Market Overview Q3 2025

The Bahamian real estate market showed renewed strength in the third quarter of 2025, marked by rising sales activity, increased pending transactions, and significant price gains in several key markets. Across the islands, active listings declined, indicating that inventory is being absorbed at a healthy pace. At the same time, pending sales jumped considerably, reflecting strong forward demand heading into the final quarter of the year. Average and median prices rose in many regions, particularly in the upper mid-range and select luxury segments, suggesting both confidence and continued appetite for high-quality properties. Notably, time on market improved in many areas, signaling that well-positioned listings are moving more quickly.

Market Coverage Note

This report specifically focuses on the Islands of Abaco, Eleuthera, Exuma, Grand Bahama, Long Island, and New Providence. All data reflects activity related to single-family homes, condominiums, apartments, and half duplexes, unless otherwise stated. Other property types, such as vacant land or commercial real estate, are excluded from these figures unless explicitly noted. This focused scope allows for a more accurate and relevant analysis of the residential market across key Bahamian islands that Graham Real Estate has a presence in.

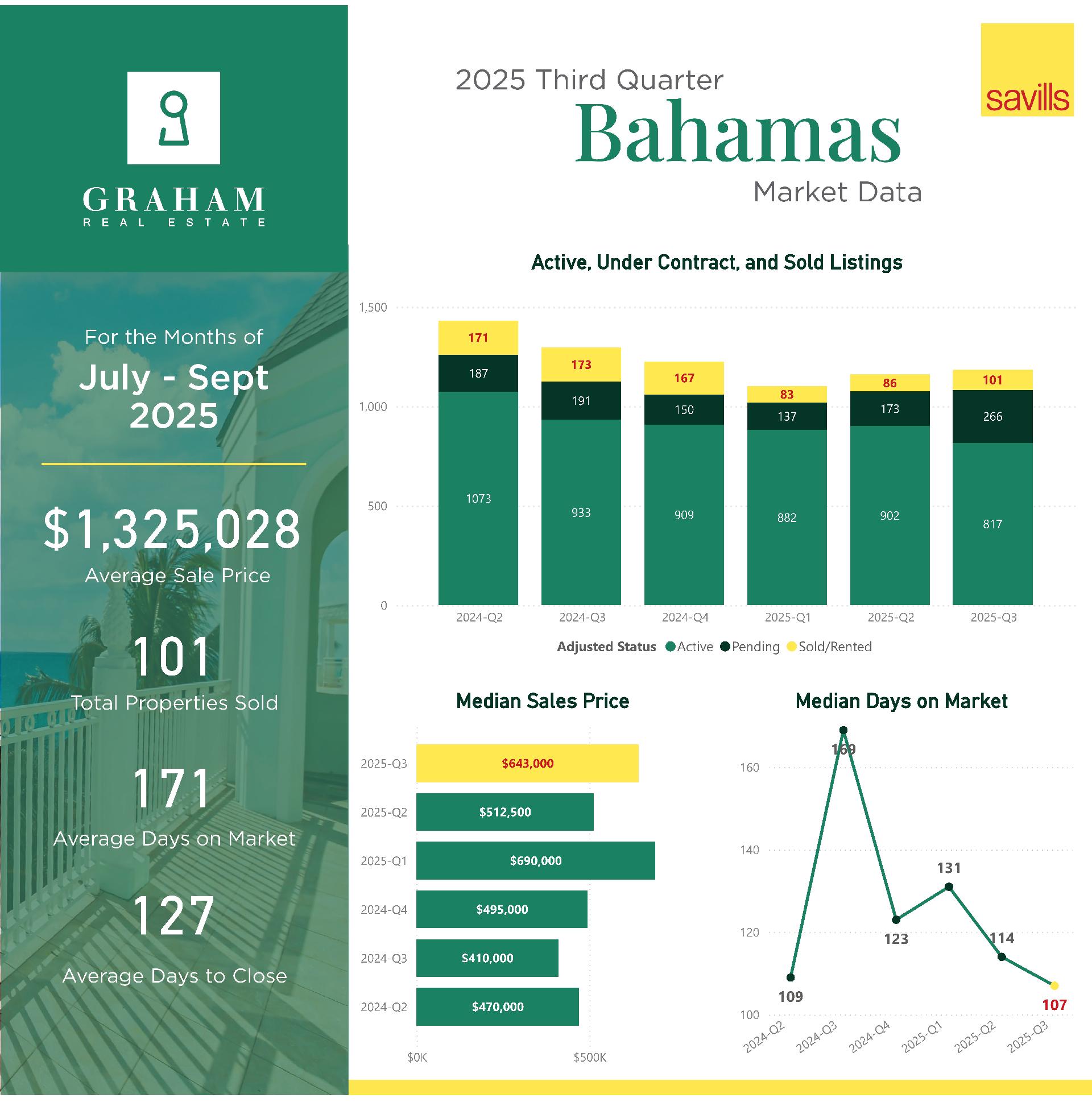

GRE Islands

The GRE Islands experienced a notable surge in market activity. Active listings declined to 817 from 902, but pending sales jumped sharply from 173 to 266, reflecting significant buyer momentum. Closed sales rose from 86 to 101. Both average and median prices increased strongly — the average rose to $1.33M from $781K, and the median climbed to $643K from $513K — indicating renewed strength in higher-value transactions. Average time on market shortened to 101 days from 159, with median days improving slightly to 107. The only slight slowdown was in days to close, which rose modestly to 127 from 112.

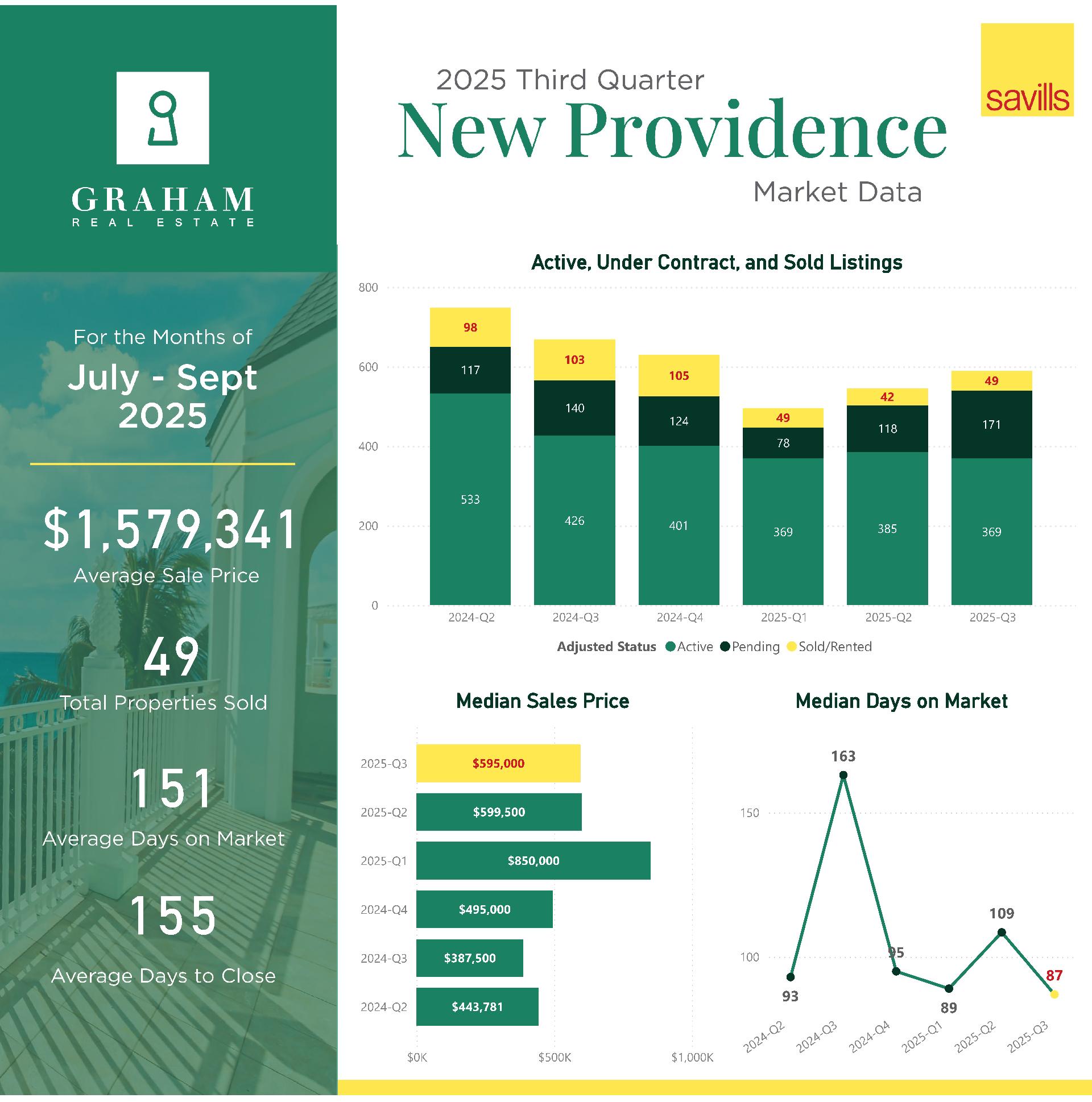

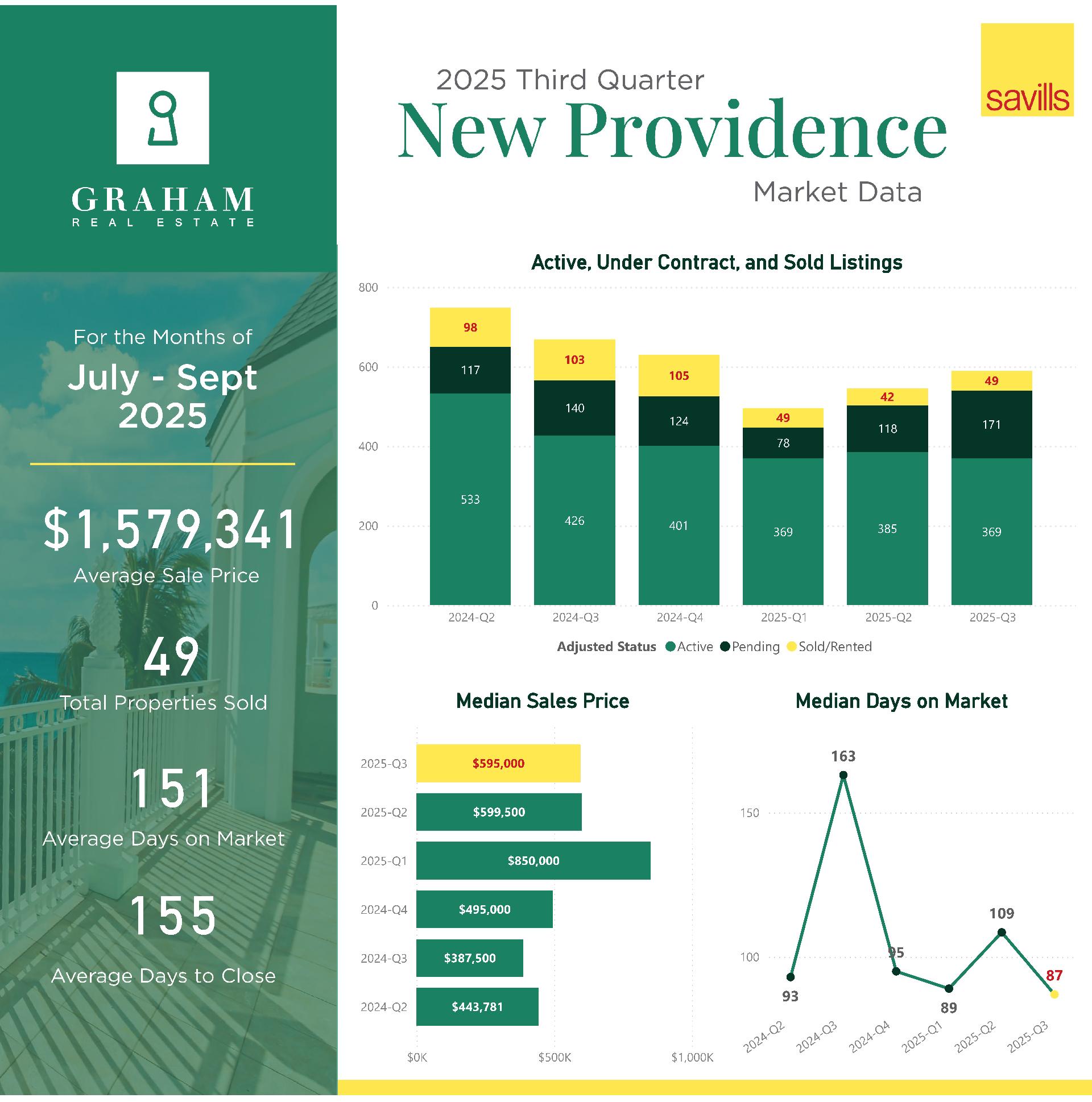

New Providence

New Providence saw a very strong quarter. Pending sales climbed from 118 to 171, and closed sales rose from 42 to 49. Average sale price surged to $1.58M from $795K, reflecting renewed high-value transactions. Median held steady at $595K. Average days on market improved slightly to 151 from 156, and median shortened to 87 from 109.

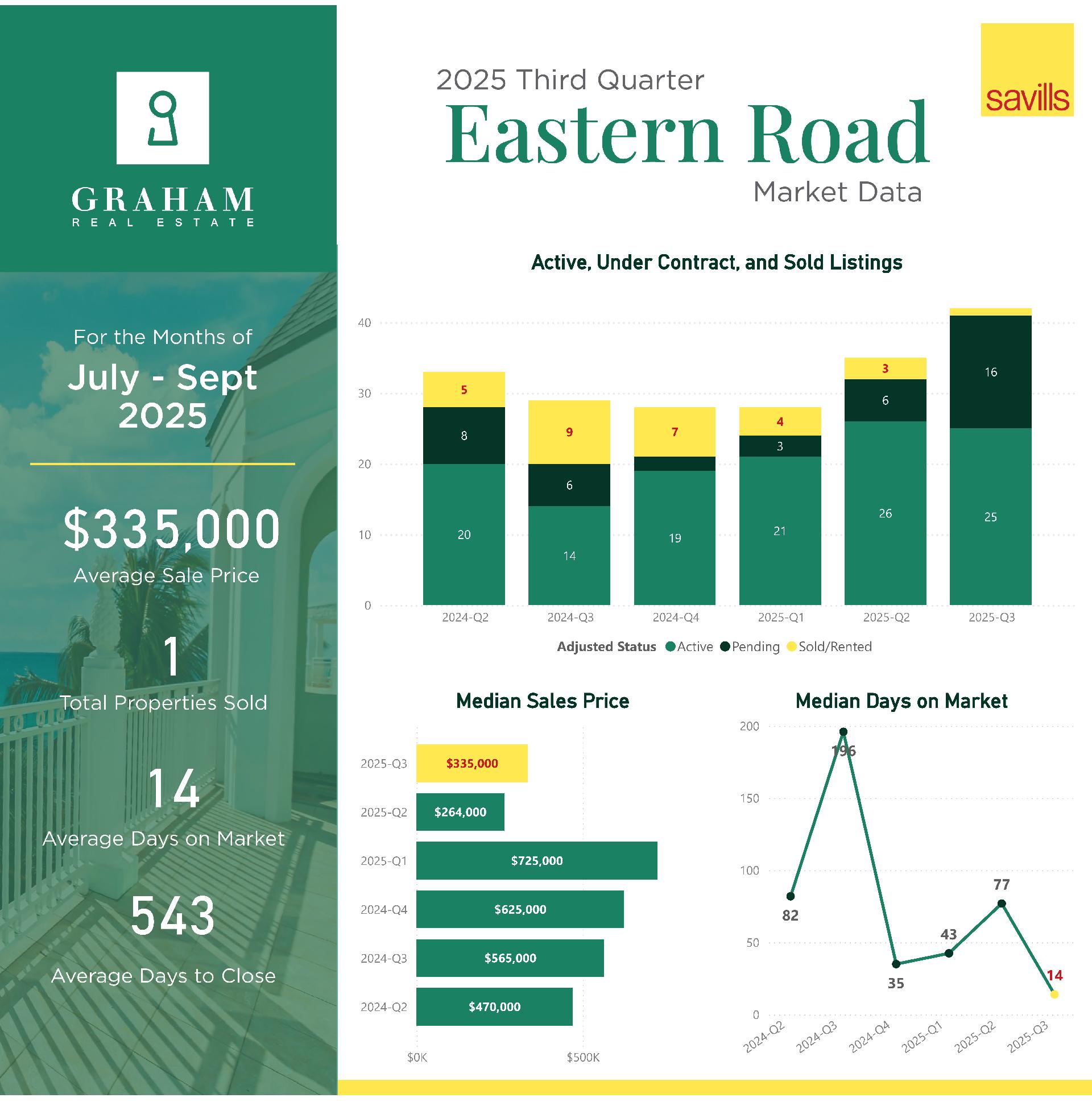

Eastern Road

Eastern Road saw mixed results. Active listings held steady at 25, but pending listings jumped from 6 to 16. Sales slowed to just 1 from 3 last quarter. The sole sale was at $335K, setting both average and median. Time on market shortened dramatically to 14 days, though time to close lengthened considerably to 543 days, reflecting an older listing finally closing.

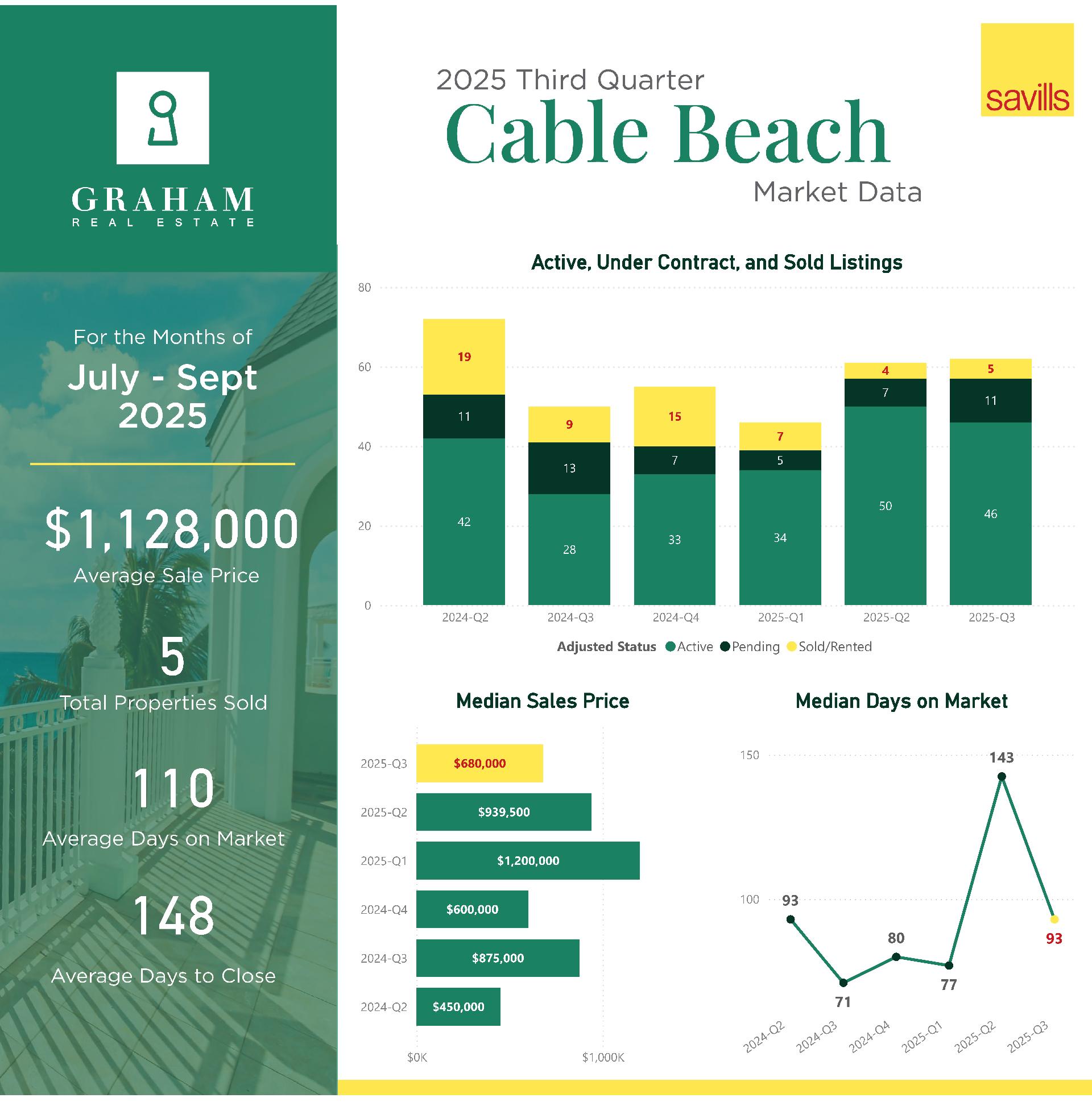

Cable Beach

Cable Beach experienced steady improvement. Pending listings rose from 7 to 11, and closed sales ticked up from 4 to 5. Average price increased to $1.13M from $982K, though median dipped to $680K from $940K. Days on market improved — average dropped to 110 from 148, and median fell to 93 from 143.

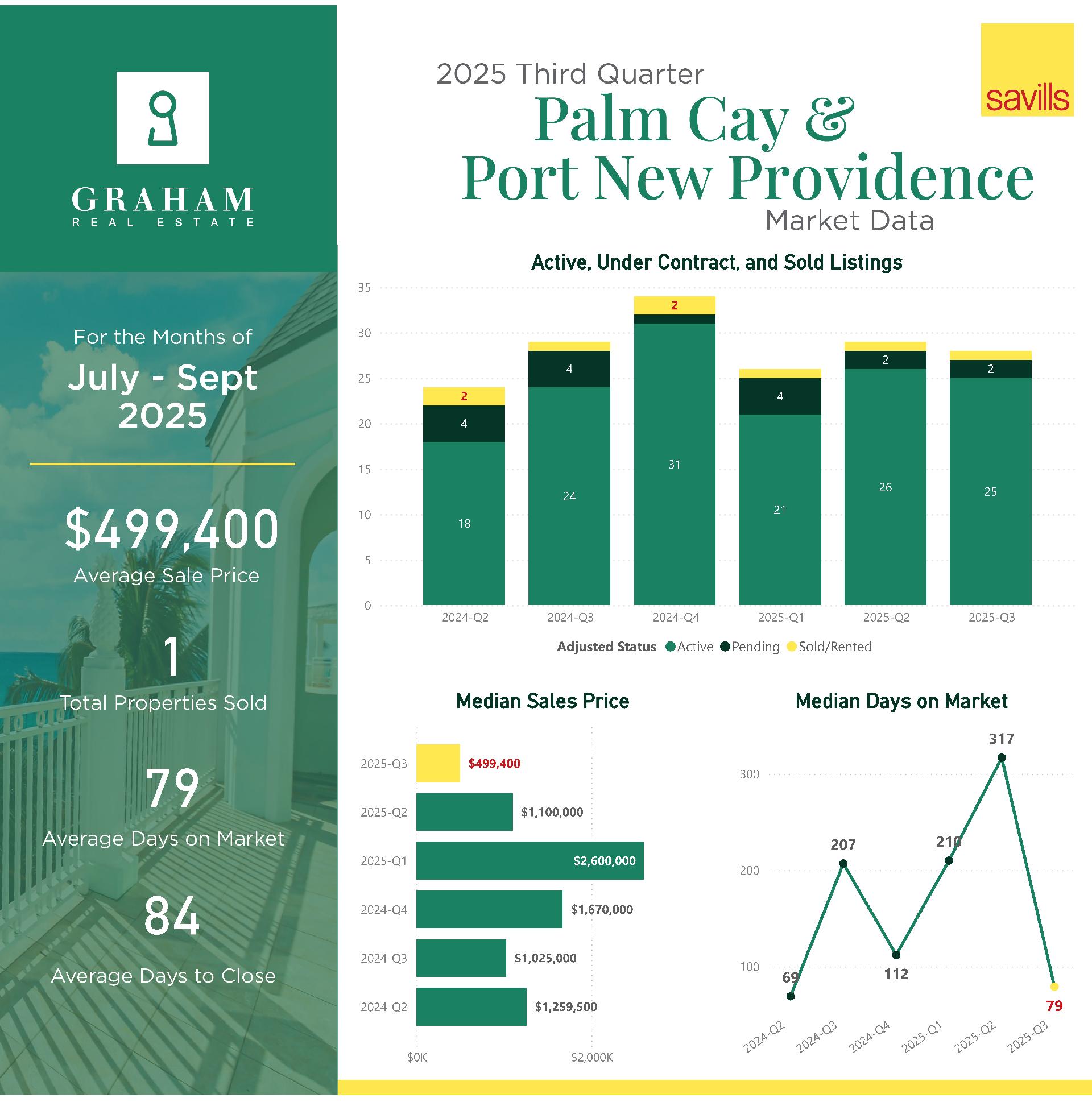

Port New Providence & Palm Cay

This segment remained quiet, with 1 sale matching last quarter’s. The sale price was $499K, down from $1.1M. Days on market improved to 79 from 317, though pending listings remained flat at 2.

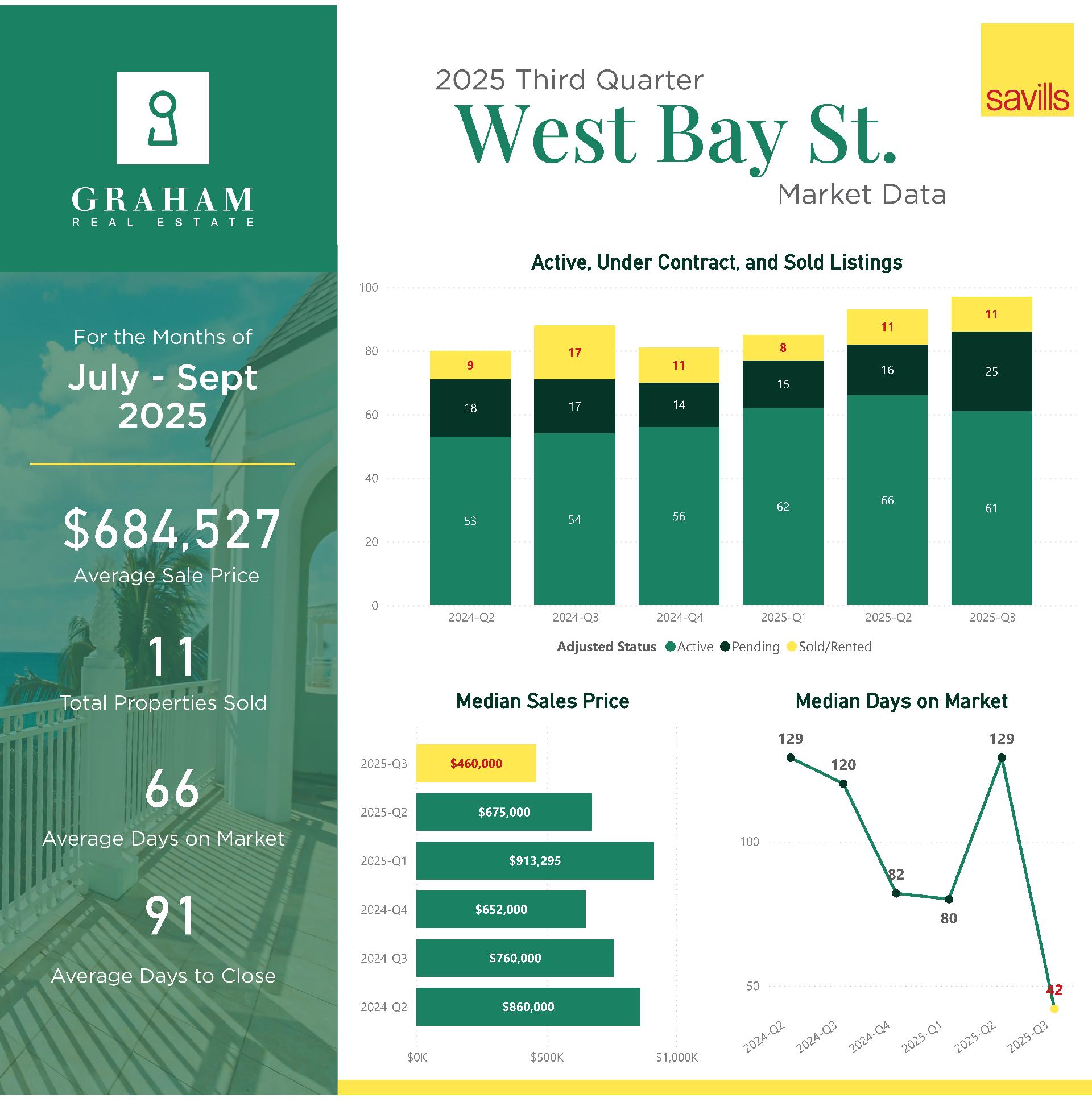

West Bay Street

West Bay Street continued to perform well, with 11 sales matching Q2 and pending listings rising from 16 to 25. Average price declined to $685K from $869K and median fell to $460K from $675K, indicating a shift toward mid-range homes. Marketing timelines improved significantly — average days on market dropped to 66 from 149, and median to 42 from 129.

New Providence Land

New Providence Land saw pending listings rise from 112 to 143, while closed sales dipped from 37 to 31. Average price fell to $172K from $253K, though median inched up to $130K from $129K. Time on market shortened modestly to 180 days from 207, while median days lengthened to 165 from 136.

Abaco

Abaco continued to build on Q2’s momentum. Active listings declined to 152 from 176, while pending listings nearly tripled from 8 to 22. Closed sales rose from 21 to 25. Average sale price increased substantially to $1.17M from $801K, and median jumped to $771K from $450K. While average days on market ticked up slightly to 203, the market overall shows deepening buyer interest, especially in mid-to-upper segments.

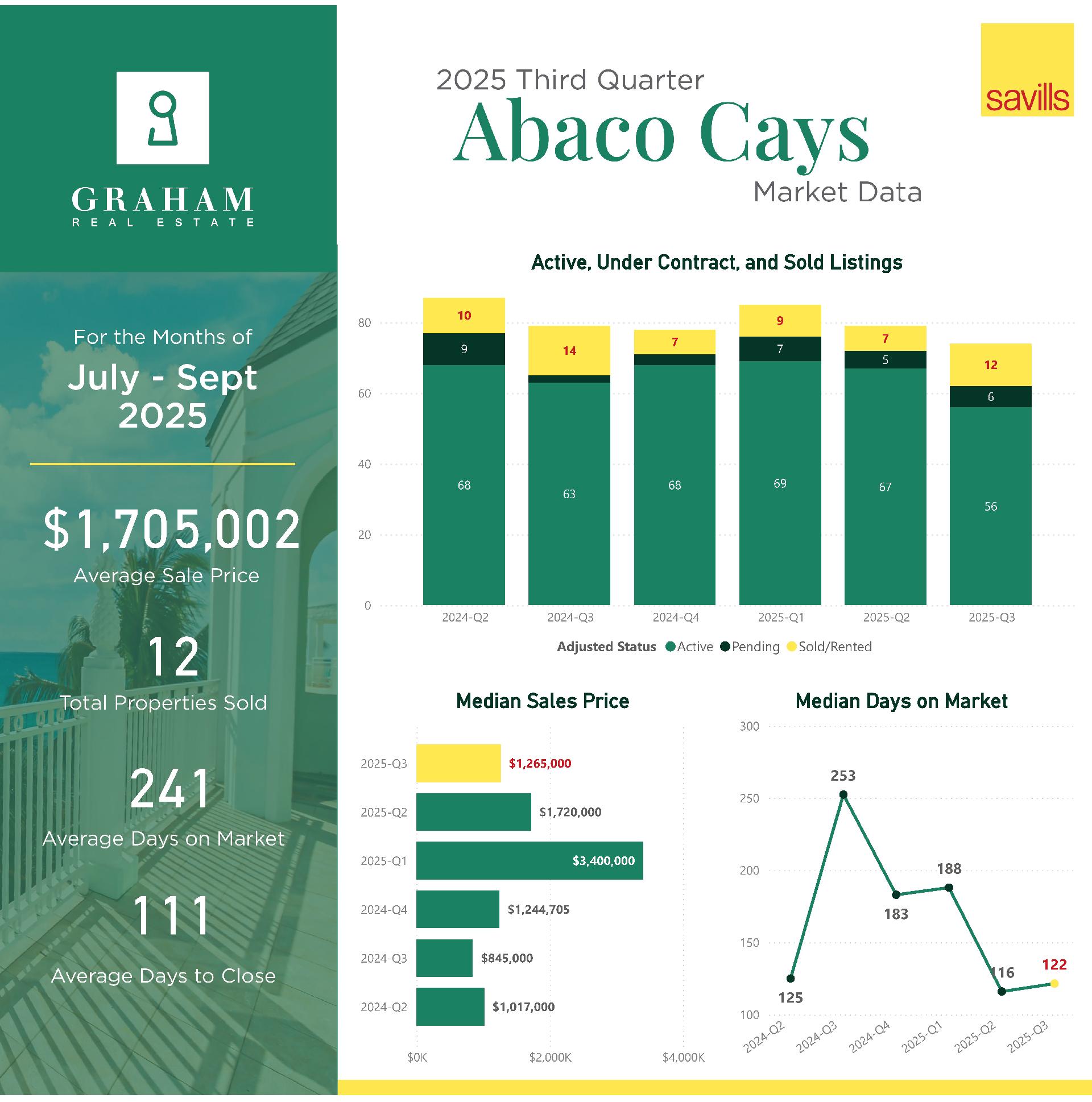

Abaco Cays

The Abaco Cays saw improved transaction volume, with 12 sales compared to 8 in Q2. Pending listings rose modestly to 6. Average price increased to $1.71M from $1.42M, though median dipped to $1.27M from $1.72M, suggesting a mix shift toward more mid-range island properties alongside continued luxury activity. Marketing timelines lengthened slightly, with average days on market climbing to 241 from 164, and days to close increased to 111 from 46, likely reflecting more complex deals.

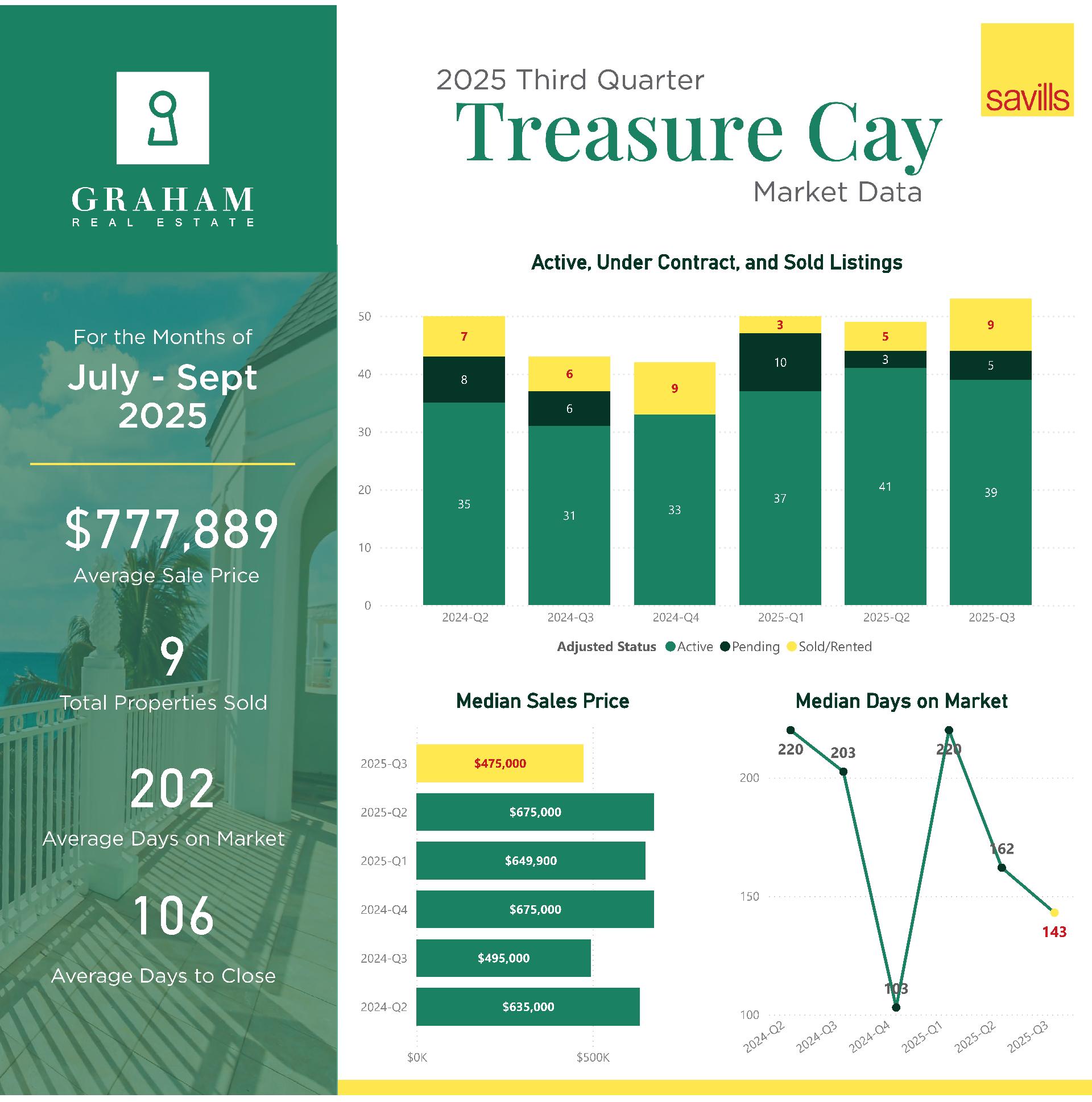

Treasure Cay

Treasure Cay posted stronger sales, with 9 transactions versus 5 in Q2. Pending listings rose from 3 to 5, and average price increased to $778K from $698K. Median price softened to $475K from $675K, reflecting a shift toward more moderately priced inventory. Average days on market fell to 202 from 247, and median days dropped to 143 from 162.

Abaco Land

Abaco Land posted solid results, with 24 sales compared to 26 last quarter and pending listings more than doubling from 18 to 43. Average price jumped to $852K from $331K and median rose to $249K from $199K. Days on market shortened to 237 from 333, and median dropped to 147 from 226, signaling increased buyer confidence.

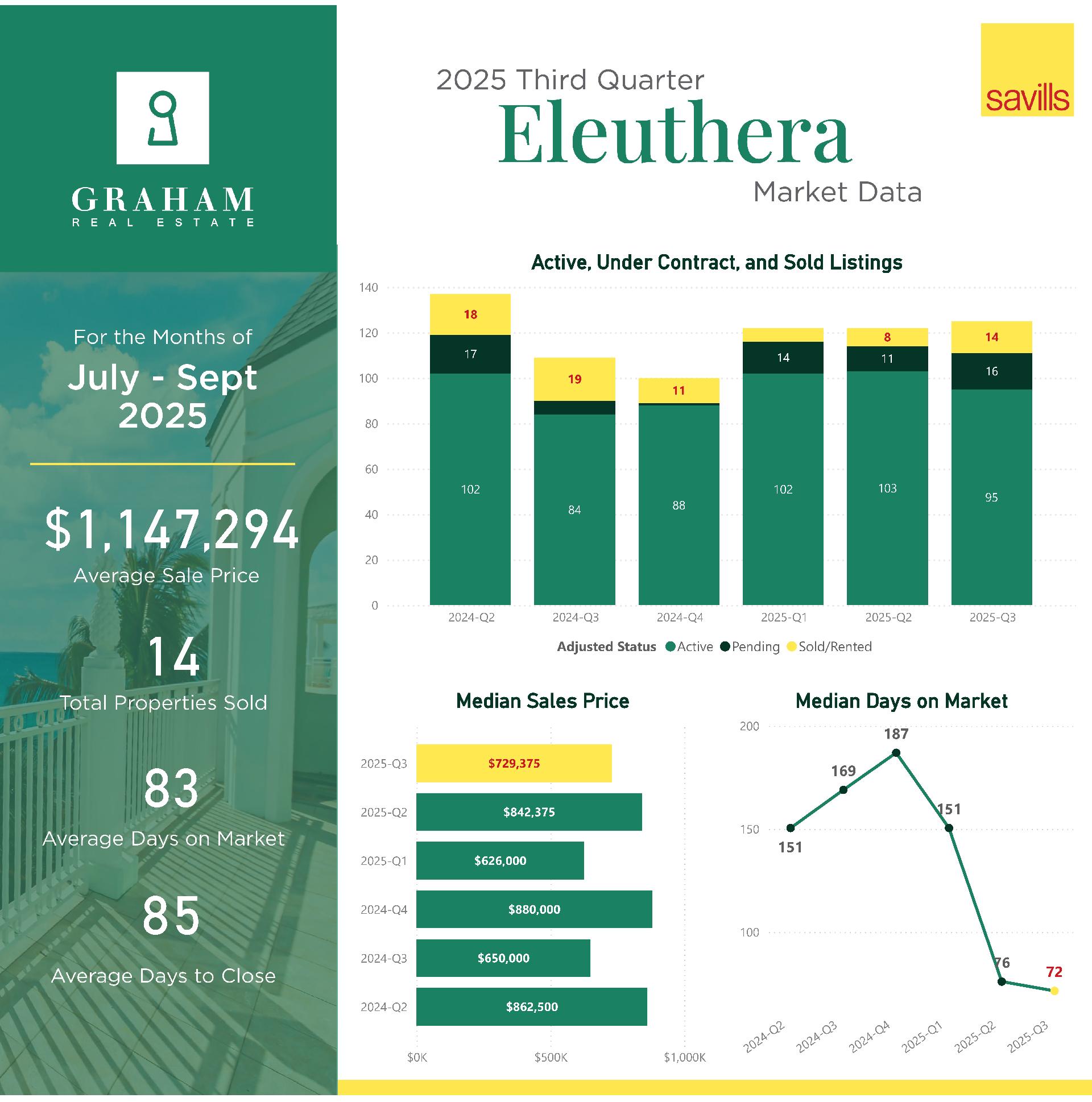

Eleuthera

Eleuthera had another strong quarter. Pending listings rose from 11 to 16, and closed sales increased from 8 to 14. Average price climbed to $1.15M from $868K, though median price eased slightly to $729K from $842K. Time on market improved, with average days dropping to 83 from 95 and median down to 72 from 76. Days to close remained stable at 85.

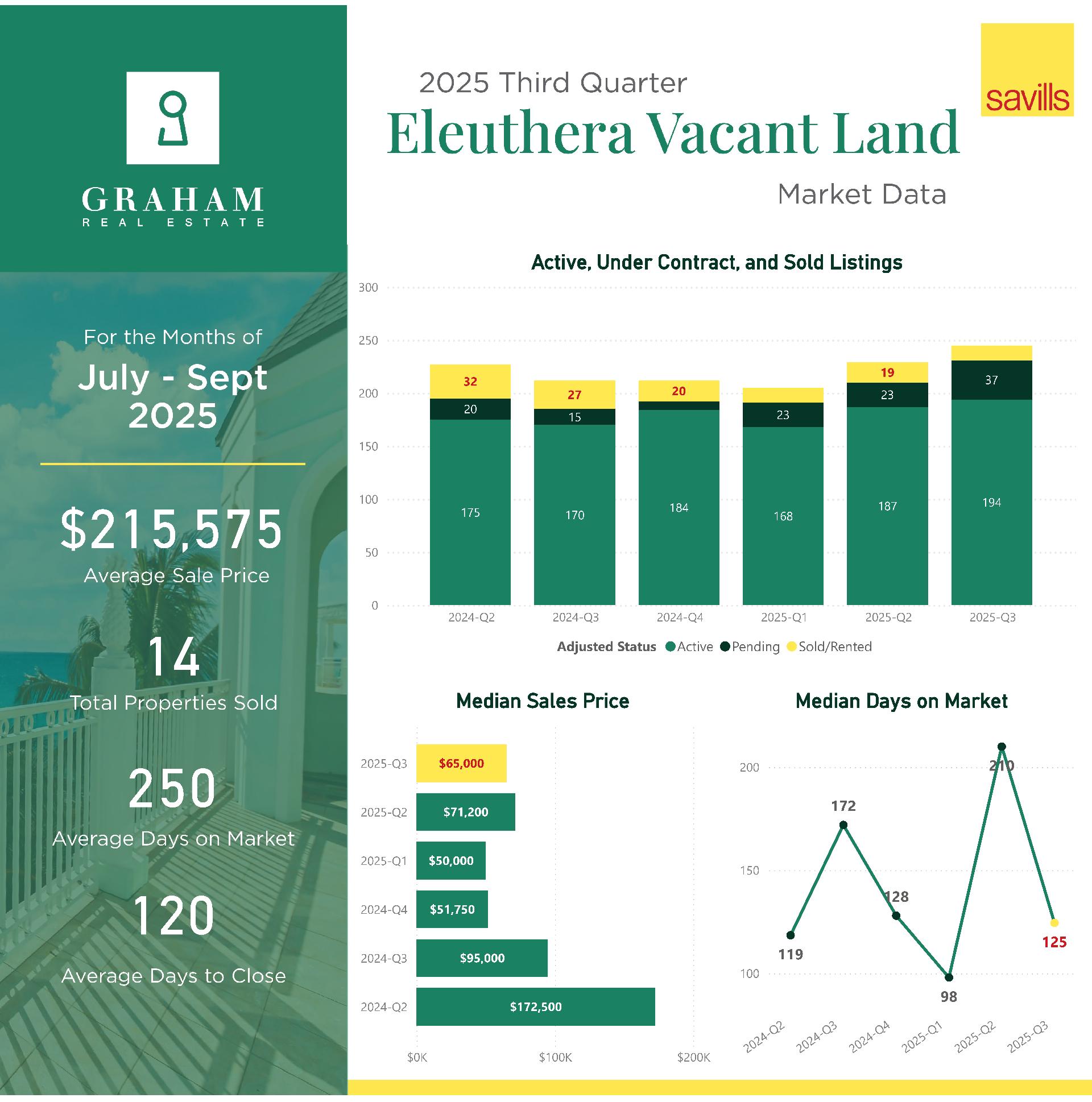

Eleuthera Land

Eleuthera Land saw a slight dip in sales from 19 to 14, though pending listings climbed from 23 to 37. Average price eased to $216K from $239K, and median fell to $65K from $71K. Time on market remained stable at 250 days average, while median shortened to 125 from 210.

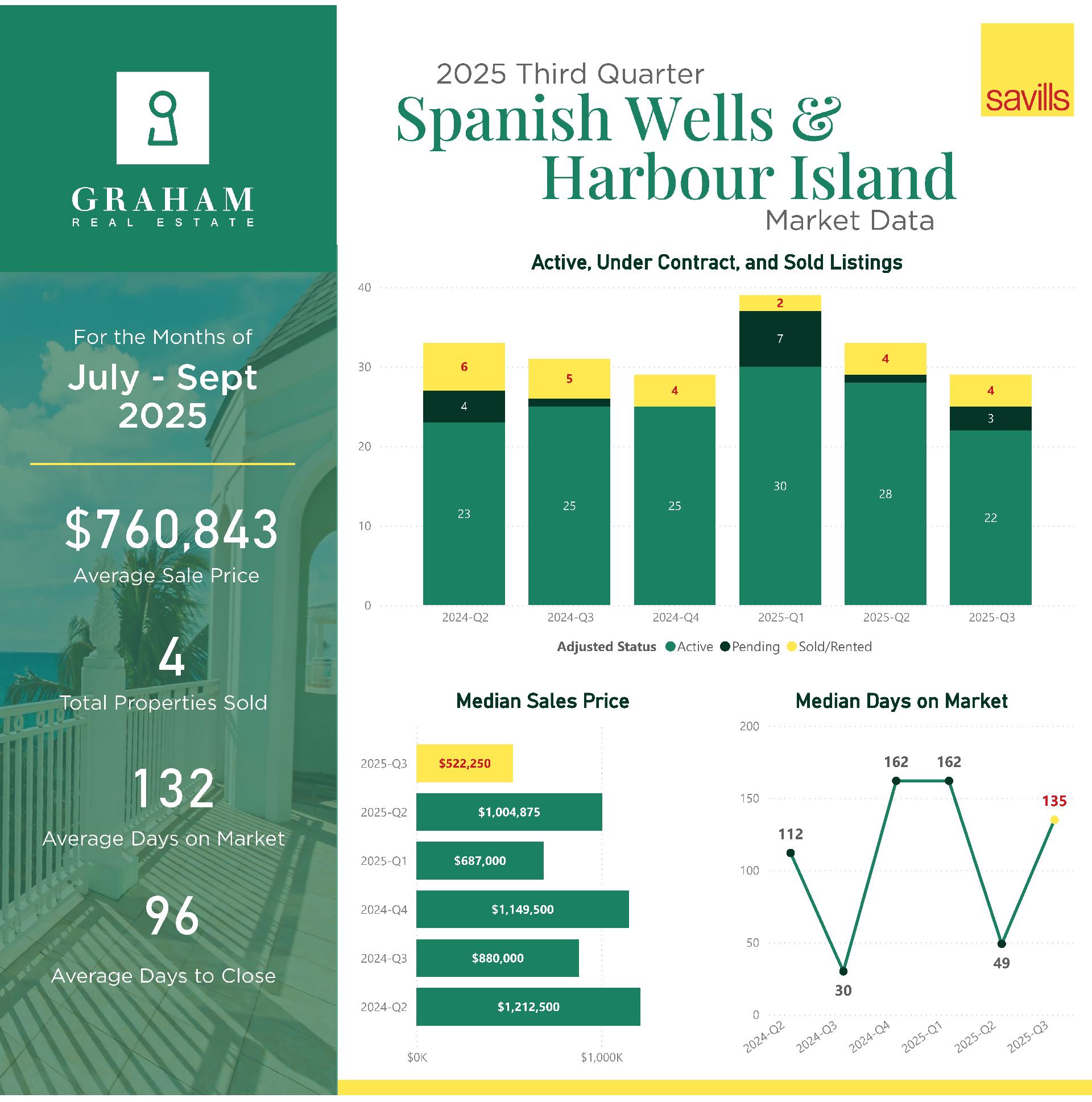

Spanish Wells & Harbour Island

This market remained active, with 4 sales matching Q2’s total and pending listings increasing from 1 to 3. Average price fell to $761K from $987K, and median declined to $522K from $1.00M. Marketing time lengthened substantially — average days on market rose to 132 from 45, and median to 135 from 49 — likely reflecting a shift toward smaller or lower-priced properties.

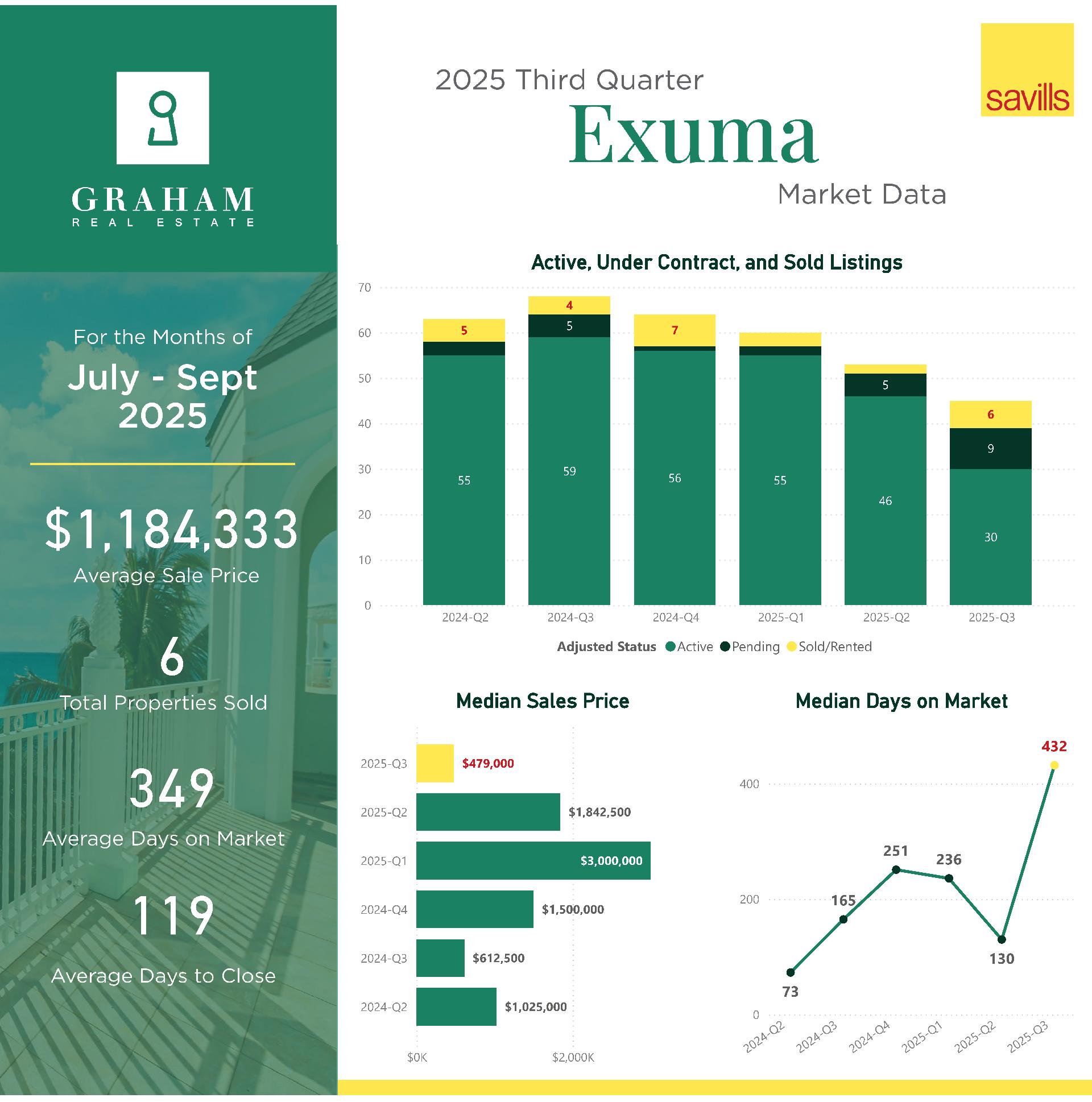

Exuma

Exuma showed renewed activity in Q3. Active listings dropped from 46 to 30, while pending sales nearly doubled from 5 to 9. Completed sales tripled from 2 to 6. Average price moderated to $1.18M from $1.84M, and median dropped to $479K. Days on market lengthened sharply to 349 average and 432 median, indicating that older listings finally found buyers.

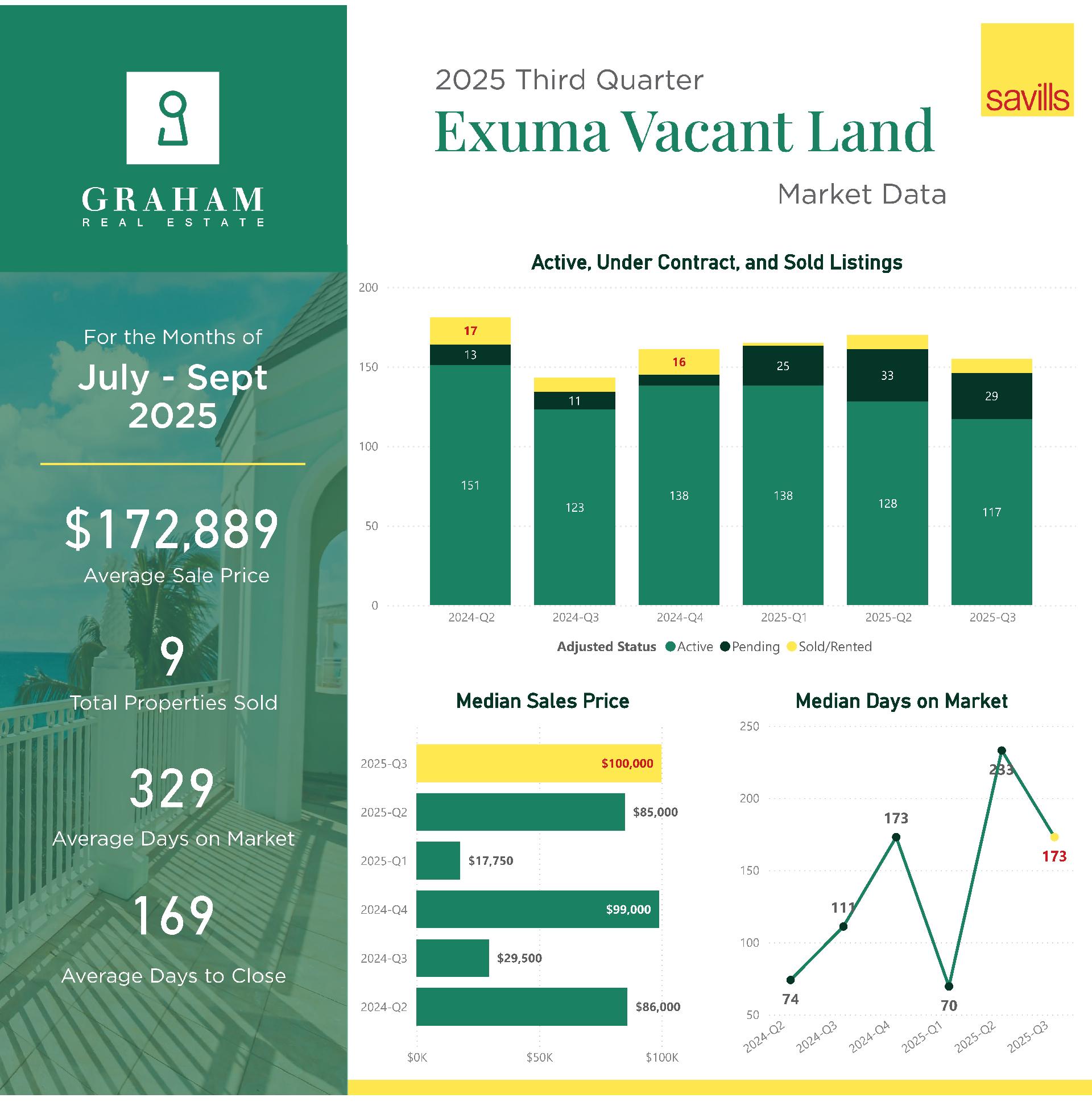

Exuma Land

Exuma Land activity held steady with 9 sales, matching Q2. Average price moderated to $173K from $267K, while median rose slightly to $100K from $85K. Days on market shortened to 329 average and 173 median, indicating improved liquidity.

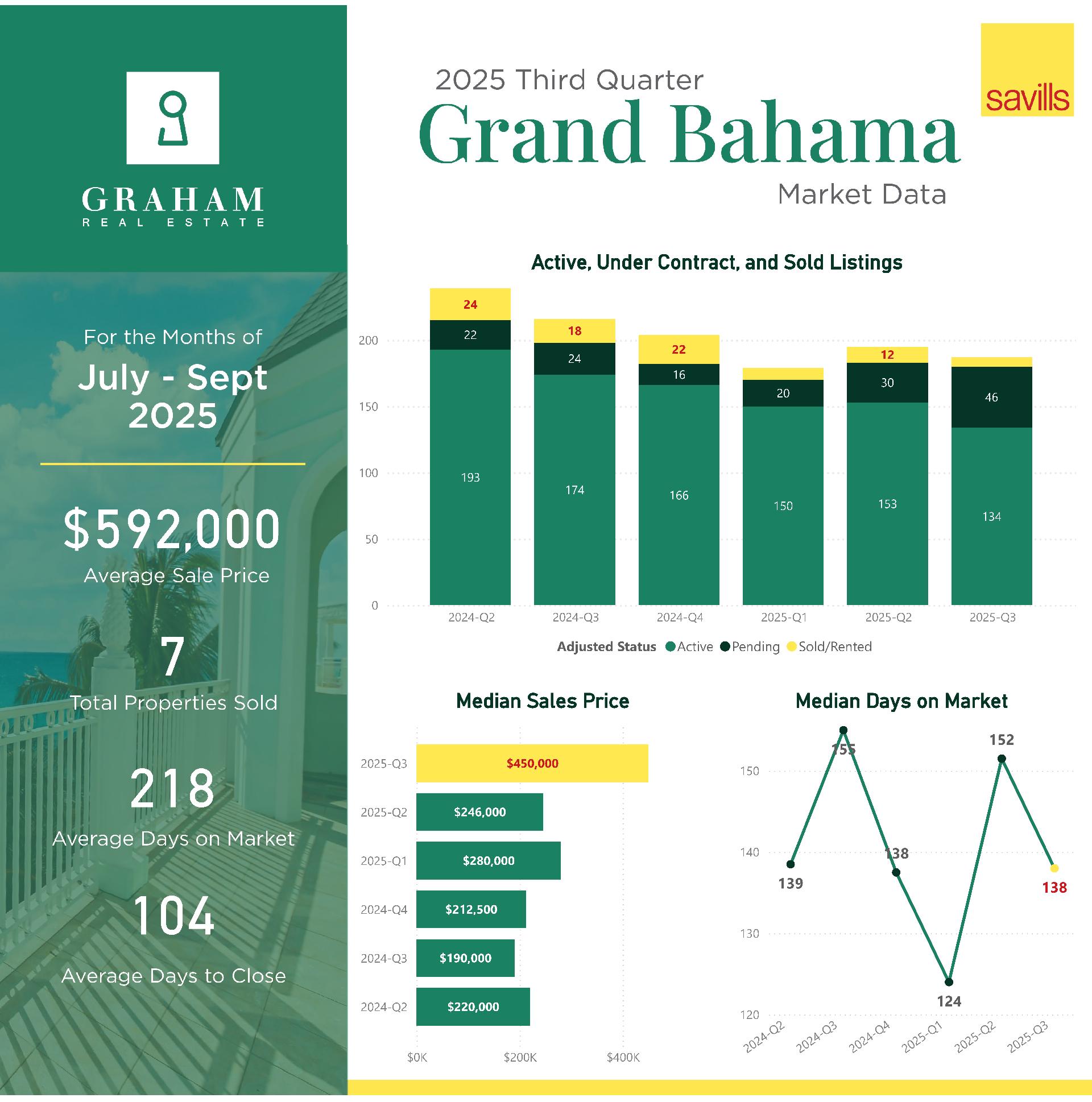

Grand Bahama

Grand Bahama continued its recovery trend. Active listings declined to 134 from 153, and pending sales rose strongly from 30 to 46, though closed sales dipped from 12 to 7. Average price improved to $592K from $517K, and median rose to $450K from $246K. Average time on market lengthened to 218 days, while median shortened to 138, suggesting quicker movement on accessible inventory.

Looking Ahead

Looking forward, the final quarter of 2025 is expected to benefit from the strong pipeline of pending transactions recorded in Q3. As updated VAT and real property legislation continues to be implemented, the market should see smoother closing timelines and increased transactional clarity. Some short-term delays may still occur as stakeholders adjust, but overall, the outlook remains positive, with rising demand in both mid-range residential and select high-end segments heading into year-end.

Conclusion

The third quarter of 2025 showcased a broad strengthening of the Bahamian real estate market. Pending and closed sales rose in most regions, average pricing rebounded sharply in key markets, and marketing times improved significantly. Buyers remain selective, but well-positioned properties are moving more quickly than earlier in the year. The luxury segment showed renewed life, particularly in New Providence and Abaco, while mid-range and land markets continue to provide solid, steady activity. With strong forward momentum, the market enters Q4 on a confident footing.

Disclaimer:

The data presented in this report is based on information available at the time of publication and may be subject to change due to updates or corrections to the MLS. For the most up-to-date and accurate information, please contact us directly. Investors are encouraged to conduct their own due diligence and consult with a qualified professional before making any financial or investment decisions.