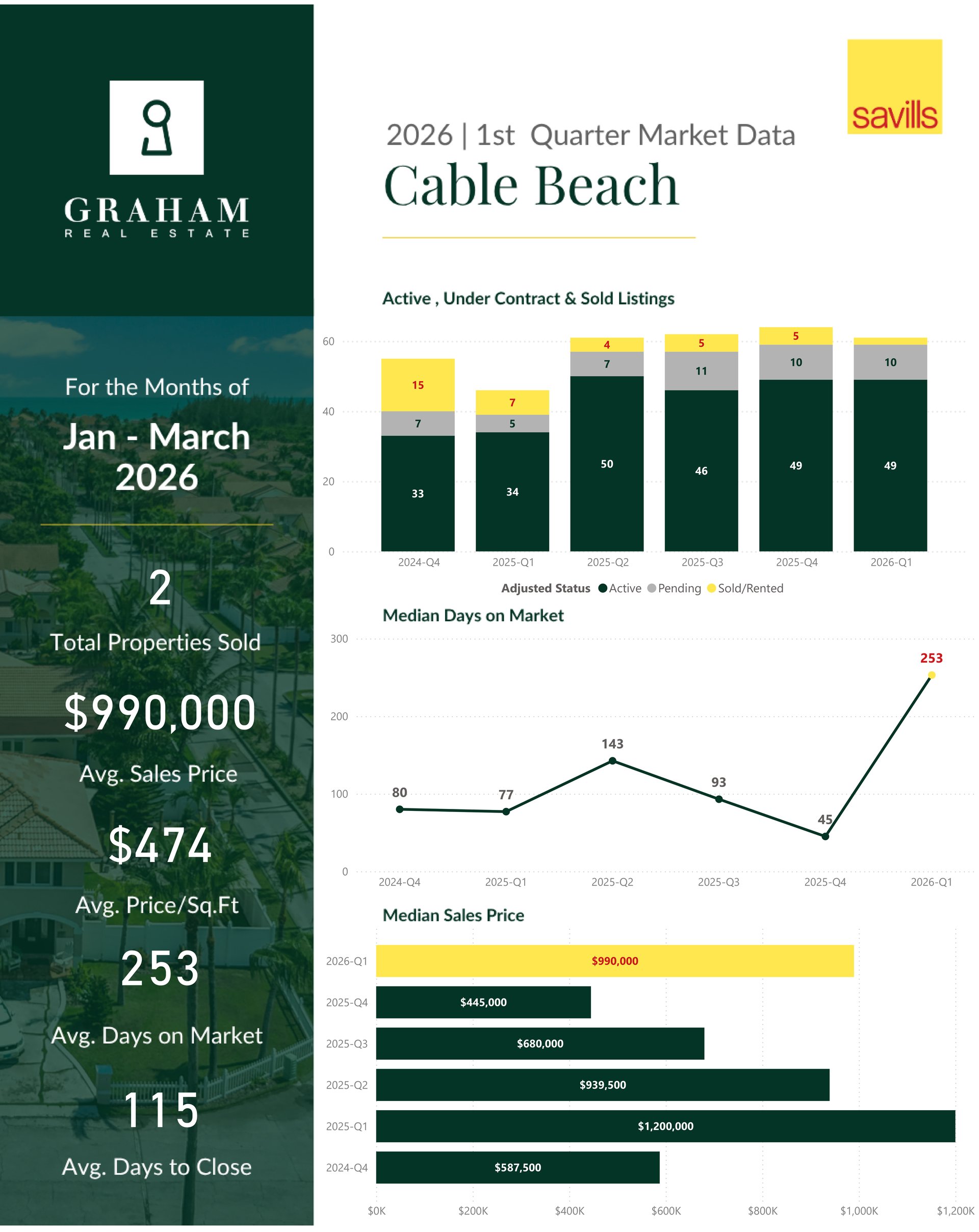

Cable Beach

Cable Beach saw 49 active listings, 10 pending listings, and 2 closed sales in Q1. The average and median sales price both came in at $990,000. Average days on market extended to 253 days, reflecting more typical marketing timelines for condo and resort-area properties at this price level.

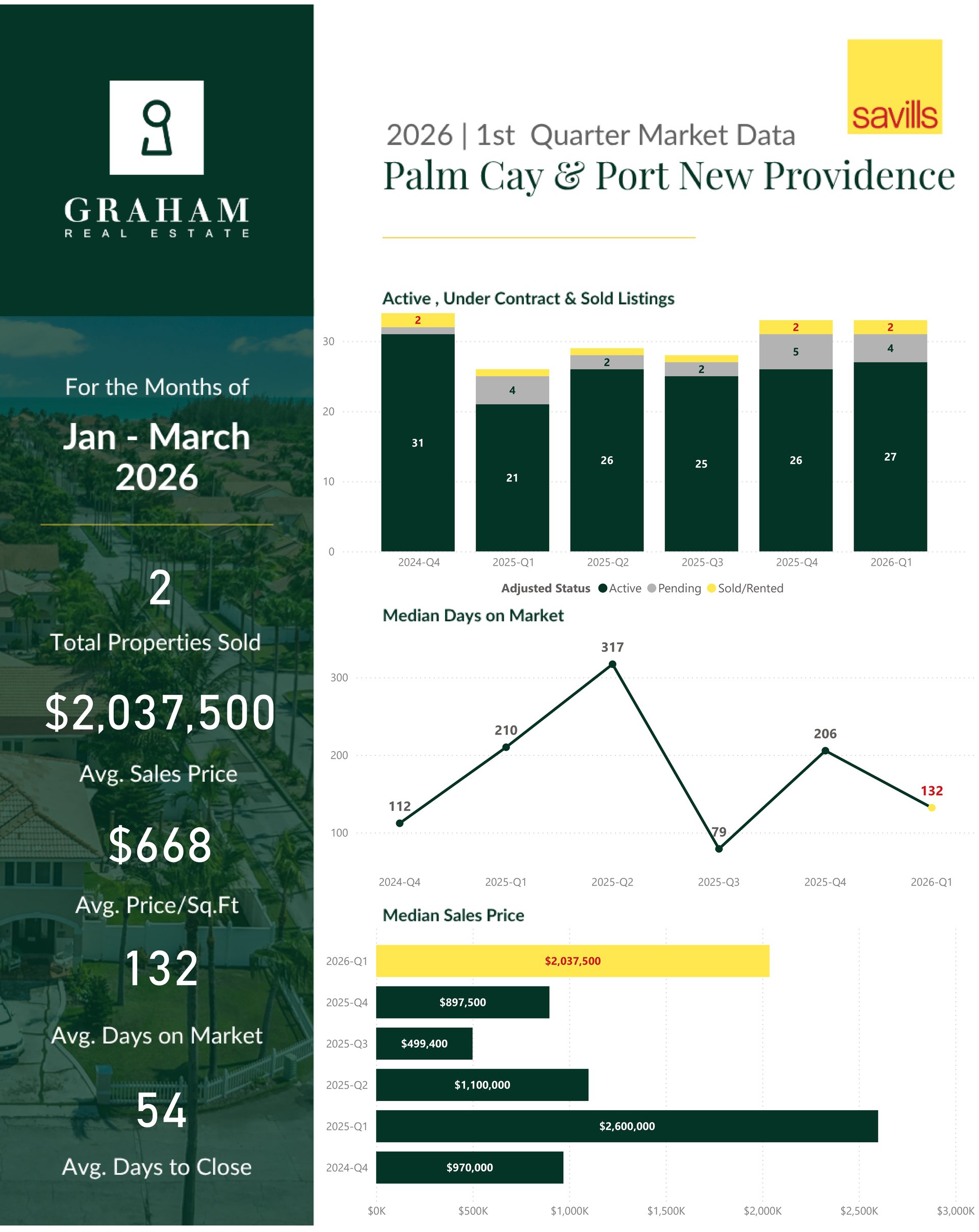

Port New Providence & Palm Cay

Port New Providence and Palm Cay finished Q1 with 27 active listings, 4 pending listings, and 2 closed sales. Both the average and median sales price came in at $2,037,500, while average days on market were 132 days and days to close 54 days. Buyer activity remains selective, with efficient transaction timelines when the right property becomes available.

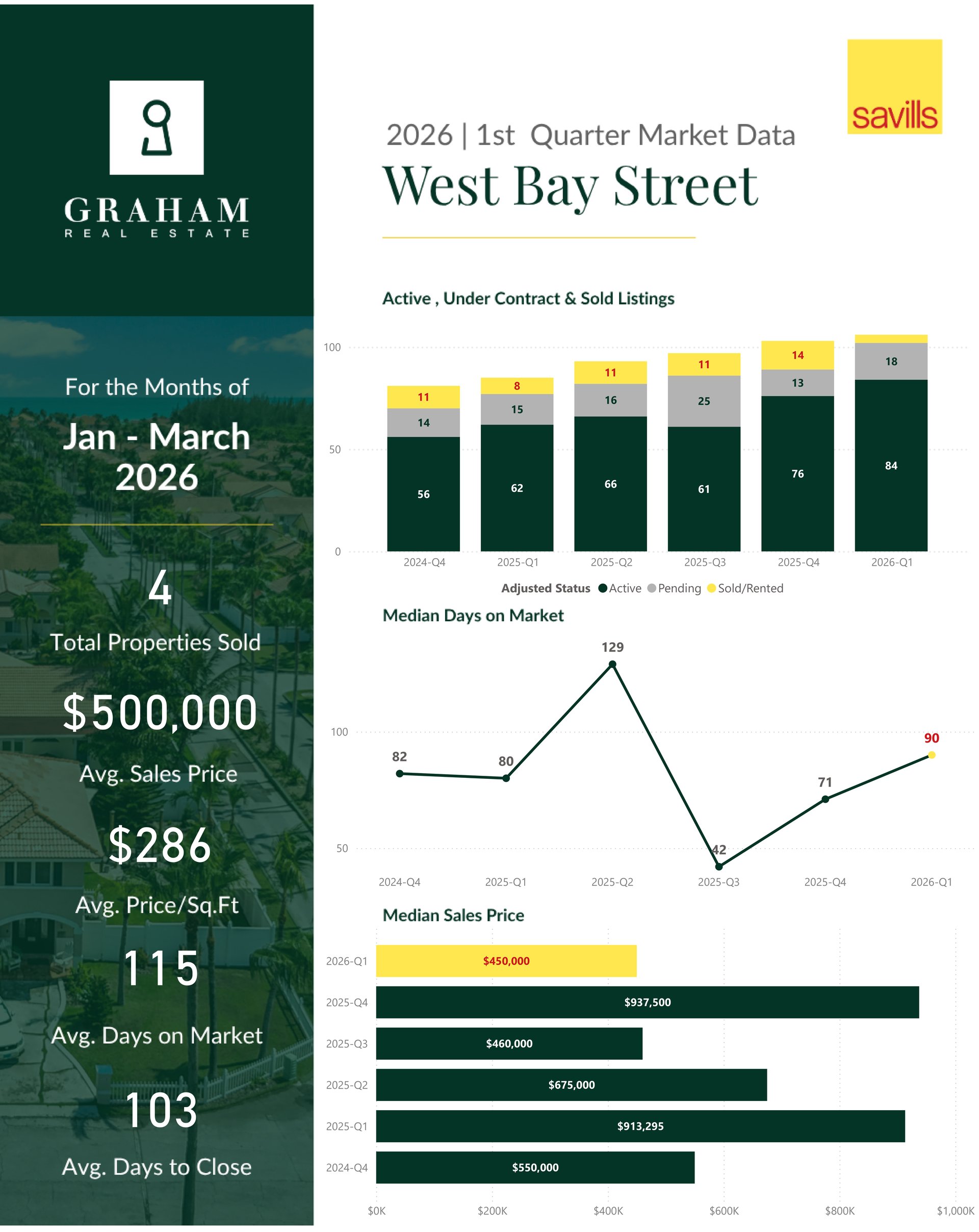

West Bay Street

West Bay Street recorded 84 active listings, 18 pending listings, and 4 closed sales in Q1, down from 14 in Q4. The average sales price was $500,000, with a median of $450,000. Average days on market were 115 days, and days to close came in at 103 days, reflecting continued steady demand in this mid-market corridor.

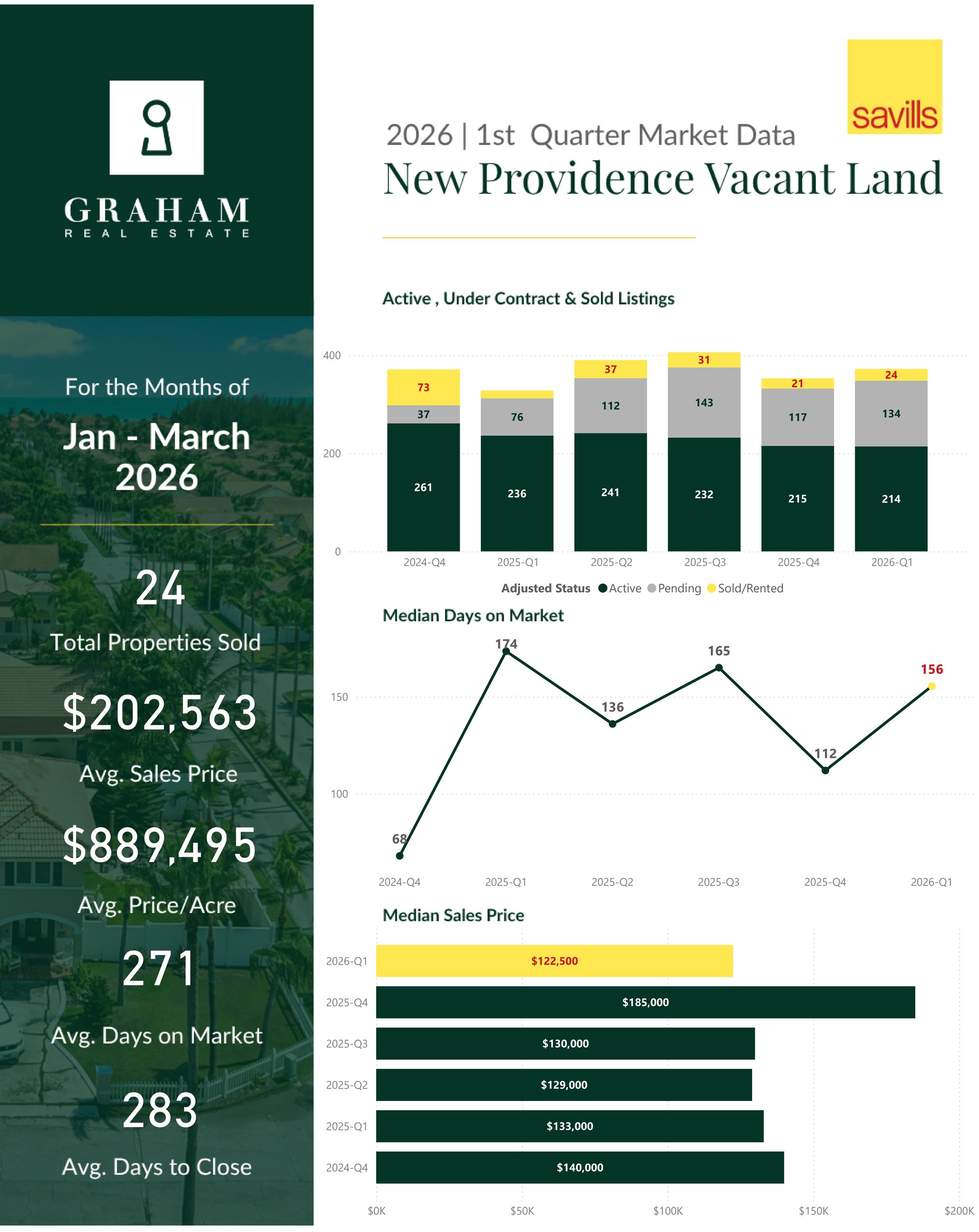

New Providence Vacant Land

New Providence land recorded 214 active listings, 134 pending listings, and 24 closed sales in Q1. The average sales price was $202,563, with a median of $122,500. Average days to close extended to 283 days, reflecting the complexity of land transactions, while demand remains strongest for well-located residential lots.

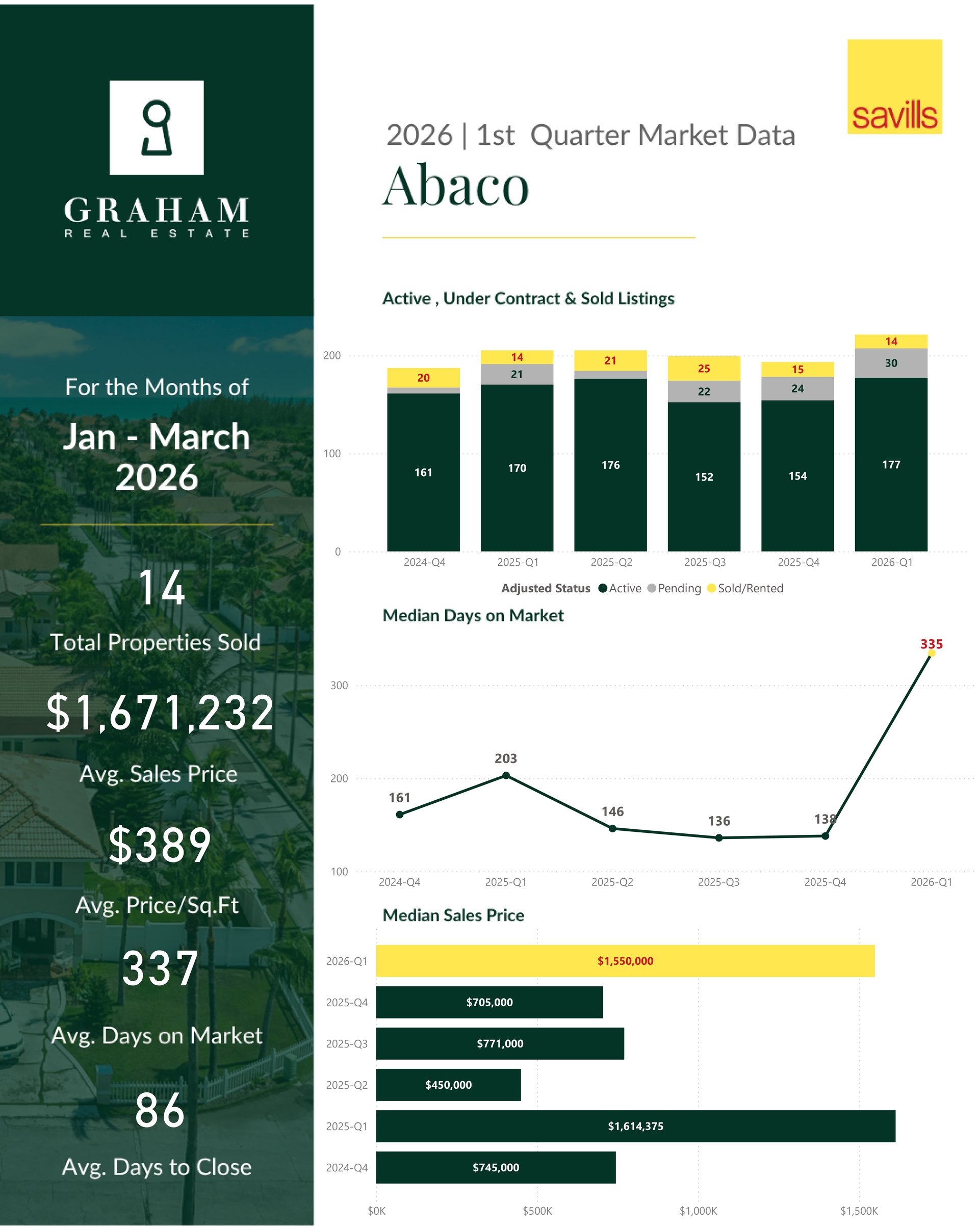

Abaco

Abaco recorded 177 active listings in Q1, up from 154 in Q4, while pending sales increased to 30 and closed sales declined slightly to 14 from 15. The average sales price rose to $1,671,232, with a median of $1,550,000. Average days on market extended to 337 days, while days to close improved to 86 days, suggesting that well-priced properties continue to move efficiently once buyers commit.

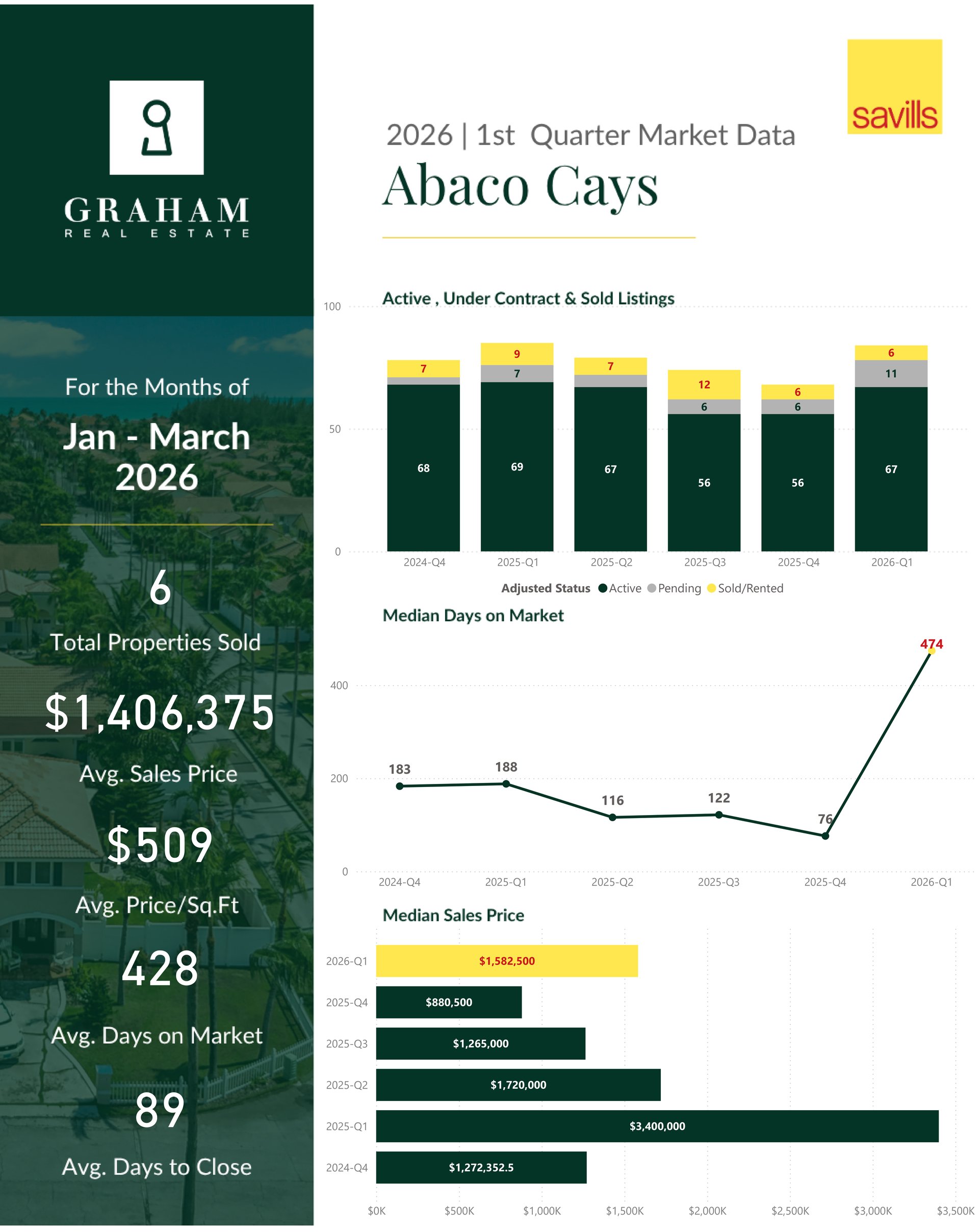

Abaco Cays

The Abaco Cays recorded 67 active listings, 11 pending listings, and 6 closed sales in Q1. The average sales price was $1,406,375, with a median of $1,582,500. Average days on market extended to 428 days, underscoring the patient and selective nature of this submarket, while days to close came in at 89 days.

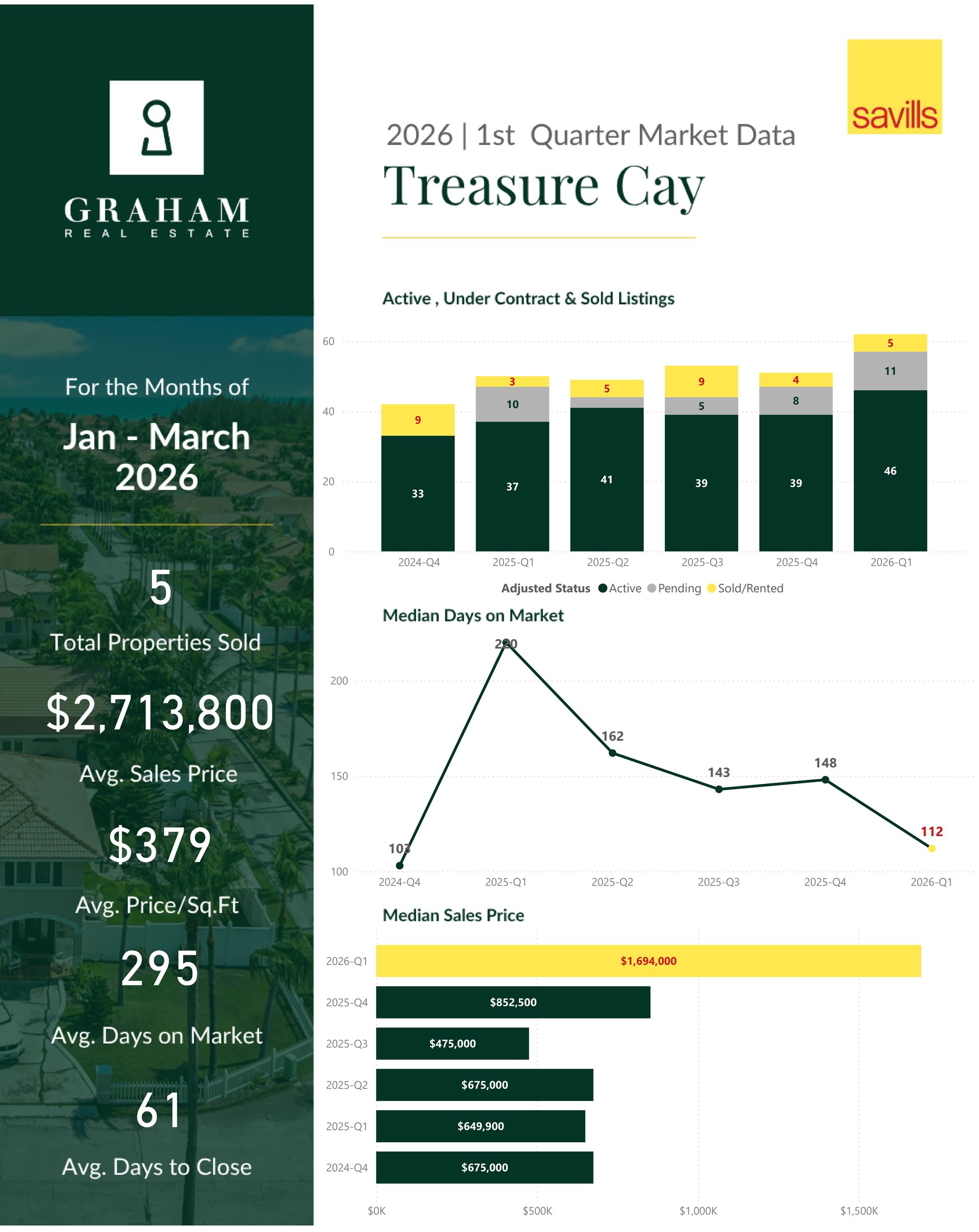

Treasure Cay

Treasure Cay recorded 46 active listings, 11 pending listings, and 5 closed sales in Q1. The average sales price rose to $2,713,800, with a median of $1,694,000. Average days on market were 295 days, while days to close shortened to 61 days, indicating efficient transaction timelines when buyers are ready to move.

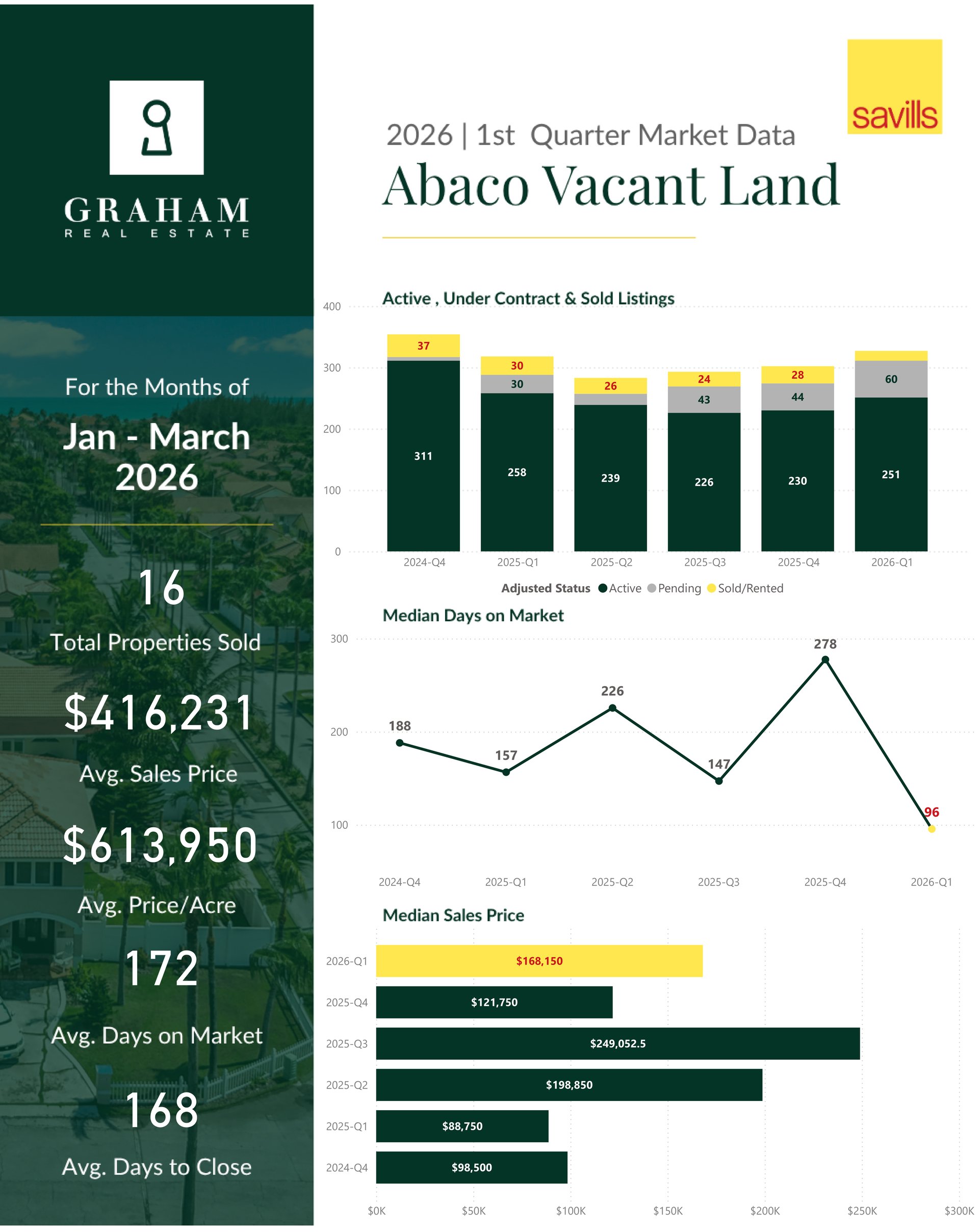

Abaco Vacant Land

Abaco land recorded 251 active listings, 60 pending listings, and 16 closed sales in Q1. The average sales price was $416,231, with a median of $168,150 and an average price per acre of $613,950. Average days on market were 172 days, with buyers remaining active across a range of parcel sizes and locations.

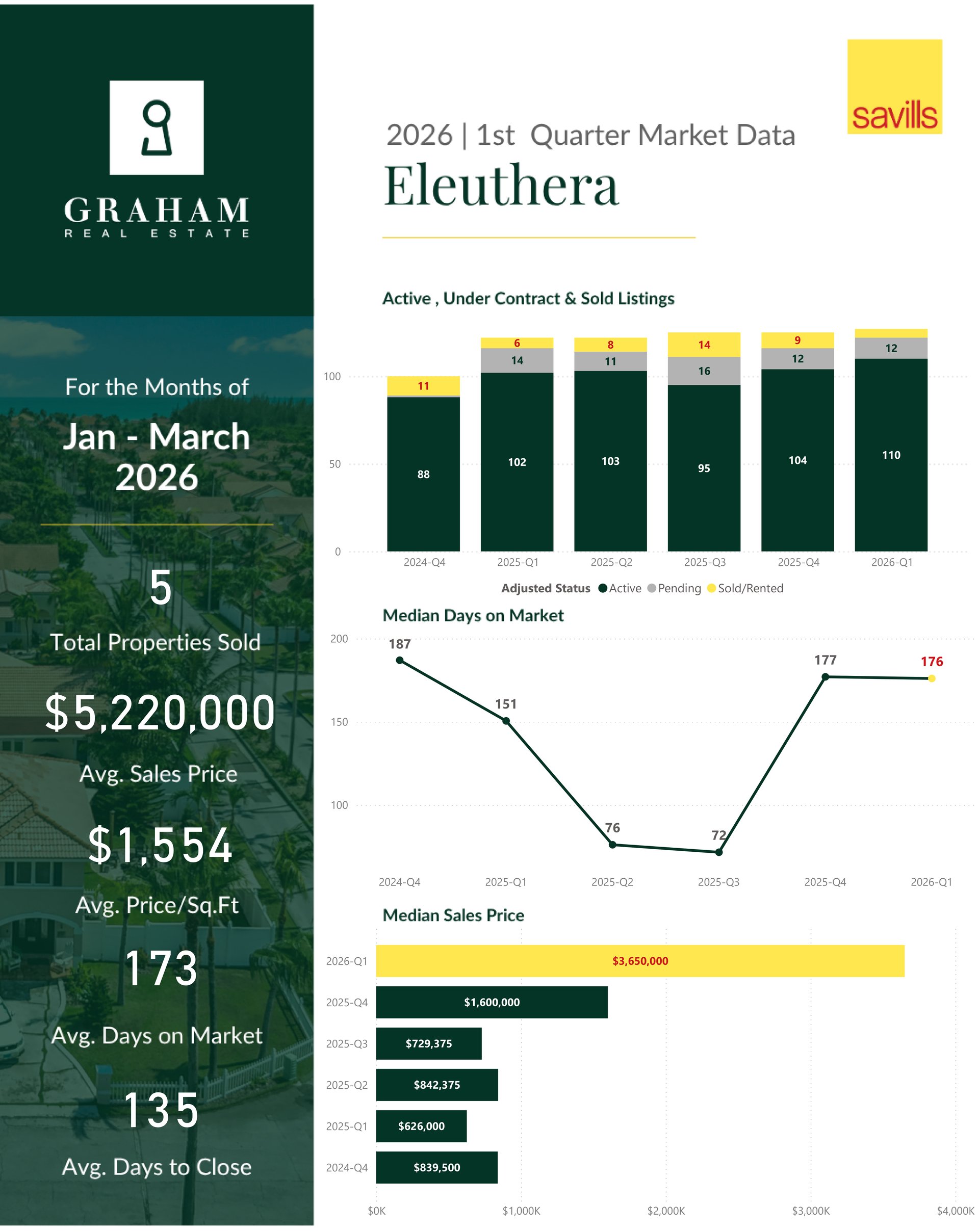

Eleuthera

Eleuthera recorded 110 active listings in Q1, with 12 pending listings and 5 closed sales. Pricing rose sharply, with the average sales price reaching $5,220,000 and the median sales price at $3,650,000. Average days on market were 173 days, reflecting a market driven by higher-end transactions where buyers are taking a measured approach.

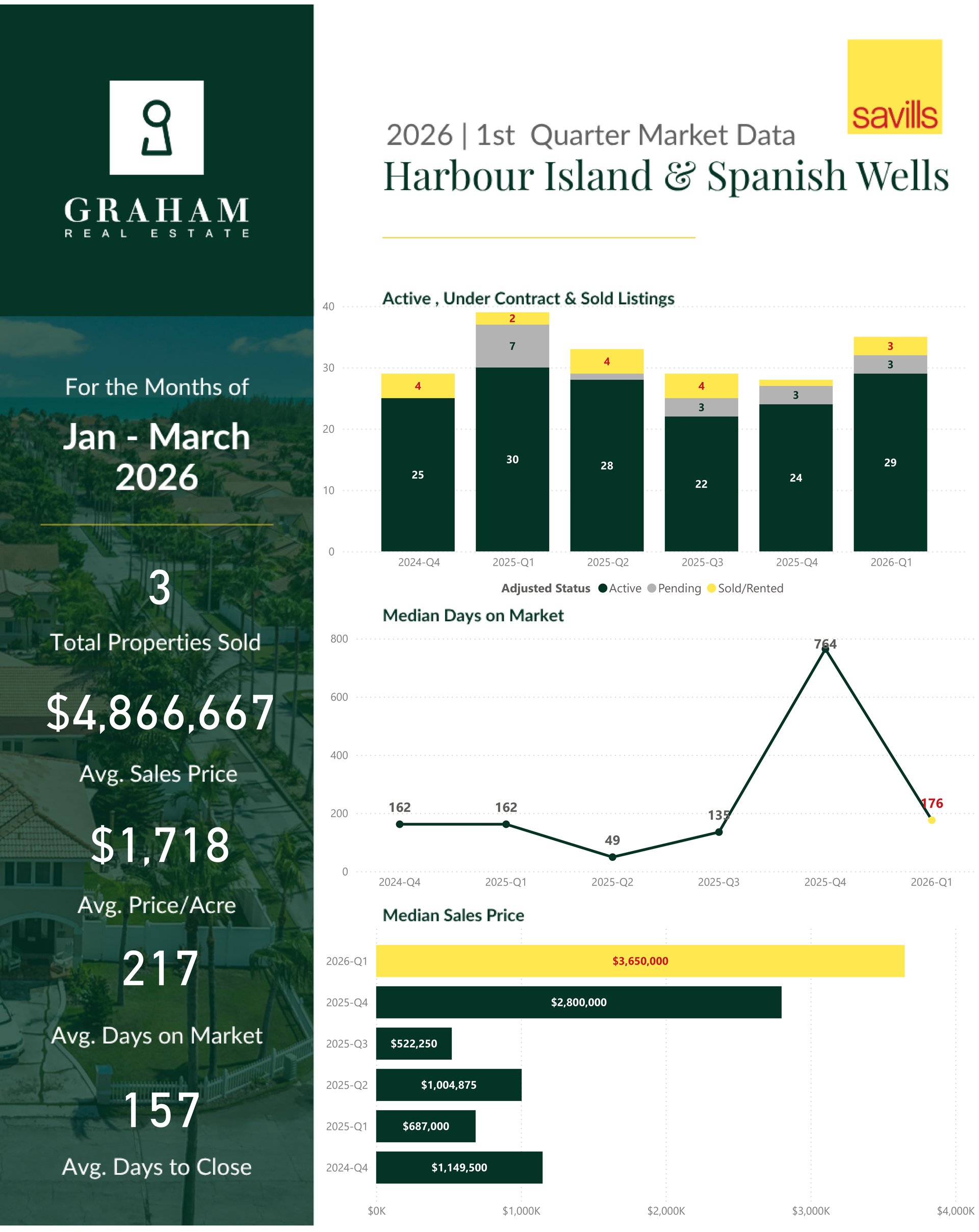

Harbour Island & Spanish Wells

Harbour Island and Spanish Wells recorded 29 active listings, 3 pending listings, and 3 closed sales in Q1, up from 1 sale in Q4. The average sales price was $4,866,667, with a median of $3,650,000. Average days on market were 217 days and days to close 157 days, reflecting the specialized and high-value nature of this market.

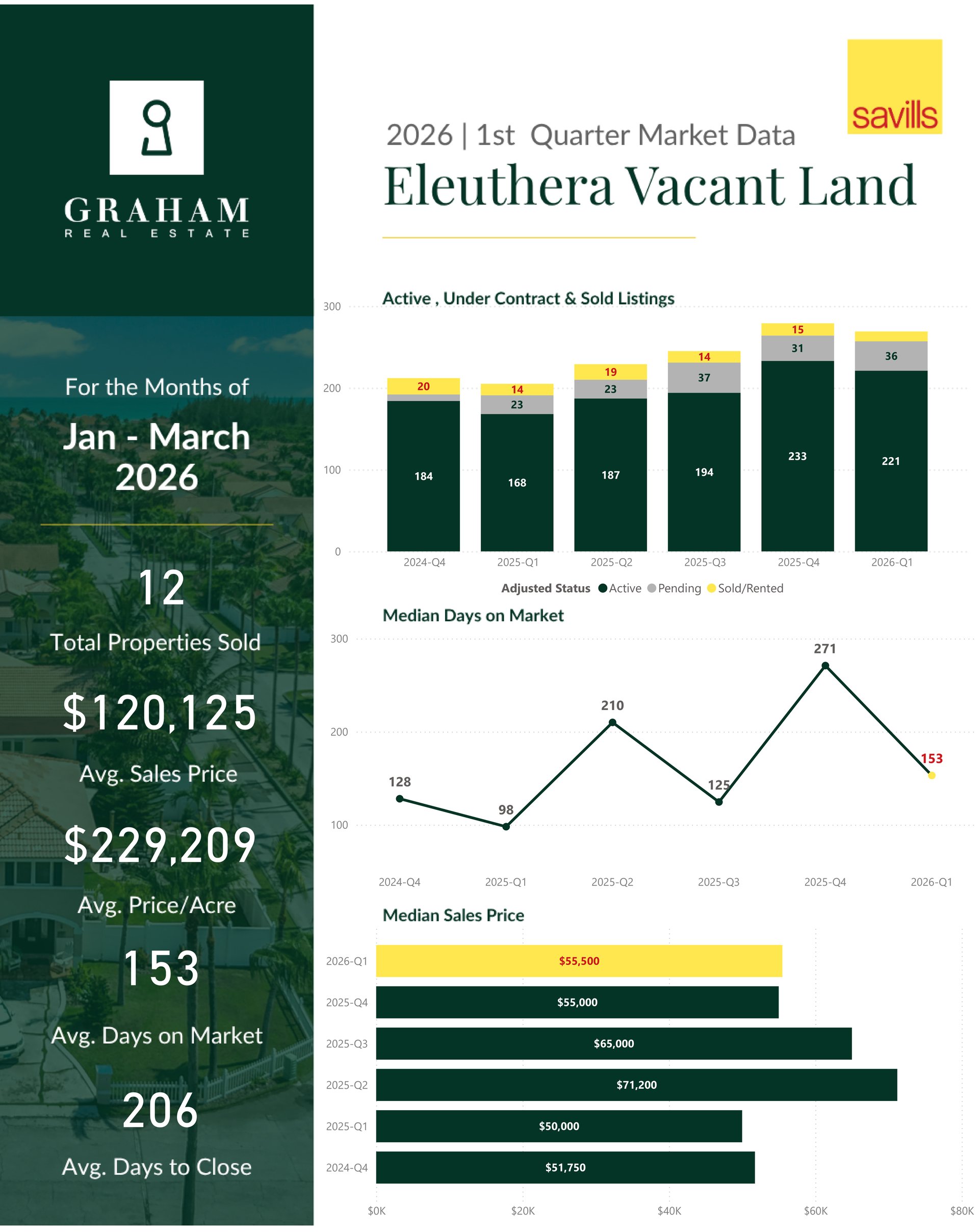

Eleuthera Vacant Land

Eleuthera land recorded 221 active listings, 36 pending listings, and 12 closed sales in Q1. The average sales price was $120,125, with a median of $55,500 and an average price per acre of $229,209. Average days to close extended to 206 days, consistent with the due diligence timelines typical of out-island land transactions.

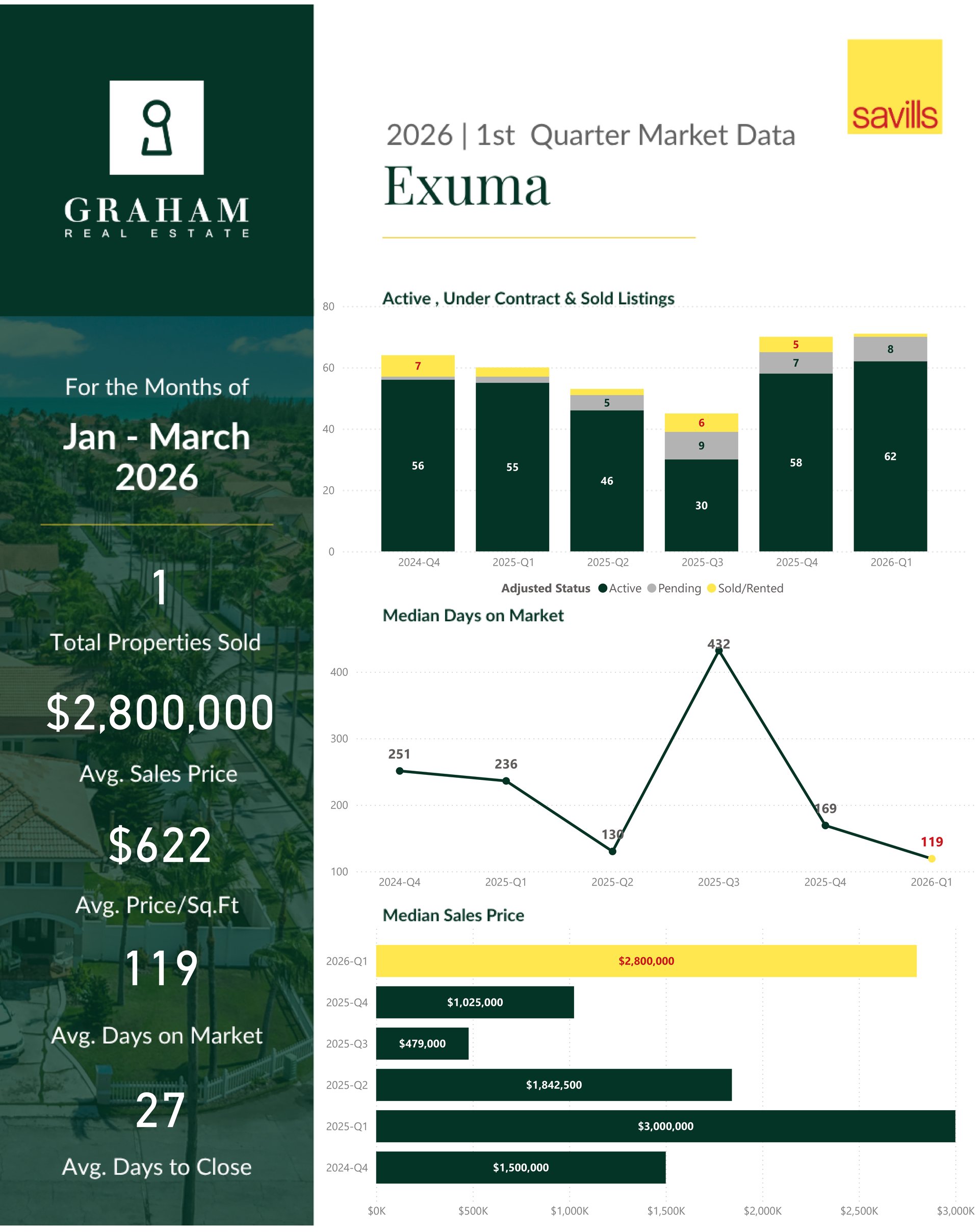

Exuma

Exuma recorded 62 active listings in Q1, with 8 pending listings and 1 closed sale, down from 5 in Q4. The average and median sales price both came in at $2,800,000. Average days on market were 119 days and days to close 27 days. While closed volume was limited, the pending pipeline points to more activity ahead.

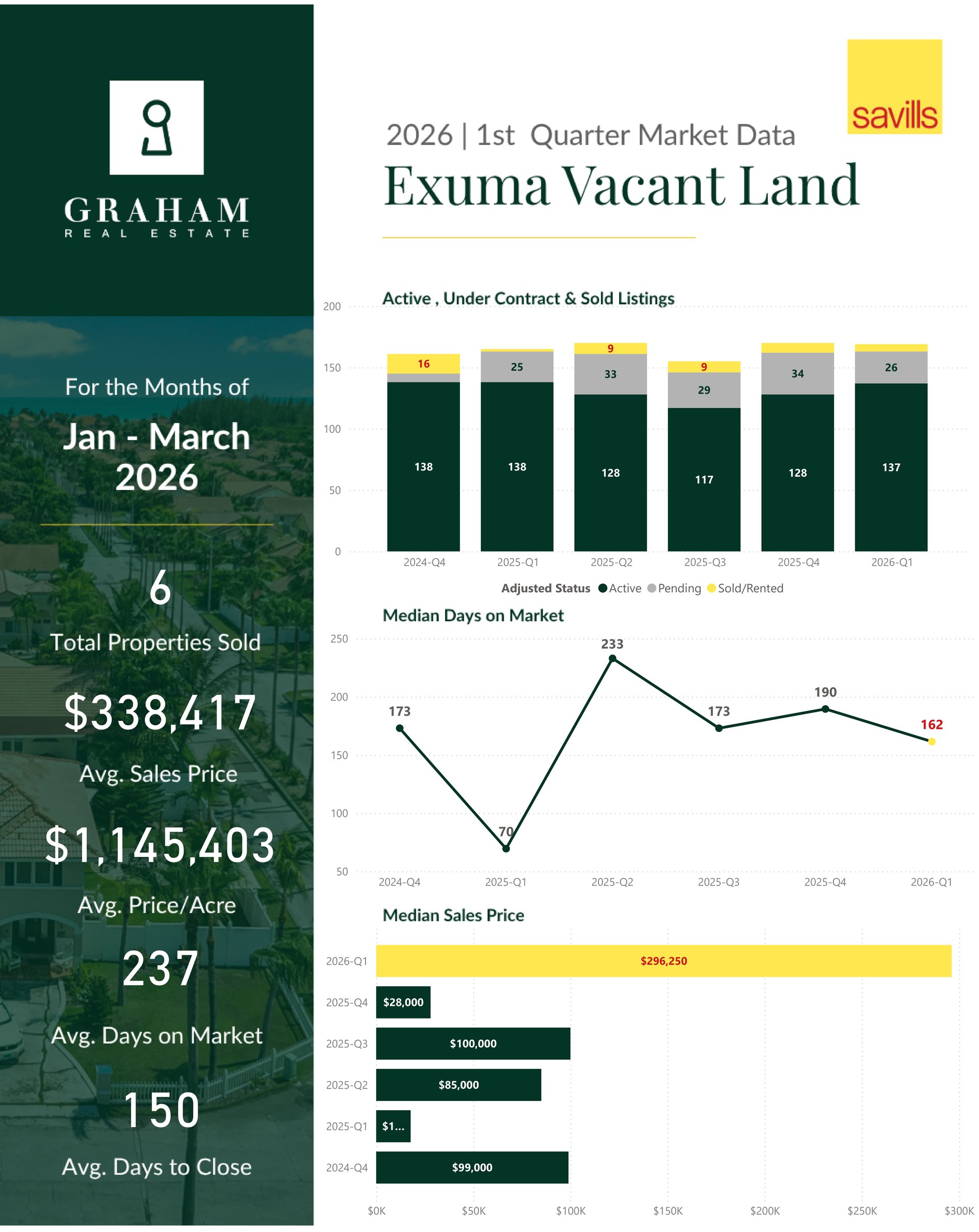

Exuma Vacant Land

Exuma land recorded 137 active listings, 26 pending listings, and 6 closed sales in Q1. The average sales price was $338,417, with a median of $296,250 and an average price per acre of $1,145,403. Average days on market were 237 days, with buyers remaining engaged but selective across the land market.

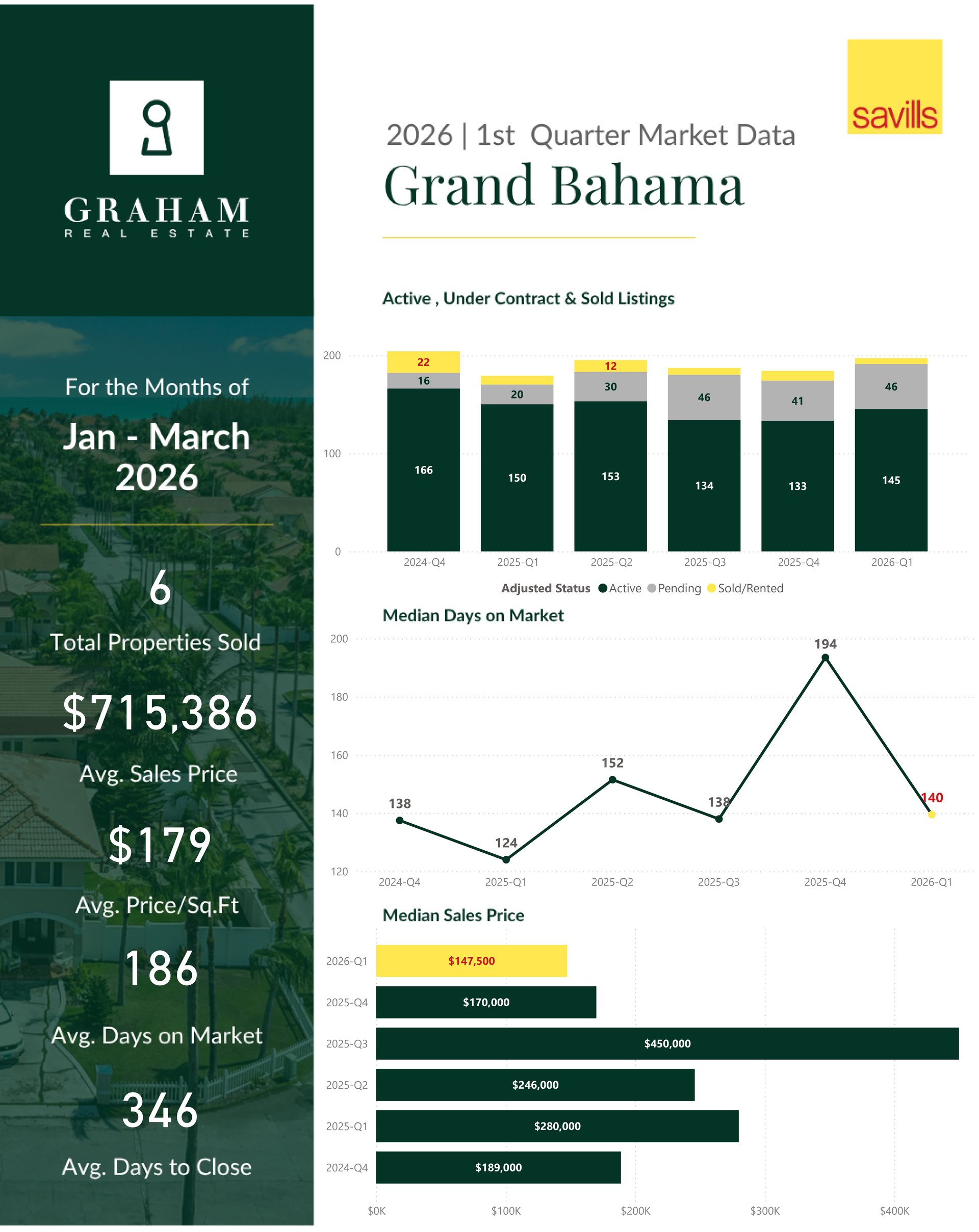

Grand Bahama

Grand Bahama recorded 145 active listings in Q1, with 46 pending listings and 6 closed sales, down from 10 in Q4. The average sales price was $715,386, with a median of $147,500. Average days on market were 186 days, while average days to close extended to 346 days, reflecting continued price sensitivity and longer transaction timelines in this market.

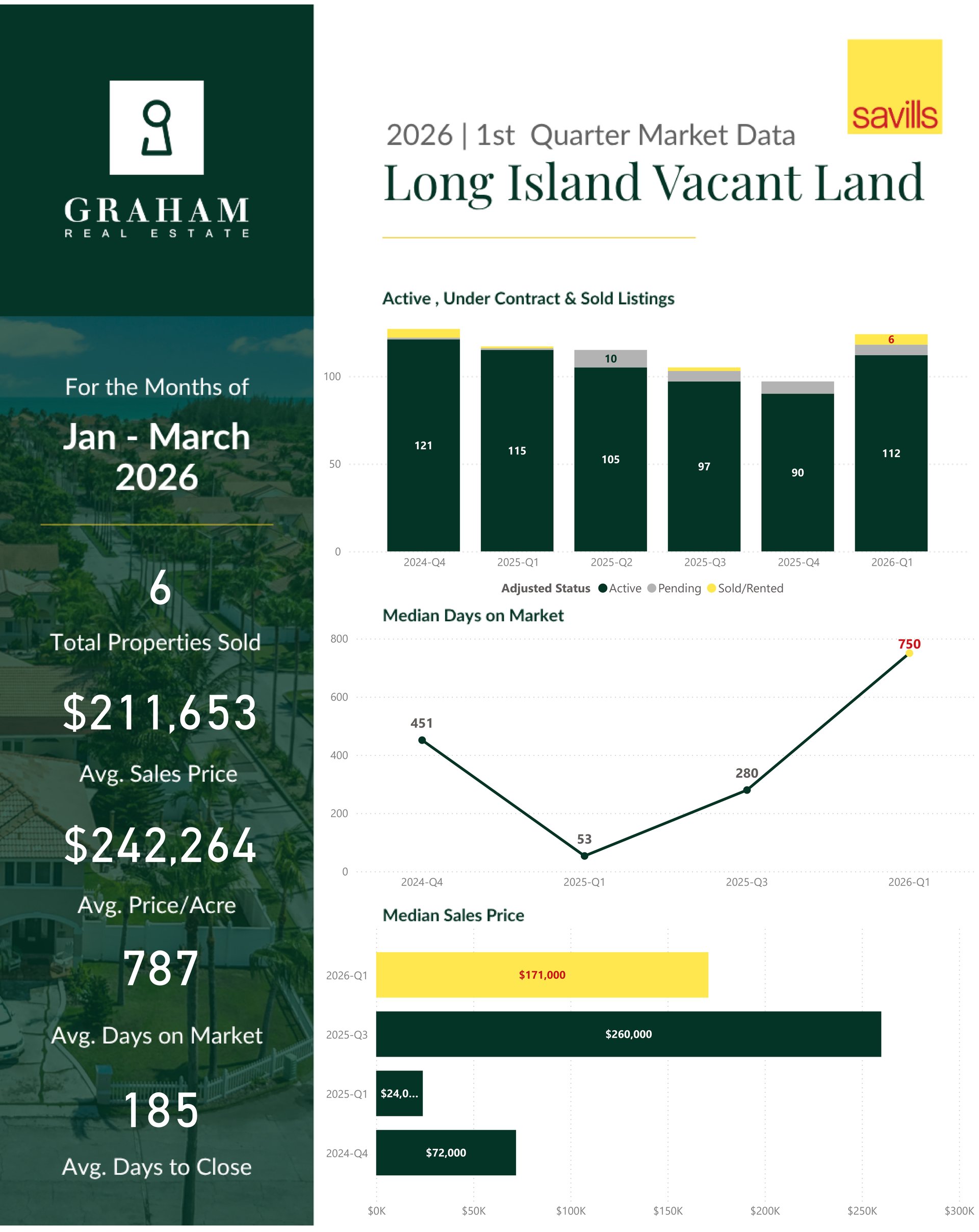

Long Island

Long Island recorded 112 active listings and 6 pending listings, with 6 vacant land sales closing in Q1. The average sales price was $211,653, with a median of $171,000 and an average price per acre of $242,264. Average days on market were 787 days, consistent with the patient nature of the Long Island land market. The most recent vacant land transactions prior to this quarter were in Q3 2025, when 2 properties sold at an average and median price of $260,000. No residential property sales were recorded in Q1.

Conclusion

Q1 2026 reflects a market with growing inventory, a strong pending pipeline, and moderating transaction volumes, a combination that gives buyers improved selection while reinforcing the value of accurate pricing for sellers. Premium markets continued to perform at the high end, while mid-range segments on New Providence demonstrated consistent demand. With pending sales up across the islands, Q2 is positioned to be a more active quarter for closings.